Our office has a Segway the youngins like to ride around on, but I refuse to. I try explaining to them that I don’t fall the way they do. I’m old, out of shape, and unathletic. If I go down, it won’t be a gentle tumble.

This weekend proved my point. My wife and I started playing pickleball, which in itself is a painful reminder that age is catching up to me. But my brain is still convinced I am a young, athletic, hyper-competitive twenty something.

My wife, a former D1 athlete, dropped a beautiful shot barely over the net, painting the line. I was on my heels, but took after the chase anyway. As I got closer, I realized I had a chance to make the shot. I extended the paddle in my hand, reached with all my might, and flicked the ball back over the net..just as my wheels gave out and I began falling hard onto the concrete. This was not a dive. I did not consciously decide to lunge for the ball, I simply was unable to keep myself upright.

My sunglasses exploded off my face, the paddle went flying. I laid there, stunned, trying to determine if anything was broken. The first words out of my mouth were, “Did I get the point?”

“No.”

She had heartlessly, ruthlessly, coldly returned my all out shot back to the wide open middle of the court while I laid there, presumably bleeding to death. Not from jai alai. Or parkour. Or mountain biking. From pickleball. It was emasculating on so many levels.

I was banged up, bleeding everywhere, wondering where my athleticism had gone. My wife, supportive as ever, said, “Get up already - chicks dig scars.” I would have never forgiven her for a sympathy point and she knew it. Ahh love.

That love will also be tested as we begin our 11 day cross country RV trip with three teenage boys this week. We have never driven an RV, have never parked an RV, have never fueled an RV…you get the picture. I have no idea when the next newsletter will be, but if you don’t hear from me again, just assume I’ve abandoned the RV, and maybe the family, and I’m tearing up an RV park as the Bad Boy of Pickleball.

Last Week This Morning

- 10 Year Treasury up to 2.83%

- German bund up to 0.94%

- 2 Year Treasury at 3.23%

- LIBOR at 2.37%

- SOFR at 2.29%

- Term SOFR at 2.29%

- Nonfarm Payrolls came in at 528,000 vs expected 258,000

- Unemployment dropped to 3.5%

- Consumer borrowing jumped by $40B, the second most ever after March

- Pre-covid, the biggest increase on record was $28B. Consumers keep on consuming, but they are using debt to do it. That tends to work as long as unemployment doesn’t climb.

Jobs

This was an incredibly strong report, no doubt about it. The consensus forecast was a gain of 250k, so the 528k gain was a staggering upside surprise. The three and six month averages are around 450k – not indicative of a recession.

This report also means the economy has regained all jobs lost as the result of the pandemic. This year alone, the economy has added 3.3mm jobs.

I’m still of the mind that hiring at year end will be a better reflection because it takes firms a while to downshift hiring plans. I think the Great Resignation may also exacerbate this. How many of us have struggled to hire/retain talent over the last year?

Just like the Great Financial Crisis caused firms to be slower to hire, the Great Resignation may make them slower to pause hiring or do layoffs.

I expect hiring to move materially lower in the next year. Remember, at the first rate hike in March Powell reminded us that it takes 12-18 months for Fed policy to work its way through the economic plumbing. The public markets react immediately, but the actual data takes a hit a year later.

It’s almost hard to believe, but rates were at 0% just five months ago. Even though our universe has changed dramatically, the real impact is to be felt next year.

Jobs Impact on Rate Hikes

The last Fed meeting had a baseline of 75bps, with 100bps on the table.

The September 21st meeting has a baseline of 75bps, but with 50bps on the table.

While this report doesn’t quite lock in 75bps, it does increase the likelihood.

More importantly, if inflation falls this week as expected, it might save the Fed from itself. If the Fed pulls back too soon, it may concede hard fought ground on the inflation front. Continued strength in the labor market, particularly wage inflation, probably keeps the Fed on track for an aggressive hike in September.

CPI – Wednesday

CPI, the one we will see plastered all over the headlines Thursday morning, is forecasted to have dropped from 9.1% to 8.7%. This sort of move would be mostly attributable to oil prices.

But if you’ve been reading this newsletter, you know that right now the Fed is laser focused on the monthly reports. Is inflation accelerating or decelerating? Show me the monthly!

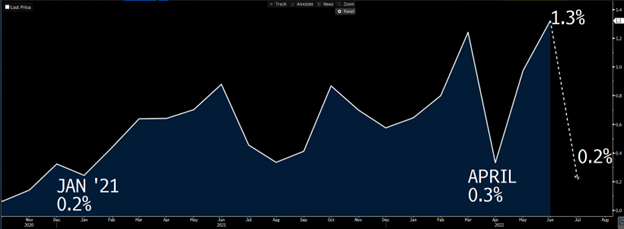

CPI m/m is forecast to plunge from 1.3% to 0.2%, its lowest point since January 2021. Even though Powell can do a mean cartwheel, I think he’s saving that for a successful soft landing. A CPI m/m number like this probably won’t break out the cartwheel, but probably gets a nice little exhale.

Source: Bloomberg Finance, LP

Source: Bloomberg Finance, LP

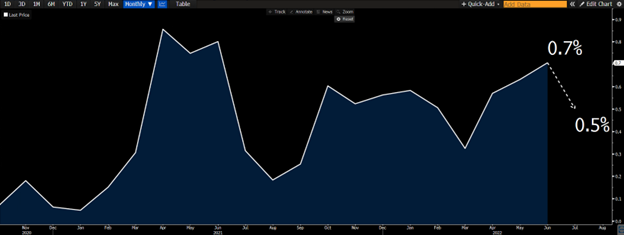

Let’s take it a step further because we know the Fed also prefer “core” inflation readings, meaning it strips out volatile food and commodity prices. Core CPI m/m is expected to drop from 0.7% to 0.5%. The plunge isn’t as extreme because it isn’t benefitting from lower oil prices, but it’s a move in the right direction nonetheless.

Source: Bloomberg Finance, LP

Source: Bloomberg Finance, LP

PPI – Thursday

The less referenced inflation reading is PPI, which measures inflation for producers rather than consumers.

This tends to front run CPI by a few months. Producers feel the pain first, and then try to pass it on to consumers.

Headline PPI is expected to drop from 11.3% to 10.4%, which would be the lowest reading since the beginning of this year.

Core PPI is also expected to drop, from 8.2% to 7.7%. This would be the lowest reading in almost a year.

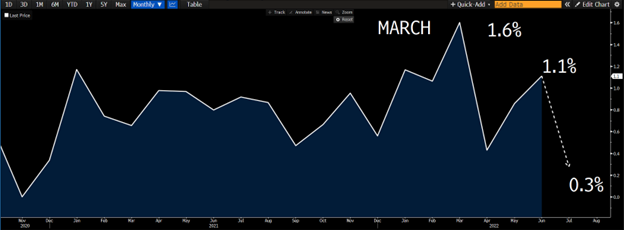

PPI m/m is expected to plunge from 1.1% to 0.3%. Oil - that’s the main reason. When you want to accuse the Fed of cherry picking data and excluding commodities for its preferred inflation readings, remember this graph. The Fed isn’t saying oil doesn’t matter, just that it’s hard to determine policy with a one year lag when oil can run up to $130 and back down to $90 in a few months.

Source: Bloomberg Finance, LP

Source: Bloomberg Finance, LP

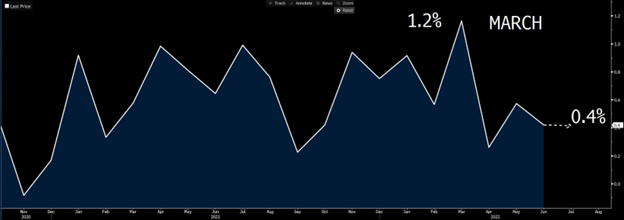

Stripping out food and commodities, the Core PPI m/m is expected to remain at 0.4%. But that’s in large part because it peaked back in March. Remember, it leads CPI by about 3 months. This is still an elevated number, but an enormous improvement from double digits.

Source: Bloomberg Finance, LP

Source: Bloomberg Finance, LP

Takeaways

This could be a huge first step. If these readings come out as forecasted, it’s a signal that relief is on the way.

Most importantly, this could take the worst-case scenario off the table. I think the hypothetical worst case is why so many firms and lenders are pencils down. Take that away, it’s easier to make decisions.

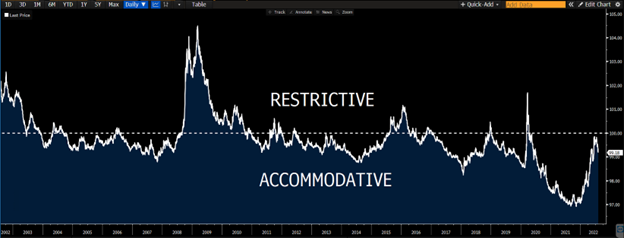

Check out my favorite graph, Financial Conditions. After spending the first six months of the year barreling towards restrictive territory, they’ve actually retraced a bit. This is the sort of signal that the credit spigots might open again.

Source: Bloomberg Finance, LP

Source: Bloomberg Finance, LP

Week Ahead

The main focus of the week will be CPI data which will be released on Wednesday. Thursday brings us jobless claims and leads us into PPI and prelim U-Mich Consumer Sentiment and 5Y Inflation expectations on Friday.