I wonder how many World Cup visitors are going to be supremely disappointed when they side quest to West Virginia because of that song…

Last Week This Morning

-

10T: 4.56%

-

2T: 4.21%

-

SOFR: 3.53%

-

Term SOFR: 3.66%

-

Existing Home Sales: 4.09mm vs 4.20mm expected

-

Fed Speeches

-

Fed Waller: “I continue to believe that forward guidance can be a valuable tool that has, at times, significantly strengthened policymaking and will continue to be useful.”

-

Fed Williams: “The markets still expect oil prices to come down over the next six to twelve months. I think that's a pretty reasonable baseline.”

-

-

The USA was so bad against Belgium that “James Franklin” started trending on Twitter

Tuesday - CPI Up to Bat

Tuesday brings the All-Star game to the greatest city on Earth…as well as the next CPI report. This could be a doozy for the front end of the curve (and therefore caps).

Headline CPI is expected to fall from 4.2% to 3.8%, while the m/m reading is expected to fall from 0.5% to -0.1% (yes, negative 0.1%).

I think I speak for all of us when I say, “yes please”. Remember, CPI is much more directly influenced by oil than Core PCE is…but it would still be welcome news.

Even if Iran keeps getting derailed, this type of retreat gives the Fed cover fire to sit pat. “See! The recent spike in inflation is transitory merely the reflection of surging oil. And as soon as that reversed course, inflation reversed course right with it. Even if it goes back up again, we just need to wait it out.”

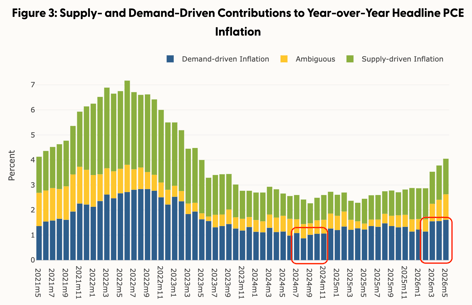

All that being said, we are not out of the woods, either. I’ve shown you guys this graph a lot over the last few years. Adam Shapiro is an SF Fed Economist and he does some great work on the components of inflation: demand/supply/ambiguous. The demand component is double what it was two years ago.

In fact, the demand component alone is 1.61% of overall Core PCE. If just a small piece of the ambiguous component is really demand, suddenly we are north of 2%. And that’s before we tack on any supply side effects.

Do you see what I’m getting at? Fed monetary policy impacts demand…the demand component is climbing…the Fed may hike…

Is the oil shock masking a rising demand inflation issue?

I believe strongly the Fed is on hold this year, but I have to remind myself to not assume all inflation right now is related to an oil shock.

Most Overlooked Story Last Week

SMBC Chief Economist Joseph Lavorgna said on Bloomberg that Trump would be fine with a hike. There’s no way that’s true, but here’s the argument: hiking Fed Funds could very well drive down the T10, which directly influences mortgage rates, which is Trump’s focus. Make America Affordable Again!

Not only is Lavorgna a well-respected economist, but he spent the last year as an economic advisor to Scott Bessent. He also was Chief Economist of the National Economic Council during Trump’s first term.

Did Bessent ask Lavorgna to signal the market? Or was he just providing an opinion?

Rates

I still don’t believe the Fed will hike this year. I don’t care that 9 out of the 19 FOMC members see at least one hike this year - Fed officials are the only ones worse at forecasting than me! Warsh et al are talking tough about hikes so that they don’t actually have to hike…and it’s working. So much for avoiding forward guidance, huh Kevin?

Oil is driving inflation and a rate hike won’t change that. Plus, the labor market isn’t overheated, so a hike right now has an asymmetric risk/reward profile. A hike barely helps inflation, but could really hurt the labor market. Only a foolish apex inflation hawk totally insulated from economic gyrations because he’s married to a billionaire so he’s totally price insensitive and doesn’t need a job would consider hiking given that…

Here’s my overly simplistic mental model about hikes vs no hikes this year:

-

Hikes right now will do more harm to the economy than they will help inflation.

-

This will ultimately cause the Fed to cut more next year.

-

-

An extended pause right now allows the oil shock to work through the system the way tariffs did

-

The Fed resumes cutting next year, but only once or twice.

-

This is a continuation of the last two years’ “easing off the brakes”

-

We drift down to 3%-ish

-

Meanwhile, the T10 is stubbornly range bound. Iran is as muddied as ever and the eco data is conflicting, at best. It’s going to take something dramatic to break resistance levels of 4.11% and 4.66%.

The Week Ahead

Lots of Fed speeches and Tuesday’s CPI report are the main catalysts outside of Iran news.