I quit. Apparently Kevin McCarthy is the only person that lost their job last week. Jobs to the moon. Rates to the moon. There will never be another real estate transaction.

Last Week This Morning

- 10 Year Treasury at 4.80%

- German bund at 2.91%

- 2 Year Treasury at 5.09%

- SOFR at 5.32%

- Term SOFR at 5.34%

- We’ll never have another recession, Bidenomics are amazing, soft landing achieved, free money for everyone, no student debt, let’s make the government as big as possible and just turn the keys over to them because they’re the real experts, this will never go bad promise.

Jobs

It’s just whatever.

Jobs are a lagging indicator, not a leading indicator. But none of that matters when the job market throws up gangbuster numbers, right?

I am skeptical of governmental conspiracy theories because I believe the government is too inept to pull them off. But this jobs thing feels weird. We go all year with downward revisions and just as everyone is catching on to the con, suddenly the revision is a huge upward gain?

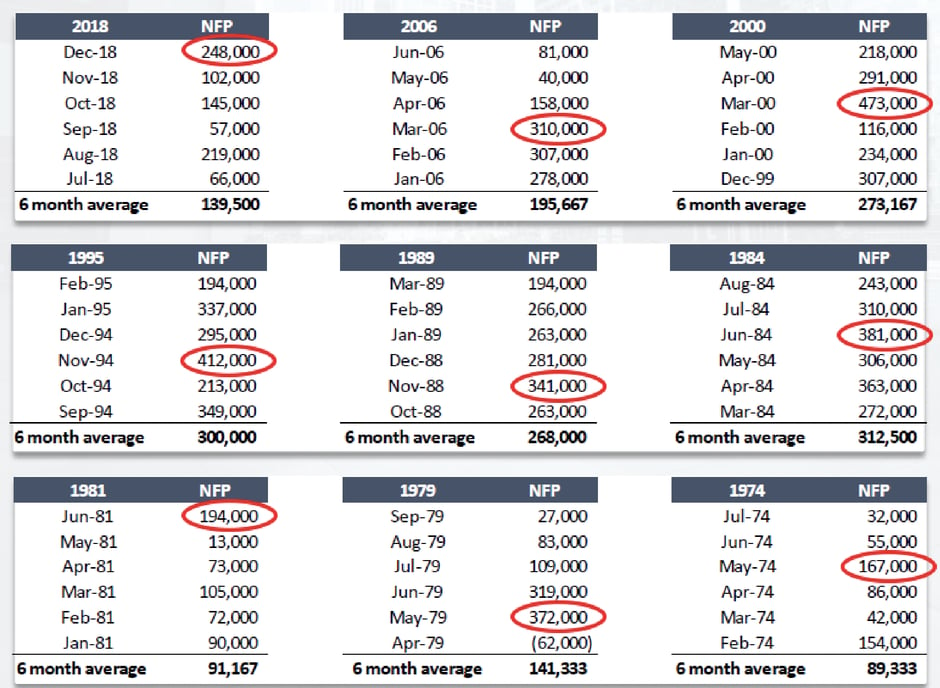

I know I’m beating a dead horse, but a strong jobs number doesn’t mean squat to me. Here are the last 9 cycles, with the monthly NFP heading into the final hike. Sometimes the highest number comes the month of the last hike.

Rate Hikes

So odds of a hike spiked, right?

Oddly enough, no. November 1st is still showing just a 27% probability of a hike. Extend that to include the December meeting and the odds increase to 42%. Not exactly the sort of response you’d expect after a gangbuster jobs report.

Remember – if the Fed believes it will be hiking at the next meeting, the Fed chatter will ramp up aggressively in the weeks ahead. The Fed’s ideal outcome at 2:30pm on November 1st is zero market reaction. That means they signaled appropriately. They will talk up a hike, driving market odds north of 60% ahead of the meeting.

The Fed goes dark the week before the meeting. That means they have two weeks to signal. If Fed-speak doesn’t drive up odds of a hike by the time Penn State is shocking the Buckeyes on October 21st, the Fed isn’t hiking.

The Wells econ team made headlines last week when they called for 2.25% of rate cuts in 2024, putting Fed Funds somewhere around 3% - 3.5%. It seems implausible right now, but this pattern repeats itself every cycle. The Fed says they have a few hikes left in them, but they don’t. They say they aren’t cutting. But they do.

In December 2018, the Fed said it would hike two more times in 2019 – pushing Fed Funds to 3.0%.

Instead, Fed Funds finished 2019 at 1.0%. A full 2% below what they expected.

I don’t know if we’ll get to 3% in 2024, but I do know the cuts will catch us, and the Fed, by surprise.

CPI This Week

Core CPI (the Washington Commanders of inflation) peaked one year ago at 6.6%. Last month it was 4.3%, and this month it’s projected to come in at 4.1%.

But the monthly data matters more.

2021 Q4 Core CPI m/m was .7%/.6%/.7%. That annualizes at 8.0%. CPI peaked at 9.1% six months later.

If it comes in Thursday as expected, the last three months would be 0.2%/0.3%/0.3%, which annualizes to 2.7%. That’s still above the target, but with enough downward momentum to be patient and wait for the hikes to work their way through the system.

As long as that monthly number doesn’t increase to 0.4% or 0.5%, I don’t think the Fed hikes.

If it does, however, the inflation hawks will have plenty of ammo to keep hiking.

This is Still Fine, Right?

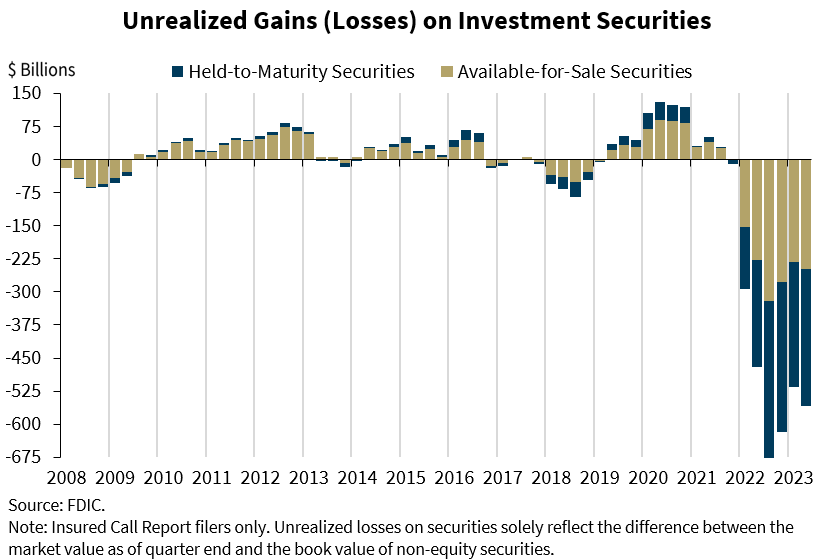

The FDIC’s most recent quarterly report revealed banks have the largest unrealized losses of Treasury holdings ever.

Remember, banks don’t have to MtM Treasurys. But that didn’t stop SVB from going under after the market ran the math and determined it would be upside down if it did have to MtM Treasurys.

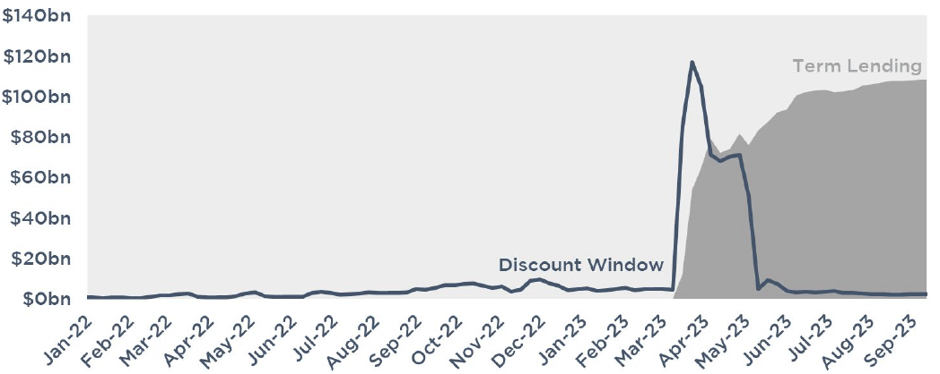

So the Fed rolled out the Bank Term Funding Program in March. Banks stopped borrowing from the discount window and switched to the new program. They post Treasurys to the Fed, and the Fed gives them one hundred cents on the dollar (instead of $.80). The more rates climb, the more those bonds drop in value. This creates more incentive to post the Treasurys to the Fed and take face value cash.

SVB would have likely survived if this program existed in February. The Fed is buying banks time to figure out their balance sheets and avoid a similar fate.

Some questions:

- If everything is fine in the banking system, why is this program still open?

- What happens in March 2024 when the program ends and banks have to give back the cash?

- What does it mean if the Fed extends the program?

In addition to extending the program, there’s one other way to lessen the losses on those bonds…

Cut rates.

Which, if you are believer in conspiracy theories, would play nicely into the 2024 election…

Week Ahead

Another week filled with Fed speeches ahead of the PPI and CPI inflation reports as well as the release of the FOMC minutes.