On Thursday morning after the Heels were eliminated from the ACC Tournament and were set to miss the NCAA tournament for the first time in forever, I wrote the following intro for the newsletter:

I, for one, appreciate the Tar Heels willingness to sacrifice their post season hopes and sit out the NCAA tourney to protect the American public. This type of forward-thinking vision makes me proud to be a Tar Heel. I can only hope other schools eight miles away follow suit…

By the end of the day, March Madness had been cancelled. Along with all college spring sports. Along with the NBA season. MLB. Hockey. Golf. Soccer (I’m convinced people that watch soccer in between World Cups also say “covid-19” instead of coronavirus. Take the scarf off, leave the non-prescription glasses at home, shave the beard, order a black coffee or a Bud Light, and simma down now). Every conference I can think of has been cancelled.

In our household this week, we had a very real example of how panic sets in. Thursday night, my wife comes back from the grocery store loaded with toilet paper and paper towels. She had a thousand-yard stare. It was a battle ground in there. “We’re going to ration toilet paper, apparently there’s going to be a shortage.” I was incredulous. Everyone is overreacting. By falling into step with it, we only exacerbate the problem. It becomes a self-fulfilling prophecy. Don’t be an accomplice.

Early the next morning, I’m reading one of a billion articles on coronavirus. It says there’s going to be a shortage of toilet paper. Nah, this is absurd. I move on to the next article. But…what if there is a shortage? I’m not part of the problem, but that doesn’t mean the rest of the country is acting rationally. And if the country is filled with a bunch of crazies like you guys, then maybe the crazies are buying up the toilet paper? I go to Amazon and sure enough, a lot of suppliers are sold out. This was escalating. I click on a supplier with 12 rolls available. “But will that be enough?” Maybe we should get 24 rolls? Or 36? If I wait, will those be sold out in a few minutes? If I come back tomorrow, will the world be out of toilet paper? When will toilet paper be available again?

I bought 48 rolls.

And felt totally justified in doing so.

It doesn’t matter if I’m rational if the rest of the world isn’t.

The next morning (and I cannot make this up) we get an automated call from the county water company at 6:30am. The entire county’s water supply has been exposed to E. coli. Stop drinking water immediately. Stop cleaning yourself in it (which fans of irony will love since washing your hands regularly is how to prevent coronavirus). Boil water before using. The next automated call was going to be about zombie sightings, I was sure of it.

I called the wife from the office, “We need bottled water.” She was already in the car with our oldest son, who’s school had just been cancelled. I asked which grocery store she was headed to. “Neither of the two we normally use, they will already be out.” So smart. She was headed into the next county. I imagined a tidal wave of cars a la Mad Max, racing toward the county border. First ones there live, everyone else dies. She pulled into a gas station, thinking they wouldn’t have been looted yet. But she immediately saw a line of people stockpiling water and just kept driving. Grocery stores. Convenience stores. Sold out. She headed to Staples. She must have beat the office crowd because they still had bottled water. Told you she was smart. She loaded up. We would live though the day. We’ll worry about tomorrow if the sun comes up.

With water and toilet paper from Amazon adequately stocked to survive a few days, she headed to a grocery store to buy anything that hadn’t been bought by other customers. All the carts were being used by other customers at 7am. It was a zoo. Everyone had multiple carts, so she and my son grabbed a couple of race car carts intended for kids. She had two, a Panic Cart and a Normal Cart. Panic Cart got bulk, emergency supplies like Mac & Cheese the kids would live off of for months. And a shocking amount of wine. Normal Cart got stuff others were passing over, like avacados and turkey bacon. Our son popped out from around the corner, crazy eyed from the battle, and held up completely random items he had snagged, happy to find anything. “Throw them in the cart and keep grabbing stuff!” She was Platoon Leader mode and was giving orders, not suggestions.

She came home and filled the pantry up with her spoils of war. Then she started to boil water, which must have just been for the two of us because the kids live off chocolate milk and seltzer water. She called me in a panic, “The county is cutting off all water. We need to fill up buckets to let the toilets flush. Where are the buckets?” Buckets? We have buckets? I mean, maybe one somewhere in the back of the closet in the garage but I’m pretty sure a family of spiders is wintering in it. She started filling up pots and large mugs with water. I started checking hotels in the next county over. Booked. This was insanity. Apocalyptic. Tell the kids to shower ASAP.

A few hours go by, and I check back in. The water hasn’t been cut off yet. “Where did you hear water was being cut off?” I asked. “A friend of a friend said she saw it online…”. We checked the website, no news of water being cut off. We had been so caught up in the frenzy we hadn’t stopped to fact check. We had stopped behaving rationally. We had fed into the vicious cycle. We were part of the problem.

And that little microcosm helps explain last week’s rate market movements. The time for rational talk about fundamentals and liquidity is for tomorrow. Today, it’s all about survival. Algo trading has only exacerbated this issue because computers aren’t rational or irrational, they simply follow the rules. Human traders may look at a plunging 10 Year Treasury yield at 0.75% and say, “That’s absurd, I’m selling here.” But they can’t, because the algo trading is triggering more and more buying, forcing down yields further. So the humans sit on the sideline, waiting for the dust to settle before jumping back in.

A decade ago, the 10T probably wouldn’t have broken 1.00%. But today, traders just ride out the storm and jump back in when the computers are done re-positioning.

The market can stay irrational longer than you can stay solvent.

And so can your fellow grocery shoppers.

Last Week This Morning

- 10 Year Treasury touched 0.48% before closing the week at 0.96%, so yeah things are volatile

- German bund jumped higher by 20bps to -0.55%

- Japan 10yr climbed 20bps to positive territory, 0.02%

- 2 Year Treasury is not experiencing the same volatility as the T10 because it’s driven by Fed Funds expectations, closed the week at 0.49%

- LIBOR dropped to 0.70% and then rebounded to 0.80%, while SOFR is back up to 1.20%

- ECB disappointed by not cutting rates

- The Fed cut rates to 0% and rolled out $700B of QE5

- Oil below $40/barrel

- the Heels can’t miss a tournament that never happened

- the real reason I’m so mad at coronavirus is that it is cancelling college. Our two daughters came home from spring break and now they’re not going back. What have I done to deserve this!?

- Every company I have ever interacted with is emailing me. I get it, you are taking it seriously. Stop cluttering up my inbox.

FOMC Meeting

On Sunday night, the FOMC cut interest rates 100bps to 0% – 0.25%. Hello ZIRP, good to see you again. Can negative rates really be totally ruled out?

I’m not sure how warm and fuzzy markets will respond to this. They are going to wonder if the Fed has any more dry powder. Are things worse than we realized?

I had thought it was a coin toss between a 50bps cut and a 100bps cut, but there was no scenario where they wouldn’t cut to 0% eventually, so why not just get it over with?

- 0 – $700B ($500B Treasurys and $200B MBS)

- Cut reserve requirement of banks to zero

- Enhanced swap lines for with foreign central banks to provide greater liquidity in dollars

In the six weeks since the last scheduled FOMC meeting, the Fed has enacted two emergency rate cuts. On March 3rd, it cut rates 50bps. Last night, it cut 100bps.

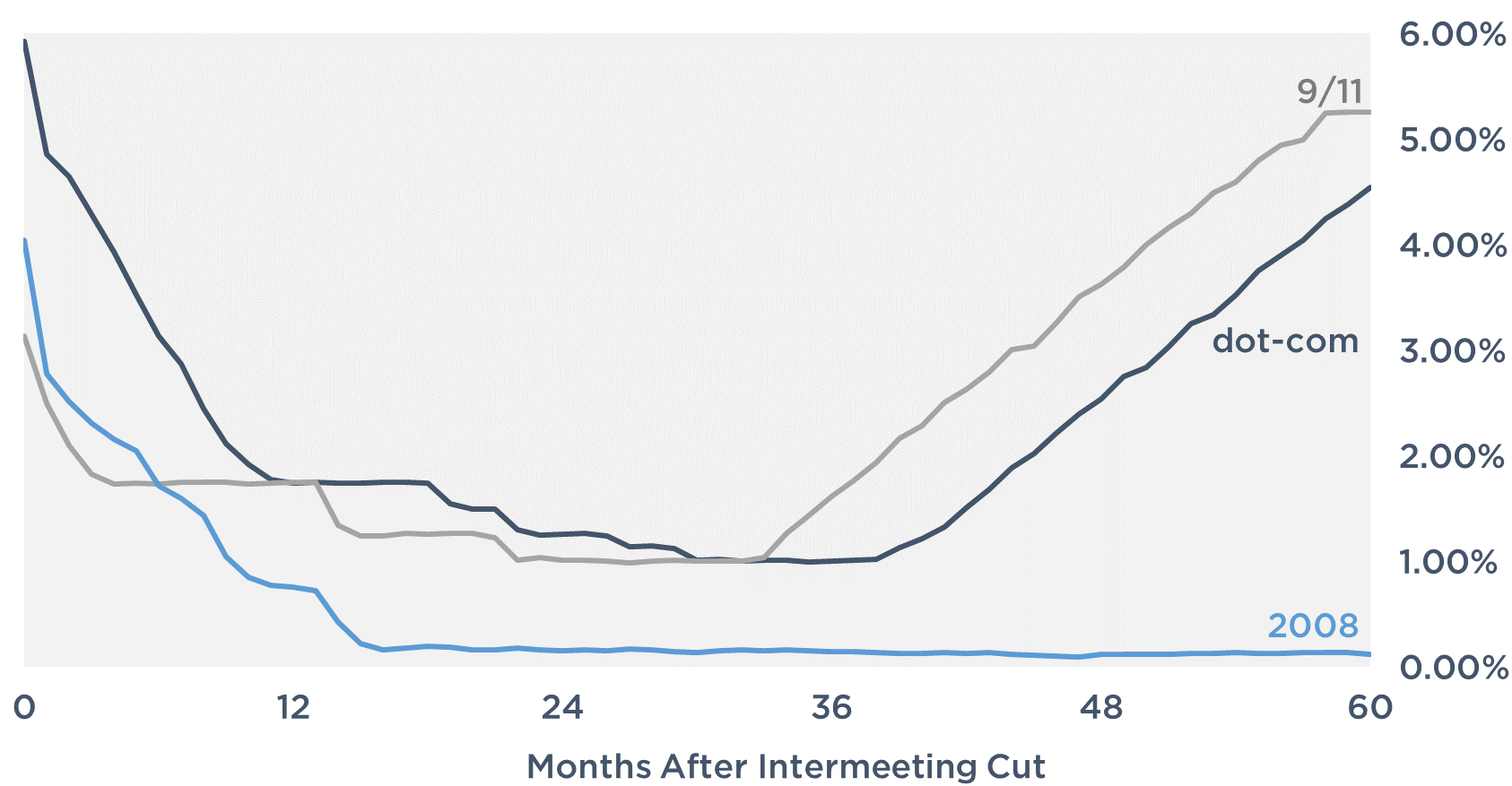

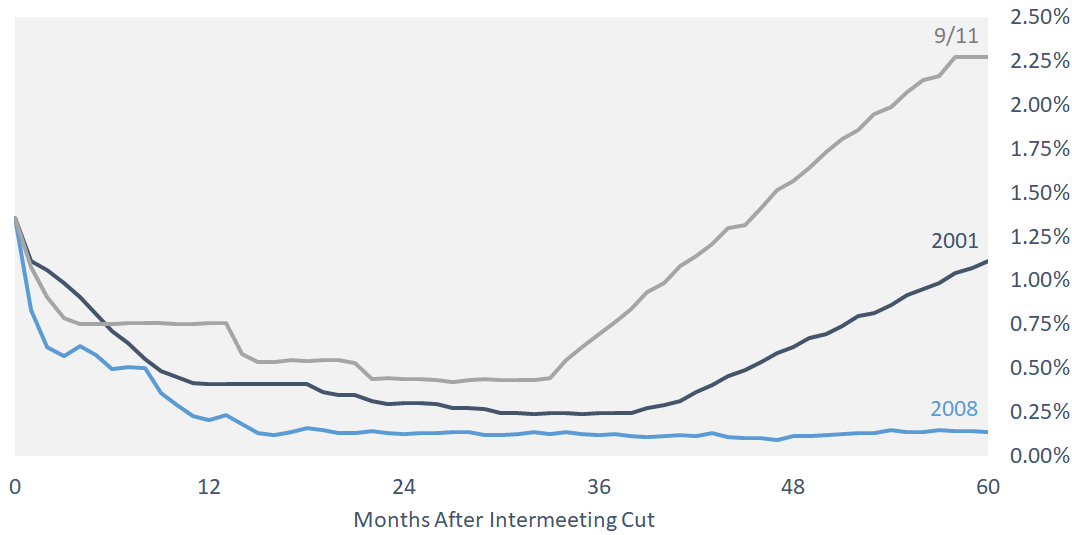

Intermeeting cuts are so rare, they always signal a significant market event. Something happened to cause the Fed to cut rates between meetings. Dot-com, 9/11, financial crisis, etc.

We went back and looked at how Fed Funds behaved in the years after an intermeeting cut. In other words, when there’s a significant catalyst for a sharp downturn, what do floating rates look like in the subsequent years?

They head lower for two years, but then what happens next was dependent on the cycle.

Following the dot-com bubble and 9/11, rates were on the rise again within 2-3 years.

Following the financial crisis, they stayed flat for a decade.

Here’s what LIBOR would look like over the next five years if it followed previous cycles.

Which path we follow depends on where we head from here.

Black Swan Event

Over the last few years as we worried about the expansion ending, I was frequently asked what the next black swap event would be. Student debt was a common refrain. China dumping Treasurys. No one, not a single person (me included), ever mentioned a pandemic. Yet, here we are. We have our black swan. It always seems so obvious with the benefit of hindsight.

Our economy is going to fall off a cliff. If we aren’t in a recession today, we are about to be. Q2 and Q3 are almost certainly going to show significant contraction. China will slow further. Europe is now the epicenter and may experience the worst economic downturn of anyone. The only tool we have to fight coronavirus is social distancing. That means we stop doing everything, hunker down, and try to outlast it.

A week ago, Seattle banned gatherings of more than 250 people. Seemed draconian. A month from now, it will seem understated.

Schools started with extending spring break. Or maybe just cancelling for two weeks. This is just the start. They are just buying themselves time to announce the formal plan. The reality is that kids are not returning to school this spring, it just hasn’t been announced yet. It sounds drastic today, but a month from now we will have forgotten when it ever felt awkward. Maybe they resume in the fall, but there will be a lot of talk about how the virus has been lying dormant during the summer months and a second wave could begin.

If shops close, where do those employees go? Can they survive a month without pay? Probably not. And if shops are closed, they can’t simply move to a competitor. What about childcare? The unemployment rate is about to rise. Is it going to 5% or 10%? How long will it take?

Everything we do is about to change. A week ago, we would have thought canceling the NBA season was absurd. Turned out they were just the first. And it doesn’t matter if you are aren’t compromised, because others are.

There is some non-zero chance that we are all effectively living under some version of house arrest within a month.

The US is about to close for business and probably doesn’t reopen for business until June at the earliest, aided in part by summer temps that the virus can’t survive. Life may not return to normal until the fall.

The recession is unavoidable. The depth and length will be determined primarily four, interconnected items:

- Consumer spending – as we pointed out in last week’s newsletter, consumer spending comprises 2/3rds of GDP and will likely dictate whether we experience a U-shaped or V-shaped recovery. This will be a long-term measure. We are almost certainly in a recession already and demand will bring us out of it, but when that occurs is the question. How quickly will life resume as usual? How many people lose their jobs as a result of this?

- Monetary policy – The Fed has cut to 0% and announced other measures. It has injected $1.5 trillion into the repo market (still not QE though). It recently said it will cap Treasury yields if necessary. It would take a pretty bad stumble by Powell at this point for the market to suddenly believe the Fed is asleep at the wheel. This box is largely checked already.

- Federal government response – this is the one that matters the most. Markets rallied Friday as Trump declared a national emergency because it meant the federal government was finally awake to the dangers. The more aggressively the government intervenes (social distancing measures, airline bailouts, emergency aid, tax holiday, etc), the more positively the market will react. If Trump undermines policy with an ill-timed tweet or ignores the advice of medical professionals, the market will respond negatively. It’s time for Congress to do its job and may God have mercy on the party that tries to politicize this. Fiscal intervention, aggressive medical response, and social distancing rules will create confidence and, in turn, drive consumer spending.

- Pandemic curve flattening – life has changed a lot in the last week and it’s going to change a lot more this week. And the next. I think we are working and living at home by the end of the month. The stats haven’t really impacted us yet, but this is the calm before the storm. By the end of March, I bet we are living under quarantine-type laws, self-imposed or otherwise. The number of cases by month end or in April will blow us away. We aren’t scared yet, but we will be. We are just late to the party. Loved ones will be affected.

Depending on how quickly and aggressively we intervene, this could be more like dot-com or 9/11 than the financial crisis. Here’s how some benchmarks behaved in the month following the start of the downturn.

- After 9/11, GDP fell to -1.7%. But by the end of Q1 2002 (within six months), it had rebounded to 3.6%.

- After the financial crisis, GDP fell to -8.4%. But it took a year to turn positive again.

One recession was shallow and short lived, while the other was deep and long-lasting.

The more aggressively we intervene now, the quicker the recovery will be.

Stocks and bonds are behaving like this is the second coming of the financial crisis. But it doesn’t have to be.

The federal government needs to take the lead and pull out all the stops to avoid -5.0% GDP over the next six months. This isn’t something the Fed alone can address.

Credit is Key

I remember when the world started falling apart in June 2007 (a year before most of America became aware of the issues), one of our swaps traders said, “a credit crisis is the worst type of crisis.” When credit stops, everything stops. The financial crisis wasn’t a run of the mill recession the way the dot-com or 9/11 recessions were because of how credit behaved.

While credit markets are certainly repricing, they have not frozen up…yet. Yes, I know you are seeing Agency spreads widening. And CMBS is off and on again. But there’s a difference between getting a higher loan spread and not being able to get a loan. I learned that in 2008.

Whether these seize up totally or just reflect repricing will likely dictate the severity of this downturn.

ZIRP encouraged record corporate borrowing. US corporate borrowings exceed $10T. How this market, particularly the high yield (junk) bonds, perform could dictate the severity of the downturn.

Defaults will rise. Downgrades will occur (you think maybe the airlines are going to be downgraded soon?). And some big bond holders (like pension funds) must sell if bonds get downgraded below a certain level. Forced, mass selling causes market seizures.

Here’s the high yield bond index ETF. Not as bad as 2009…yet.

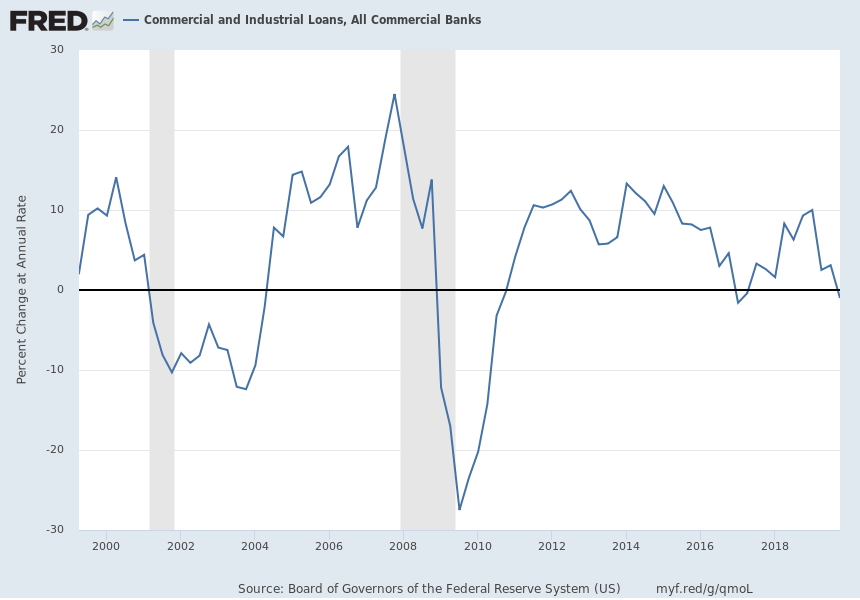

Below is a graph of the Fed’s measure of loan growth. When credit contracts, the economy contracts. Or is that vice versa? Either way, we are in the danger zone and at this point it’s a matter of how much will credit contract. How long before lenders start using their Material Adverse Change (MAC) clauses to re-trade you or pull out altogether?

We spend our time talking about interest rates, but that graph should grab your attention. I’m asked all the time about the likelihood of interest rates rising. You know what 2008 taught me?

Lending appetite is a much bigger risk than rate risk.

Sure, a defeasance penalty might be expensive today. But how cheap will it look if you can’t get a loan 12 months from now?

Sure, the spread you were quoted has gapped wider by 0.75%. But a month from now you might not be able to get a loan at all.

What if your tenants fall behind this year? Or declare bk? Are you still getting today’s favorable loan terms then?

Lenders are usually slow to cut the credit spigot back on, so even if we are exiting the recession by year end, lending may not return to normal levels until late 2021. If I have a loan maturing in that window, I’m actively looking at alternatives. Or ensuring I can hit extension hurdles.

I’m refinancing today not because the T10 is going to rebound to 1.75%, but because I may not be able to get a loan when my current one matures.

Panic or Just Repricing?

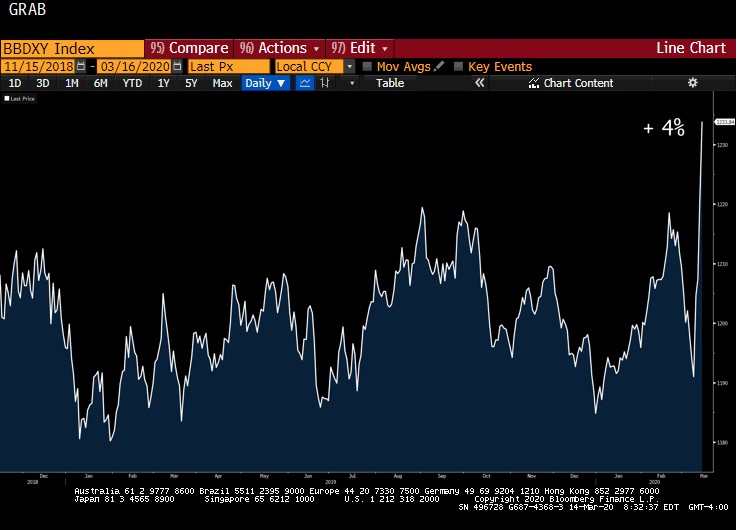

As the reserve currency, the dollar serves as a decent barometer of panic. It’s one thing to buy or sell to get out of a position, it’s another to stick it under the mattress.

In the four weeks after the financial crisis started, the Bloomberg Dollar index jumped 10%. Within another month, it was up 26%.

Over the last two weeks, the same index is up just 4%. Maybe it keeps spiking and sends up a red flag, but as of right now it is not behaving like it did post-2008.

That doesn’t mean this downturn won’t be bad, just that the classic red flags haven’t hit 2009 levels. Yet.

I was in Texas two weeks ago as the 10 Year Treasury was testing the all-time low of 1.36%. I had my handy dandy Financial Conditions graph. I pointed out that while Financial Conditions can tighten quickly, it is tough to be in a recession when conditions are as accommodative as they were. Welp, that changed quickly.

But when we step back and compare to other periods, we are still quite a long way from 2009 levels. But it’s getting worse. This index will be more restrictive a month from now than today. But with aggressive Fed monetary policy coupled with fiscal intervention, the worst-case scenario of 2009 can be avoided.

One Really Big Difference Between Today and 2008

So what reminds me of 2008? The unknown.

What’s different? The outlooks are flip-flopped.

In 2008, we started pulling a thread and had no idea how long we would be pulling before it stopped. The further out the horizon we looked, the less certain we were.

Today, we feel less certain about the next 24 hours (buy toilet paper!), but feel like coronavirus will be contained at some point. Maybe a month. Maybe this summer. We were slow to act and ill-prepared, but this is something we can wrap our arms around.

In many ways, the extreme intervention that made the last week feel so weird (empty arenas for basketball games) is the same sort of action that makes the market feel better about a resolution over the longer term.

That’s why I think this will ultimately play out more like a traditional recession and less like a financial crisis.

Unless credit freezes. Then all bets are off.

Week Ahead

It has not been confirmed, but it seems like Sunday’s surprise meeting will replace Wednesday’s scheduled FOMC meeting.

Last night, the Fed went all-in.

Congress – your move.