For the first time since December 2018, the Fed is going to hike interest rates this week. Because we will send an update out Wednesday with the market reactions, today’s newsletter is about a 60 second read.

We spend those 60 seconds examining the correlation between rising interest rates, rising commodity prices, and recessions. TLDR: we are likely headed for a recession if both keep climbing.

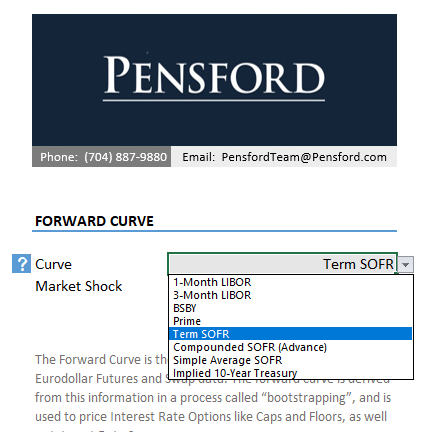

Before we dig into that, I wanted to take a moment to point out some heavily used SOFR resources we have been sending out. Here are some quick links to help navigate the rapidly evolving world of SOFR:

What’s the difference between SOFR and Term SOFR?

Where can I find today’s SOFR and Term SOFR?

On our home page!

Where can I find historical SOFR and Term SOFR?

Download our forward curve and check the second tab.

Where can I find a forward curve for various SOFRs?

That link takes you to an Excel download with a drop-down menu for various forward curves. I’m including an image here to illustrate the choices.

Last Week This Morning

- 10 Year Treasury all the way back up to 1.995%

o German bund up more than 30bps to 0.25%

- 2 Year Treasury all the way back up to 1.75%

- LIBOR at 0.39%

- SOFR at 0.05%

- Term SOFR at 0.30%

- CPI came in as expected, a whopping 7.9%

- University of Michigan Inflation Expectations

o 1yr forward: 5.9%

o 5yr forward: 3.0%

- WTI hit $124/barrel before closing out the week at $109/barrel

- I just paid almost $100 to fill up the SUV…

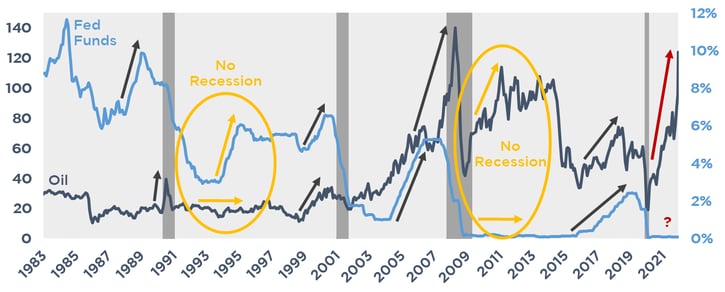

Correlation Between Rising Rates, Rising Commodities, and Recessions

When only rates or commodities rise, but not both, we can avoid a recession.

When both rates and commodities rise, we have a recession.

Check out the graph below illustrating the correlation. In the mid-1990’s, rates rose but oil did not and we avoided a recession. In 2011-ish, oil rose but rates stayed flat and we again avoided a recession.

But when they both go up at the same time, we have a recession. Even if you’ve been living under a rock, it would be impossible to be unaware of the current path of both.

This will be an enormous challenge for Powell to achieve his soft landing. I think this is a big reason the T10 hasn’t risen further – the market is worried about a recession already.

In fact, the 10 Year Treasury is just slightly below the 7 Year Treasury, and the 5 Year Treasury is just slightly below the interpolated 4 Year Treasury. Neither fit the classic definition of yield curve inversion, but there are mini-inversions occurring across the curve already.

This Week

Obviously, the Fed meeting is the major market focus. The market is pricing in 2.00% of hikes in the next twelve months and Powell has no real reason to dampen those expectations. I think there’s a chance he doesn’t expect to hike that much, but is letting the market do the dirty work for him. I think he’ll commit to being nimble and adapt to changing conditions, but avoid changing expectations:

• If he ends up hiking less, stocks rejoice!

• If he ends up hiking that much, he’s glad he didn’t try to talk the market out of it too early

News on the Russian invasion is more likely to keep volatility elevated than directly impact rates.

|

|

On a lighter note, here’s the link to our annual March Madness Upset Pool. You only have to pick 8 teams and they are weighted by seeding. There are no strings attached. No one is going to cold call you. Winner gets a cool bobbehead doll and loser gets a toilet trophy. So much easier than filling out another bracket. Click here to play the easiest bracket you’ll see this year! |