Strait Jacket

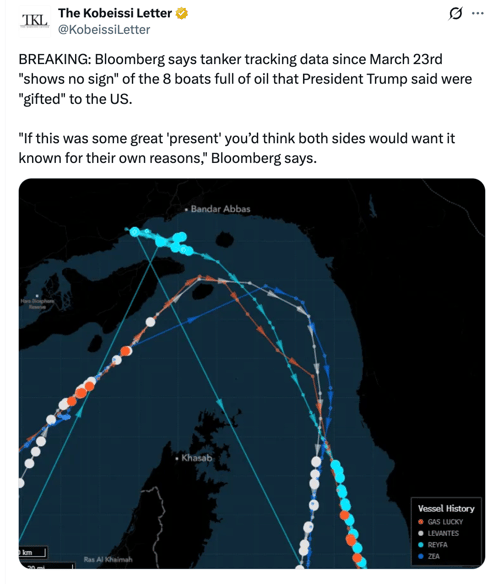

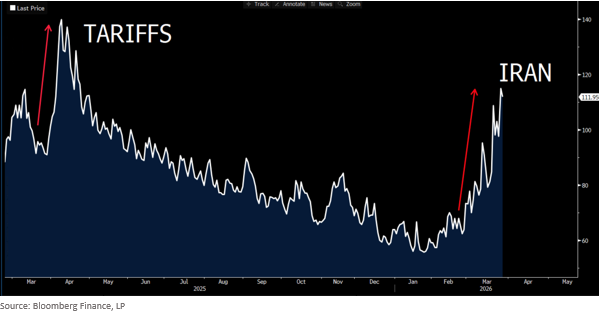

Markets are pricing in hikes rather than cuts. Caps have doubled or tripled. Oil is swinging by $20/barrel every day. Trump says Iran allowed 8 ships through as a gift to him, Iran denies it, and Bloomberg ship tracking shows no evidence. What a time to be alive.

Last Week This Morning

-

10T: 4.43%

-

2T: 3.92%

-

SOFR: 3.65%

-

Term SOFR: 3.67%

-

UMICH Consumer Sentiment: 53.3 vs 53.5 expected

-

Fed Speeches

-

Fed Barr: “I think if it turns out that inflation pressures remain contained, we will get to a place where we cut rates sooner than later.”

-

Those Jobs Tho!

Everyone wants to focus on the impact the oil shock will have on inflation, and it’s fair. But once we get through this burst, what about the effect on the consumer? Higher oil is a tax. How about the effect on corporations? Like tariffs, they won’t be able to pass all increases through, which means it comes out of margins.

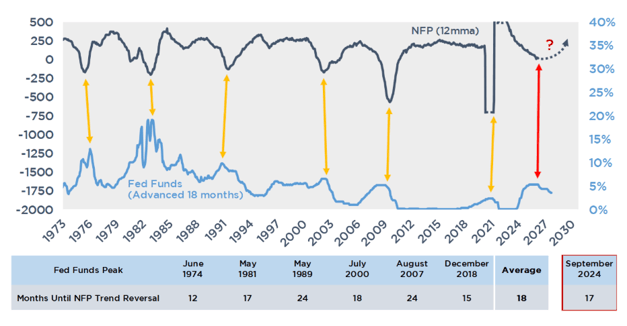

The labor market has been in a low hire/low fire cycle for the last year… is oil the thing that finally topples it?

Historically, the job market bottoms out 18 months after the first rate cut, which would be… Friday. But I’m not sure we ever had an oil shock and escalating war exactly 18 months after the first cut. Oh, and maybe the biggest technological advancement in the history of mankind. But it’s still a cool graph so here you go.

Friday’s NFP is forecasted to come in at +60k. Last year, the average monthly revision was 58k so you do the math. Just as importantly, will last month’s terrible print be revised even worse?

Does this feel like an economy well situated to handle a shock? We lost 92k jobs last month. Now is not the time to hike.

The Fed is Stuck

If you want the Fed to hike but can’t tell me how raising rates will lower oil prices, talk to a wall.

SF Fed economist Adam Shapiro was a co-author of a paper in 2024 that illustrated how rate hikes impacted financial stress depending on whether inflation was demand driven or supply driven:

- if demand driven, rate hikes had a negligible effect on financial stress

- if supply driven, rate hikes had a significant and immediate effect on financial stress

This research suggests that a hike now will results in a significant spike in financial stress, with credit spreads, equity risk premia, and default risk all moving in the wrong direction.

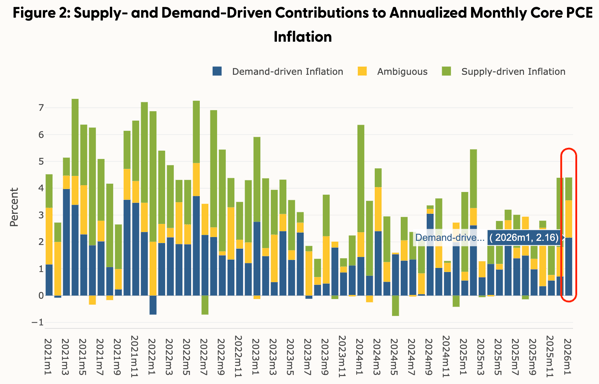

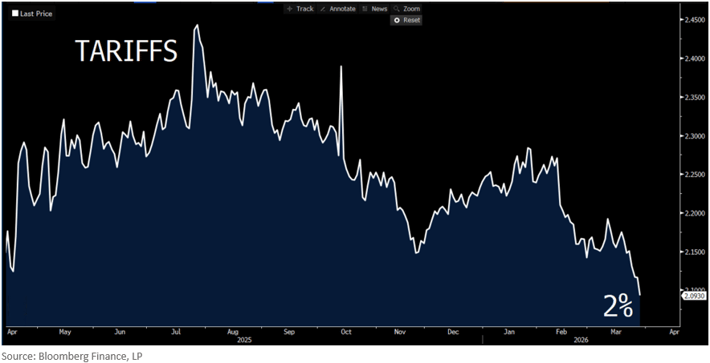

Core PCE is already at 3.1% and the Fed’s target is 2%, but it’s at 3.1% because of tariffs that were just ruled unconstitutional.

The graph below is also from the SF Fed. It breaks down the composition of Core PCE between demand, supply, and ambiguous (I’m focusing on the monthly number because the annual numbers move much more slowly). The “demand” inflation component is just 2.16% - basically the Fed’s target.

I believe very strongly that the Fed will be far more concerned with inflation expectations than actual inflation. They won’t want expectations to become unanchored. While short term expectations have spiked, longer term measures are viewing the upcoming burst of inflation as transitory temporary.

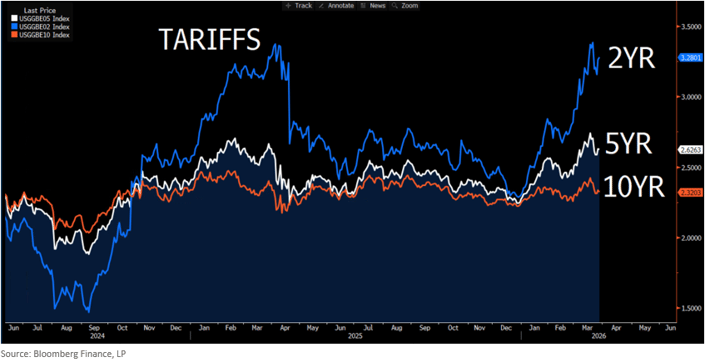

Forward inflation expectations from market pricing:

2yr 3.28%

5yr 2.63%

10yr 2.33%

The Fed is on hold until the optics of cutting in the face of surging inflation subside. But the longer this conflict with Iran drags on, the greater the likelihood of lasting economic damage.

While everyone is focused on the potential for hikes, I think the potential for even more cuts is increasing.

Those inflation measures above reflect the expected average, so they include the upcoming burst. But if you look at 5yr forward inflation expectations, they are actually falling off a cliff. That isn’t just fading tariff and oil effects, but actual economic scarring.

We have one other looming shock to contend with, and that’s a Fed Chair shock. Warsh is an inflation hawk that promised to cut rates to a president that will be a lame duck soon.

The FOMC’s current voting composition is slightly hawkish. With the labor market where it is, “slightly hawkish” means no cuts. It does not mean hikes. The market pricing in a 56% probability of a hike this year is wrong.

Rates

If the situation doesn’t improve over the weekend, I think the T10 will test 4.49% early in the week. The next major resistance level after that is in the 4.60%s.

As I noted last week, cap prices are going to remain elevated for a while. Cap vol tends to spike rapidly and then dissipate slowly.

The Week Ahead

Tons of Fed speeches and Friday’s jobs report are the non-Iranian news.

What brokers want to do to me when I talk about AI’s impact on hiring…