Father’s Day is that special weekend when you still do everything for the kids, but then add on a few extra “events” to demonstrate how much they love you. Two years ago, we went to Great Wolf Lodge for Father’s Day. It’s an indoor amusement park mixture of chlorine and screaming kids, and that fact that it’s indoors makes the screams echo that much better. Just how I want to spend Father’s Day – not only with my kids, but everyone else’s kids, too. Last year was a dance recital from 8:30am until 11pm…because, you know, they are out of school and can stay up late and work takes the summer off, too. Guess who was in charge of scheduling that? Not the dads.

Listen, I love my kids unconditionally. But I don’t love them unconditionally and uniformly. There’s variance within that unconditional spectrum. The one that clogged a toilet so badly this week we needed to call a plumber is still loved unconditionally, just a little bit less. The one that turned on the shower and went back to sleep, causing the unbeknownst-to-us clogged shower drain to overflow and then turn the living room below it into a cool waterfall pouring directly on my laptop and melting it is still loved unconditionally. Obviously. But maybe slightly less so. The 10 year old that decided to entertain himself by making a tie die shirt unsupervised and then dragging it through the house Family Circus style and getting the wet paint all over the walls is absolutely positively still loved unconditionally. But perhaps just a touch less. Temporarily.

So to celebrate, we spend even more time with these kids on Father’s Day? Pack up the family for that once a year picnic where suddenly sitting in the grass together eating sandwiches is how we spend our time? We’re like a family version eHarmony profile in motion on Father’s Day. Hiking. Holding hands. Fishing. Smiling. Grilling. Look at us – we’re active, healthy, and happy. You’d pick us, right?

You know what I want for Father’s Day? A cone of silence, my recliner, and unlimited pizza. I don’t want to hear “dad” the entire day, particularly if it’s followed by a request and/or admission of guilt about something that they just broke. Give me a chair, the US Open, and a strict “Do Not Approach” sign with two Secret Service agents guarding my space while I’m wrapped up in a warm, cozy, blanket of silence. And I mean total silence. I want to bask in the silence. That’s what I want.

But since Father’s Day isn’t about me, we don’t do that. So I needed to come up with an alternative plan of action to avoid a full day of finger painting, pottery making, basket weaving, and all the other once a year events that always seem to conveniently fall on Father’s Day. I’m getting wiser in my old age, so you know what I asked for this year? Back to back movies. Solo followed by Incredibles 2. That’s a solid five hours in dark and silence with some peanut M&M’s. I’ll probably even nap during Solo.

Father’s Day isn’t about spending time with the kids – we already do that every single day. Father’s Day is about damage control and retaining my sanity. But that’s probably just me. You probably love all those extra activities on Father’s Day and that’s why you’re a better dad than me. That’s why your kids are luckier than mine. Happy Father’s day and enjoy that picnic.

Last Week This Morning

- The 10T started the week at 2.95% and drifted lower Friday to 2.92%

- German bund ticked lower from 0.49% to 0.40%

- 2 year Treasury closed at 2.56%, up 0.04% on the week

- The Fed hiked FF to 1.75% – 2.00%

- 84% probability of a hike in September

- 56% probability of an additional hike in December

- LIBOR hit 2.08%

- SOFR jumped to 1.90% after the Fed rate hike

- Trump announced another $50B in tariffs for Chinese imports

- Goldman upped it’s Q2 GDP forecast to 3.9%

- ECB reiterated its commitment to not hiking rates until at least next summer but still suggested tapering in December

- ECB is still more dovish than our own FOMC

FOMC Decision

The FOMC hiked as expected last week and delivered a slightly more hawkish than expected tone. The Committee upgraded its assessment of economic activity and revised most of its forecasts higher. In the subsequent press conference, Powell was very upbeat about the economy.

The headline read that the Fed is now projecting an additional hike in 2018, but as we’ve discussed previously that’s really attributable to a quirk in the FOMC projections (aka blue dots). Those projections reflect the median, not the mean, forecast. This meeting, just one additional member projected an additional hike this year as compared to the March meeting. That was enough to tweak the median projection to an additional hike this year, but the average projected path really didn’t shift. Futures markets odds of a December hike only increased from 45% to 56% after the meeting.

We still fall in the camp of two more hikes this year and the Fed will only hike three more times in a true Goldilocks scenario. But whether the Fed hikes in December or March 2019, does it really matter as long as they get there?

The Fed also used the word “symmetric” again to describe its approach to inflation, meaning it will tolerate an overshoot to help compensate for the five years of below-target inflation. This implies a slightly dovish position because the Fed won’t overreact to a sudden inflation report with a 2 handle.

Couple of other takeaways:

- the Fed still projects Fed Funds to plateau just north of 3%, so floating rate borrowers shouldn’t spend too much time worried about floating rates going to 4%

- Powell will now have a press conference after every meeting starting in 2019, which he has advocated for quite some time. The market interpreted this as hawkish since it has only priced in hikes at meetings with press conferences. We think the market is overreacting a touch given Powell’s longstanding position on the Q&A.

Fed Funds Ultimate Landing Spot

The FOMC also removed the language that Fed Funds would remain accommodative for some time – this means the Fed believes rates are moving towards neutral. The Fed has hiked 1.75% already and has about 1.00%-1.25% more to go, which means we are more than halfway through the tightening cycle (58% for you math geeks).

The neutral rate is the rate at which neither promotes or restricts economic expansion. Think of it as an equilibrium rate.

The Fed has been strongly suggesting the new neutral rate is somewhere around 2.50% – 3.00%. Again, this is important for floating rate borrowers worried about their rate running away from them.

But the Fed is also projecting Fed Funds north of 3%, meaning it believes it will push rates beyond neutral and into restrictive at some point. The challenge ahead for Powell & Co is to hike enough to prevent the economy from overheating, but not so much the Fed tips us into a recession like it has done so many other times.

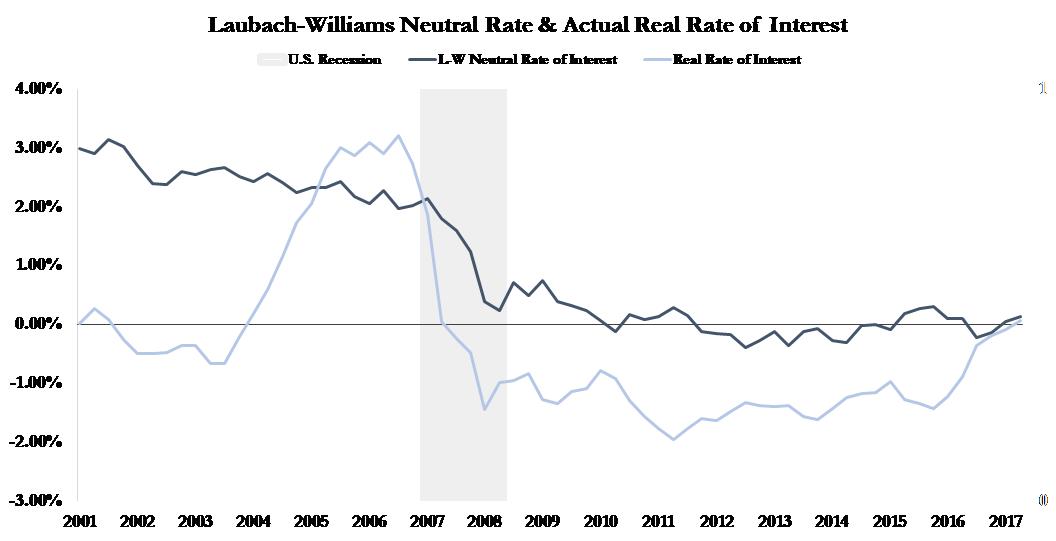

Below is a graph made by two Fed economists that tries to illustrate the relationship between the neutral rate and the real rate (rates accounting for inflation). In a perfect world, these lines would track directly on top of each other.

When the blue line (real rates) is below the grey line (neutral), then monetary policy is accommodative. That’s the environment we’ve been in since the 2008 crisis and captures not only Fed Funds, but QE policies as well.

Now that these lines are converging, it means monetary policy is neither accommodative or restrictive. If the blue line continues its trend higher, policy will shift to restrictive.

Takeaways:

- Look at how much more gradual the convergence has been as compared to 2003-2005 when the Fed hiked very aggressively. By hiking every other meeting, the Fed has done a good job of allowing rates to adjust gradually and not throwing us into a recession.

- Even if the Fed can hike five more times (and we’re not convinced they can), the end of the tightening cycle is nigh.

- Floating rate borrowers probably shouldn’t lose sleep about rates hitting 4% in the next three years and fixed rate borrowers probably shouldn’t overpay for fixed rate protection for fear of runaway rates.

Treasurys

I really crushed it a few weeks ago when the newsletter said 3.06% was the new floor on the 10 year Treasury…promptly followed by Italy experiencing a debt crisis and the 10T plunging to the low 2.70%’s.

But I also think it speaks volumes that the market has moved past that so quickly and confidently. How did we go from a debt crisis and possible end of an entire currency to the all-clear signal in two weeks?

While the issues in the eurozone will help keep the German bund low, which in turn will create a drag on the 10T, the US economy continues to diverge from the global economy.

Perhaps the bund will serve as a dampener during the slow summer months while issuance dips, but there are too many fundamental and technical factors applying upward pressure on yields for us to believe the 10T won’t break 3.00% again before year end.

- FOMC is clearly hawkish and upbeat about the economy

- Tax cuts benefits are starting to hit the system

- Congress is trying to push through spending bills now ahead of a possible government shut down in the fall and before the Democrats can take the House

- Inflation is at its highest point in five years

- Fed unwinding of its balance sheet is in full swing and set to hit $50B/mo by October

- ECB will stop QE in December and may start hiking in mid to late 2019, but signals about those will impact rates much sooner as markets price in ahead of actual change

- At some point the bund should climb and take the T10 with it

- Massive Treasury issuance to help pay for the deficit

- Testing all-time high net short speculative positions on 10yr rates

- Yields have historically dipped during the summer and then climbed again in September

- The shockingly quick recovery post-Italy suggests a very strong bias towards higher rates with quite a bit of conviction

Takeaway – the recent dip is driven by temporary fears, while the upside pressures are more permanent. The dip may stick around longer than usual given how yields tend to move over the summer, but we wouldn’t get too comfy with sub-3.00% 10yr yields.

The single greatest reason for yields to remain low in the near term is an escalation of trade war fears. If the numbers stay relatively low ($50B is not a big deal in the grand scheme of thing) and the policies are more about sending a message and less about inflicting actual damage, those fears should gradually subside (just like Italy fears). If not, however, tariffs and trade wars absolutely have the influence to drive rates lower.

This Week

Pretty quiet week on the data front, but lots of Fed speakers set to massage the message from last week’s meeting. But the real headlines will likely come from the WH policies and rhetoric.

My ten year old on Thursday, completely out of the blue, asked me where I kept my pencils at work. Such an odd question. I told him I kept them in a cup. “In a cup?! That’s it?!?” He was incredulous, as if the business can’t possibly succeed if pencils are only kept in a cup. Apparently, he’s unaware of the paperless movement. Kids are weird.

On Father’s Day, I got several heartfelt cards that were very moving, particularly from the two oldest girls. I also got a handmade painted sign that says, “you are loved”, an awesome Rick & Morty coffee mug, and shorts and a shirt (to upgrade my admittedly bland style). We also had a fun dinner without minimal (but not none) screaming and fighting.

Also, my ten year old gave me a small, hand painted ceramic jar with the names of all the kids painted on the sides. Inside was a handwritten note scribbled in pencil on a small, torn off piece of notebook paper.

“You’re the best father I could have. I hope you will use this to hold your pencils instead of a cup.”

Aren’t kids the best? I love those little….

For all the dads out there, I hope yesterday was everything you deserved.