Rates popped last week on the back of lots of commentary from Fed officials who are in favor of a patient approach even as inflation drives lower.

- Kashkari commented he believes only “two or three cuts” will take place in 2024

- Barkin isn’t “quite sold” on the idea that progress on inflation will continue as he supports being “patient”

- Kugler commented she is “optimistic” that progress on inflation will continue with help from slowing wage growth and lower rents

- Collins remains optimistic and still sees three 25bp rate cuts this year

- Logan sees “no rush” to cut rates

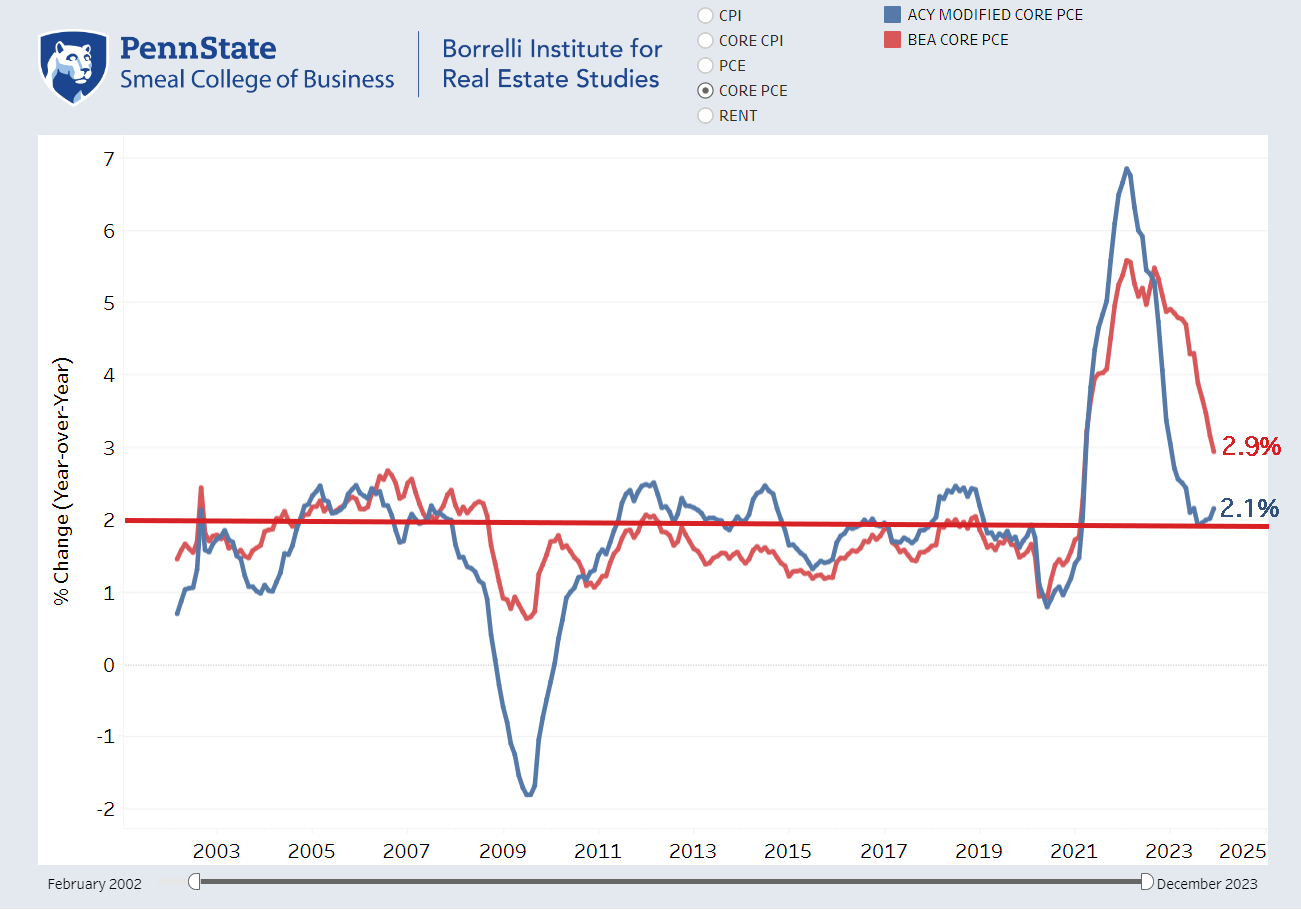

Six months ago, the Fed projected Core PCE today would be 3.9%.

Instead, it’s 2.9%.

They were off by 1.0% in just six months. I’ve never been more confident that the Fed will cut rates more than three times this year.

Last Week This Morning

- 10 Year Treasury at 4.18%

- German bund at 2.38%

- 2 Year Treasury at 4.48%

- SOFR at 5.31%

- Term SOFR at 5.32%

- SLOOS Report – Banks are expecting to tighten standards for loans and expect a deterioration in credit quality across most loan types in 2024

- Sleepy Joe would have been better off sleeping

Inflation This Week

Friday’s annual revisions were mostly a non-event, but did add to the overall disinflation story. The December Consumer Price Index was revised lower to 0.2% growth from the initial 0.3% report, granting the Fed some relief as they feared there would be a lack of meaningful change from their policy tightening.

Headline CPI is projected to come in at 2.9% this week (last month 3.4%). This would be the first 2-handle since March 2021. Inflation hawks will find something to complain about despite 2.9% being, I believe, a little below the peak of 9.1% in mid-2022.

The monthly print is projected to come in at 0.2%, which would be three consecutive months. Annualized, that’s 2.4%.

The Penn State Alternative Inflation Index suggests inflation has already bottomed out and may be starting to rebound. Remember, this index purposely addresses the lag from the shelter component. It started falling March 2022 and bottomed out a few months ago.

The official Core PCE didn’t start falling until October 2022 – seven months later than the PSU index. If it bottoms out with a similar lag, that means we could be hearing about reaccelerating inflation later this year.

People will start freaking out. “It’s the 1970s all over again!” But it’s not. It’s a simple mathematical calculation that involves capturing the prior year’s plunging data (economists call it Base Effects).

Disinflation is also a global story. ECB Member Fabio Panetta suggested the ECB needs to cut rates soon. “Macroeconomic conditions suggest that disinflation is at an advanced stage, and progress toward the 2% target continues to be rapid,” he said on Saturday. “The time for reversal of the monetary policy stance is fast approaching.”

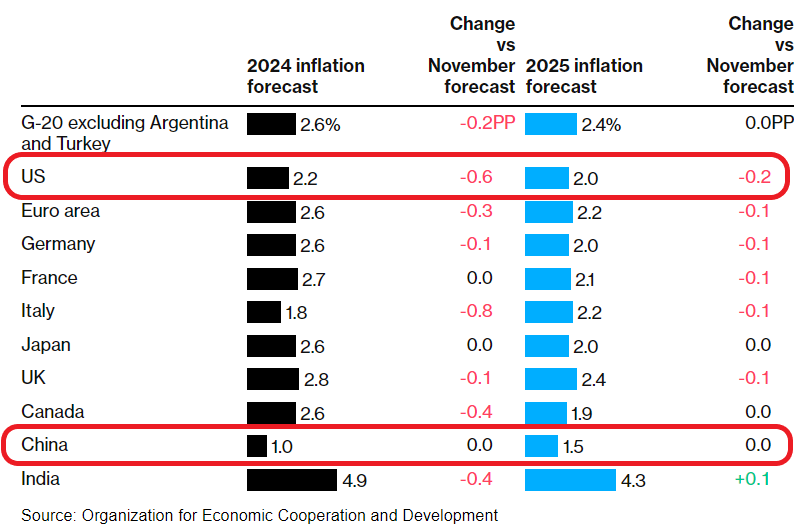

The OECD revised lower global inflation forecasts. An argument can be made that we are importing deflation from China.

Lower But Slower

As we pivot, the Fed needs a new catchphrase to replace Higher For Longer. I nominate Lower But Slower™. The Fed needs to keep up the appearance of not cutting soon, but real rates continue to move higher even as the Fed stands pat. We are approaching rarified air in terms of real rates and the economy is not going to handle it well.

The Fed says three cuts, the market says six cuts, and I say five cuts. Here are the odds for the first cut:

May: 60%

June: 92%

Interestingly enough, the market actually has higher odds that FF finishes this year below 3.75% than above 5%. With all the recent headlines about stress in CRE, it can’t get here fast enough.

The Week Ahead

In addition to CPI and PPI, there are another round of Fed speeches this week that will likely preach patience.

Or…Lower But Slower™.