While at NMHC this week, I was reminded of a very important lesson I learned on my first day on the Wachovia trading floor. This will surprise you, but I am known to talk trash from time to time. Not often, but every once in a while. Even more surprisingly, that sometimes gets me into hot water.

I wasn’t the typical Analyst fresh out of school. I was older because I had done my time in Army. Basic Training, Airborne, 1/75th Ranger Batt, etc. I was less scared of the trading floor atmosphere than my peers. No offense, but middle-aged dudes in khakis and rolled up sleeves weren’t exactly intimidating. But those guys had one thing that my Ranger Instructor’s didn’t have…money. I failed to account for that prior to popping off at the mouth around 5pm that first day.

We were discouraged from speaking to anyone other than the people in our immediate team. And traders were absolutely off limits. But I couldn’t help but overhear them debating about the recent ESPN Top Athletes of the Century. A passionate argument was being had between Babe Ruth and Michael Jordan. I knew it was MJ. KNEW IT. For the youngins reading this, I know this debate today can be settled in 2 seconds. But back then, the internet was still new. I decided to chime in, “It was MJ.”

My fellow Analysts shriveled, their eyes as big as saucers. Heck, even the VP sitting next to me started kneeing me, “shut up!”

“No, it was Babe Ruth,” said the head Treasury trader (for my WB buddies reading this, it was Ham).

“No, it was MJ. 100%,” I stood my ground.

“How much you want to bet?” he asked. The trap was set - I just didn’t realize it.

“Whatever you want,” I said like money didn’t matter to me.

“$100?”

Gulp.

Lee Trevino famously said, “Pressure is a $5 wager with $2 in your pocket” and I’m pretty sure he was talking about me in that moment. Suddenly, MJ wasn’t a 100% certainty. But I was stuck. Do I back down on my first day? Or stand my ground? We hadn’t gotten a paycheck yet, I had negative dollars to my name. I thought about what I could run home and sell quickly. How long could my two year old daughter go without eating? Did I have a credit card that allowed cash advances?

“Done,” I said, reciting what I had heard the traders say to each other all day long. My palms were sweaty. The room was spinning. What were his credit terms? Is my health insurance already in effect?

“Done there,” he replied, locking it in. It was official now.

Someone used dial up internet and looked it up…after the longest 45 seconds of my life…

MJ.

PRAISE THE LORD! I exhaled, trying to play like I never had a moment of doubt. The other traders lit him up for losing to a first day analyst.

He was the consummate gentleman. He walked over, pulled out a wad of hundred dollar bills, peeled one off, and handed it to me. It had never occurred to me that he actually had $100 on him, let alone thousands. No snarky comments, no stink eye, nothing. Here’s the money. Wager honored without ceremony.

I learned that a trading floor is not a place to pop off at the mouth if you aren’t prepared to put money on it. Putting money is how you express conviction in your position. Whether it’s a property acquisition or starting a software company, putting money down is how you separate the signal from the noise. If you want to know how serious someone is about their trash talk, put it to them like that trader did to me. Some dogs bark, some bite. I did this on LinkedIn last year when someone @ me that Fed Funds would go to 6%. I suggested a $10k wager to charity of our choosing, which was conveniently ignored…

On Friday, my favorite barking dog, JMo, texted me 2 seconds after the labor report to give me grief about how he is right about how strong the labor market is, “It would be so much easier to be in your camp if you were not so often and wildly wrong about labor market strength.” He continued…

“Getting much under 4% inflation is gonna be hard.” For the newer readers, JMo is the guy that started talking about inflation in 2014 and last year said, “See? Told you so.”

Then he finished with a mic drop emoji and wished me a good weekend because we are very close friends who happen to disagree.

I decided to test his conviction level. “I will bet you $XYZ Core PCE averages below 4% this year.”

Blinking dots for at least 10 minutes. He ultimately ducked and dodged while poking fun of the fact that Spotify lists my podcast as “educational”. Turns out we agree on at least one thing.

I decided to lower the target to make it easier, but my conviction level changed so I lowered the wager. “I will bet you $ABC Core PCE averages below 3% in 2024.” Because JMO doesn’t speak trader via his texts, I can’t tell if we are actually done there. But if I lose, I will honor the wager like that trader did, because I have conviction in my opinion. Knowing JMo, he will give it to charity.

My takeaway from NMHC is that a lot of smart people expressed their conviction in real estate and are waiting for that dial up connection to tell them if the correct answer was MJ or Babe Ruth. I think we get the answer soon and most people will exhale like I did on that Wachovia trading floor all those years ago. We learn a lesson we will never forget, then move on to the next cycle…

Except for those unlucky unprepared few that bet $5 with $2 in their pocket.

Last Week This Morning

- 10 Year Treasury at 4.02%

- German bund at 2.23%

- 2 Year Treasury at 4.37%

- SOFR at 5.32%

- Term SOFR at 5.32%

- Strong jobs report

- JOLTs Job Openings: 9.026M vs. 8.75M

- ADP Private Payrolls 107K vs. 145k expected

- FOMC Meeting:

- Fed held rates steady at 5.50%

- Powell: Rate cut in March unlikely

- BoE held rates steady

- BoE Governor: Does not object to the market’s current view on cuts

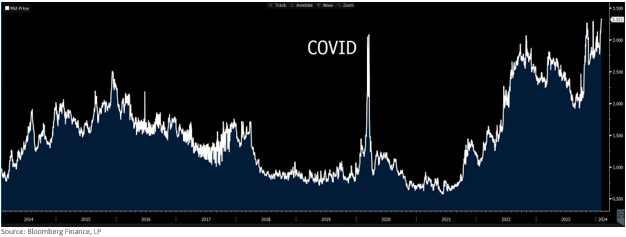

Treasury Liquidity

Treasury liquidity is strained right now, exceeding levels we briefly experienced during early weeks of the pandemic.

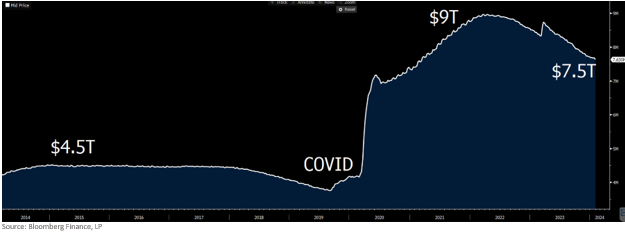

Obviously, the main culprit is the massive amount of issuance needed to fund the helicopter money. Another reason is that the Fed has been shrinking its balance sheet, sucking $1.5T in liquidity out of the market. Given the lack of liquidity in the market, I would not be surprised for QT to end at some point this summer.

While a pause in QT helps general market liquidity, it doesn’t really help the lack of liquidity in the Treasury market.

Have No Fear – Treasury Buybacks Are Here!

Back in September, the Treasury announced a buyback program for 2024 that went largely ignored. This little experiment was last conducted in 2002. You’re going to hear a lot more about this in the coming months. In essence, banks are throwing up their hands and saying, “We are full up on Treasurys!” The Treasury Dept says, “No problem, we’ll buy your ugly Treasurys if you take the cash from that and use it to buy new Treasurys. Deal?” Here’s an incredibly detailed step by step guide:

Step 1 - Treasury Dept buys less liquid Treasurys from banks

Step 2 – This frees up some capacity on bank balance sheets

Step 3 – Banks spend that money at new Treasury auctions

Step 4 – Rinse and repeat, basking in the perceived Treasury market liquidity

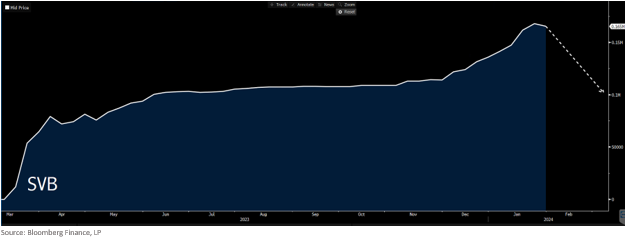

In what is undoubtedly the biggest coincidence in history, this comes at the exact same moment the Term Funding Program is ending. You know the one where the Fed is putting $160B+ in Treasurys back to the banks…

Based on the terms of the loans, banks have one year to repay the money they borrowed. That means:

- By end of March, banks will give the Fed $65B in cash and get back $65B in Treasurys

- By end of June, the same is true for an additional $45B

Do you see the problem? Banks already have too many Treasurys…and now they are about to get a bunch put back to them.

This means banks will be taking back billions of Treasurys at the same time the US Treasury needs help taking down massive issuance.

And that’s why the Treasury Dept has to roll out a buyback program to coincide with the ending of the Term Funding Program. Here’s how I will be watching the Term Funding Program play out in the coming weeks:

- If the balance drops to $100B, it suggests the banks repaid the money they borrowed last March

- Of course, this could impact liquidity and lending appetite

- If the balance doesn’t drop to $100B, it suggests that banks simply re-borrowed before the March 11th closing and pressed the reset button on the one year maturity OR the Fed gave an extension

In summary

- Treasury Liquidity is already squeezed

- Fed is about to put $100B+ Treasurys back to banks

- $1.5T of liquidity has been sucked out of the market in the last 18 months

- Treasury Dept is starting buybacks to ensure smooth auctions

We might have a liquidity problem.

What does all this mean for rates?

I don’t have the slightest clue.

But that has never stopped me from offering a guess. I just won’t put any money on it.

Rates

Some wild guesses on rates based on what I outlined above:

Rates Lower

- Improved liquidity lowers rates but only if market isn’t spooked by need for shell game buybacks just so the Treasury issuance can be absorbed

- Concerns over regional banking sector (eg, Term Funding Program balance isn’t paid down)

Rates Higher

- Markets spooked by need of buyback program

- Term Funding Program balance reduction creates more liquidity issues

The curve popped after Friday’s job report, with the front end up spiking 16bps and the 10T up 10bps.

T10 Range: 3.92% - 4.05%

A March cut is still priced at a 38% probability, likely allowing for continued inflation deceleration. On Friday, we get the first revision to the most recent CPI report.

Despite all the ink I spilled on the Treasury issuance and buybacks above, perceptions about Fed monetary policy are far and away the biggest driver of rate movements right now.

The Week Ahead

After a Fed meeting and a jobs report, this week has far fewer data points. There are, however, a ton of Fed speeches.

And today we get the next SLOOS report. Ugly/Uglier/Ugliest are the choices.