Last Week This Morning

- 10 Year Treasury spiked to 0.895% and seems poised to break 1.00%

- German bund up 17bps to -0.28%

- 2 Year Treasury up 5bps around 0.21%

- LIBOR at 0.18%

- SOFR is 0.07%

- Something about a weird jobs report?

- Daily QE purchases are down from $75B to $4B (that’s not a typo)

- The NBA is set to resume its season now that coronavirus has been eradicated and this has nothing to do with losing billions of dollars pinky swear promise…and I don’t care – give me some sports!

Jobs Report

Despite more than 12mm Americans filing for unemployment last month, the economy somehow added 2.5mm jobs in May. The consensus forecast was for a loss of 7.5mm jobs, with some high side estimates around 10mm. According to a Bloomberg survey of 78 economists, the most optimistic forecast was for a loss of 800k. This was the biggest miss since Scott Norwood.

The Good

Leisure and Hospitality + 1.2mm

Healthcare + 781k

Construction + 464k

Retail + 368k

Manufacturing + 225k

The Bad

State and Local Gov’t – 571k

Accommodation – 148k

Air travel – 50k

Transportation – 19k

The unemployment rate came in at 13.3% vs forecast of 19%. The labor force participation rate, the usual culprit for employment anomalies, actually increased.

According to the BLS report, the unemployment rate would have been about 3% higher (16%) if “employed but absent from work” respondents had been included…but still, this was way better than expected.

Some Thoughts

- 96% of the unemployed persons in March and April were those reporting a temporary layoff, which suggests a lot of them came back in May

- The number of permanently unemployed people is 1mm higher than it was prior to the shutdown. While that will undoubtedly climb, that’s only about a 1% increase in the unemployment rate

- PPP – around $550B had been used through the end of May, likely contributing to the job report.

The market interpreted this as “we’ve seen the bottom and now the recovery begins.”

If there are any fiscal hawks left in Congress, this type of report could give them cover fire to refuse additional accommodation.

10 Year Treasury Yield

This caused the 10 Year Treasury to spike, actually hitting 0.95% temporarily before settling back down around 90bps. It’s hard to believe the 10T was 2.20% just a year ago…

It looks like the 10T is about to establish a new range, with the floor being around 0.87% and the ceiling around 1.20%. The 1.00% threshold is more psychological than technical, but will likely dictate the magnitude of the upcoming moves. Unless the job data turns out to be completely fraudulent, the worst would appear to be behind us and the last month or so is likely the trough.

That doesn’t mean the 10T is headed to 2.00%, it just means the market will stop pricing in worst case scenarios. Now it can turn its attention to things like GDP and inflation, which are likely to be subdued for the foreseeable future and may prevent a bigger move upward.

FOMC Meeting – Wednesday

The Fed seems increasingly likely to rely on Yield Curve Control (YCC) to cap shorter term maturities (<3 years) while allowing the long end of the curve to “float”. The Fed will place a cap on Treasury yields out to a certain part of the curve, and intervene as needed to keep a lid on rates. The likely result?

Front End of the Curve

Rates will be anchored at the targeted level and vol will collapse. For those of you that remember mid-2012 when the Fed committed to keeping rates low for at least three years, it will probably feel like that.

- Interest rate caps should be nearly free as long as the tenor falls inside the YCC tenor

- Swaps inside the targeted tenor could make sense, but there will be little risk of floating rates climbing so is it really worth it? Maybe if the lender has a floor and agrees to remove it in exchange for the swap revenue.

Long End of the Curve

Higher long-term yields and a steeper yield curve. This would be the sort of thing that could cause the T10 to break 1.20%.

The Fed (and the federal government and the agencies) deserve credit for the intervention thus far. It will be challenging to extricate ourselves from this intervention (hysteresis cough cough), but I would rather argue about being overly reliant on accommodation than to be stuck in a Great Depression bragging, “at least we didn’t invite any moral hazard.”

Speaking of extricating ourselves from accommodation…

CARES Expiration Looming

The CARES Act has made some substantial accommodations for homeowners and renters on agency-backed loans, yet it is set to expire at the end of July. Given how successful it appears to have been at avoiding a total collapse, I would expect additional measures in the coming months.

Homeowners

About 70% of residential properties are backed by a federal agency.

Forbearance options allow for no payments for a year. Out of the gate, only 0.25% of homeowners were in forbearance. By the end of May, 8.5% were in forbearance. This money doesn’t magically disappear (although I could foresee some sort of government assistance here). Servicers can choose to tack this onto the balloon payment or at the end of forbearance. If servicers choose to tack it onto the end of forbearance, that means homeowners are going to have a pretty big lump sum due in about a year.

Renters

About 25% of rental properties are backed by an agency. The CARES Act provided a 120 day moratorium of evictions, but numerous city/states have intervened as well. We don’t need you rich landlords evicting people, creating a homeless crisis in the middle of a pandemic…

NMHC reported nearly 91% of renters made full or partial payments in May, compared to 93% a year ago. Pretty solid.

Takeaway

It certainly appears as though the rapid intervention and added stimulus has helped avoid a collapse in the housing market. One major crisis at a time please. Kudos to the government, it has handled this much better than the financial crisis.

But what happens when CARES expires at the end of July? Do we see another round of stimulus checks? Forbearance extended? How do you underwrite a deal in this environment? How much moral hazard do we risk with the continued moratorium on evictions?

At some point in the near future, we need to start letting the market shake things out. Otherwise, we are just delaying the inevitable.

Two Quick Questions

- How exactly do local governments plan on collecting taxes from landlords that can’t collect rent and are prohibited from evictions? Never mind, let’s just issue more debt and worry about it later…

- Last week, the rules for PPP changed (again). Now firms need to only apply 60% to payroll, instead of 75%, to obtain forgiveness. Additionally, they can use these funds over a 24 week period instead of an 8 week period. Will this change the dynamics of how firms layoff/furlough moving forward?

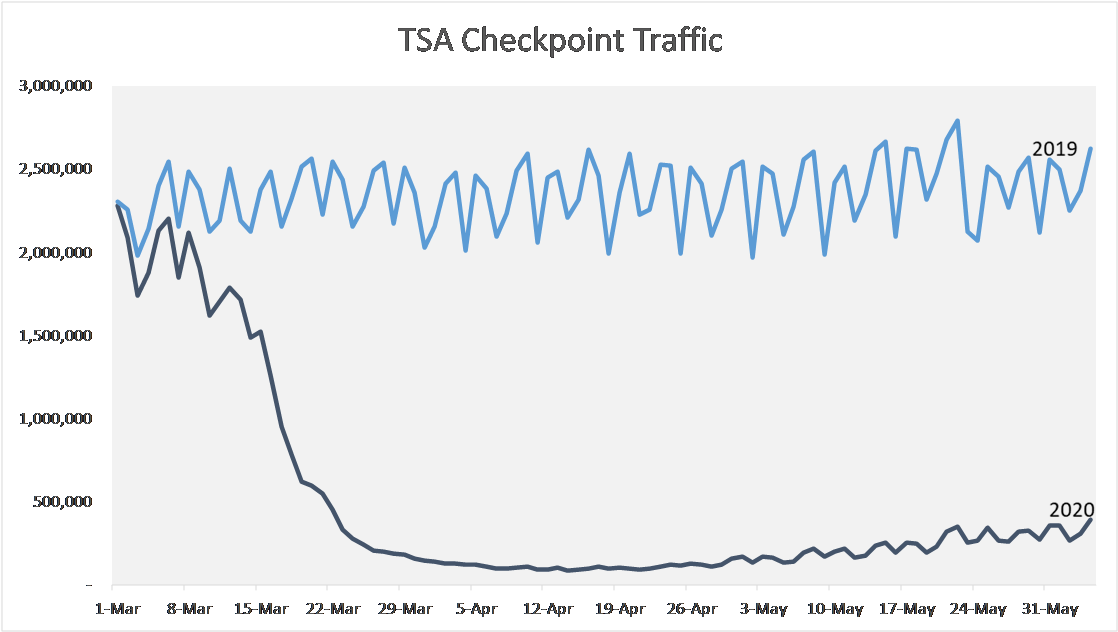

Some Lighter Data – Air Travel

In 2019, TSA checkpoints averaged about 2.25mm travelers each day.

In April of this year, that number averaged just 110k.

Over the last week, this number is back up to 323k.

The Great Thawing has begun…

Week Ahead

FOMC meeting and honestly I have no idea what else 2020 has in store for us this week.