Our quarterly webinar is Thursday this week, purposely scheduled for the day after the FOMC meeting to decrease the odds of me having to acknowledge another bad prediction. I am shockingly accurate with the benefit of hindsight. It also means you get a short and sweet newsletter this week as we prep for CPI, Fed meeting, and the big webinar. See you Thursday - we’ll have a lot to talk about.

Sign Up for the Q2 Interest Rate Webinar Here!

Last Week This Morning

- 10 Year Treasury at 3.74%

- German bund at 2.38%

- 2 Year Treasury at 4.60%

- LIBOR at 5.22%

- SOFR at 5.05%

- Term SOFR at 5.15%

- Factory Orders came in at 0.4% vs 0.8% expected.

- Initial Jobless Claims came in at 261K vs 235K expected

- The highest print since October 2021

- Eurozone is officially in a recession

Inflation

The big news this week is the FOMC meeting, but Tuesday brings us the next round of CPI. Last month’s headline CPI came in at 4.9% and is forecasted to fall even further to 4.1% this week. That would be a sharp decline since last summer’s peak of 9.1%. The m/m is also expected to drop, from 0.4% to 0.2%.

I think if we could go back to March 2022 and ask Powell, “How would you feel about CPI falling by more than 50% in one year?” he would take that all day long. Other measures are improving as well:

- Core CPI is expected to fall from 5.5% to 5.2%

- Wednesday’s PPI (considered more of a leading indicator) is expected to fall from 2.3% to 1.5%

- Core PPI is expected to fall from 3.2% to 2.9%

There’s no doubt inflation has been more stubborn than expected, but it’s moving in the right direction, right? And if Powell is right that monetary policy takes 12-18 months to work its way through the system, we are really only in the early stages of those effects.

FOMC Meeting – A Pause or a Skip?

I still expect the Fed to pause at this meeting. The market is in agreement with me, with odds of a pause at 70%. I think the real question is how hawkish is the statement/press conference?

Powell is going to portray this as a data-dependent skip rather than a pause. He’ll also reiterate that the Fed is fully prepared to hike in July (or later). This will likely be reinforced by the Summary of Economic Projections (aka blue dots) showing one more hike.

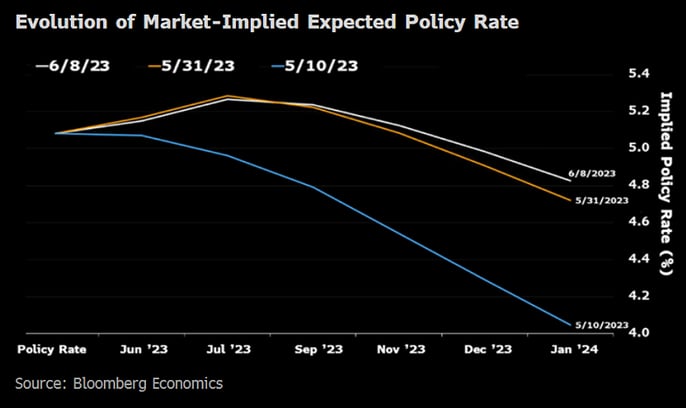

I still think they’re done hiking and this is just a tactic to buy more time to see how soft more data will come in. He can’t declare victory on inflation yet because expectations could start climbing again. Look how much progress the Fed has made on 1yr forward inflation expectations. He doesn’t want a repeat of Q1 this year.

So Powell will talk up the possibilities of more hikes to keep a lid on expectations while buying himself time to see another CPI report, another PCE report, another job report, and the next Senior Loan Officer Opinion Survey. Regardless of whether those come in hot enough to justify a hike or cool enough to justify a pause, Powell says, “See? We are data-dependent.” As we sit here today, I think there will be enough reason to not hike July 26th.

Also, there will probably be a few dissents. Bloomberg reported that across all FOMC meetings in history, only 14% have had two dissents or more. Until more cracks emerge, I suspect there will be increasing dissent at these meetings. The next time we avoid any dissents will probably be the result of a dramatically slowing economy.

Rates

Over the last month, the forward curve has shifted, with odds of one more hike in the next two months exceeding 50%. More importantly, the market has backed out two rate cuts. This is keeping one year caps expensive.

The 10T moved notably toward the high end of the range, 3.90%. I just don’t see how we break through that level unless we somehow experience strong economic growth for the next six months…and that’s not happening. The slow down is here, which means I think the 10T will grind lower in the coming months.

Week Ahead

Some might say the FOMC is the headline of the week, while others might say CPI. But my grandmother says it’s Thursday’s webinar. Don’t mess with grandma, be there.