Some Fairleigh Dickinson stats…

- FDU lost their conference championship, but the team they lost to is in the process of moving to Division 1 and couldn’t accept the automatic bid. That bid instead went to FDU. They weren’t even supposed to be here!

- they still had a play in game, which they won by upsetting Texas Southern

- 12 of their 14 regular season losses came to teams ranked below 200th

- that stat is less surprising when you consider they themselves are ranked 298th

- but that’s a huge improvement over last year when they were ranked 345th after only winning 4 games! 345 out of 363!

- FDU literally doesn’t have a center. Their starting power forward is 6’6” and he had to guard a 7’4” guy that will win player of the year. FDU’s starting guard is 5’8”. They are the shortest team in the tourney.

- 3x as many people picked Purdue to win the whole tournament than picked FDU to win this one game

- the 23 point underdogs were the biggest upset in March madness history

- I’m making my kids watch Purdue’s Zach Edey’s post-game Q&A. Even though he had a solid game, he refused to let his teammates take the blame for the loss. Unsolicited, he jumped in after a teammate’s response to make clear that last play did not cost them the game and then highlighted his own deficiencies.

Last Week This Morning

- 10 Year Treasury at 3.44%

- German bund at 2.12%

- 2 Year Treasury at 3.82%, down 120bps in a week

- Cap liquidity evaporated because we couldn’t go a day without a 25bps+ swing

- LIBOR at 4.78%

- SOFR at 4.57%

- Term SOFR at 4.76%

- CPI data largely came in as expected

- The annual number showed improvement from 6.4% to 6.0%

- But the core monthly data showed a reversal

- PPI data came in much cooler than expected

- This is considered more of a leading indicator

- Philadelphia Fed Manufacturing Index came in at -23.2 vs-15.6 expected

- UMICH 5 Year Inflation Expectations came in at 2.8%

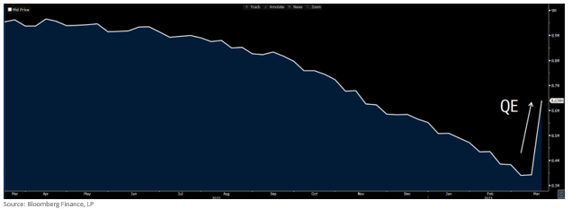

- Despite the plunge in rates, cap prices were actually up because liquidity ceased to exist

- We Are!...a Basketball School!

Goodbye QT, Hello Again QE

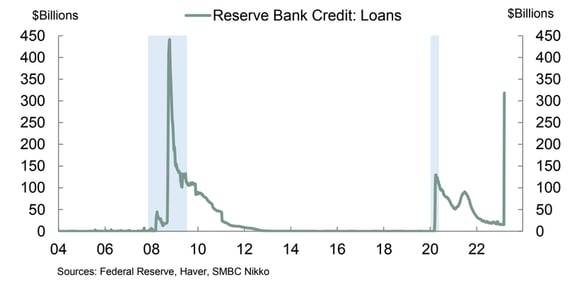

The Fed’s balance sheet surged by $318B last week following the creation of the Bank Term Funding Program. Here’s the Fed Balance Sheet reversal of QT.

Specifically, loans to banks surged to the highest level since 2008.

So the banking system is under incredible pressure and we’re gonna hike again this week? Cool……

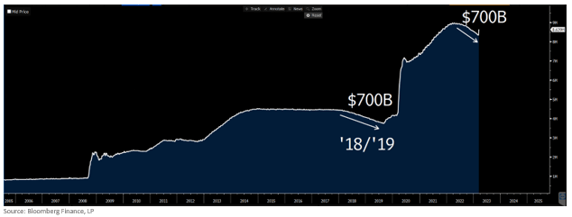

Also, I’m not sure we will ever be able to unwind the Fed’s massive balance sheet. We have no precedence of the system surviving even $1T in reduction, how are we going to close to $0?

FOMC Meeting – Wednesday

There are basically two camps right now.

- Hike 25bps to 5.0%

- The battle against inflation is not yet done

- Not hiking implies the massive intervention wasn’t enough to ensure stability

- Pause, keeping FF at 4.75%

- Are you crazy? The banking system is under the most strain since 2008 and we’re piling on?

- You can send lots of signals about hiking in May and beyond but want to get markets the opportunity to stabilize

- Time, more so than another 25bps, is needed to beat inflation

The market currently has a 62% chance of 25bps. That feels about right to me, even though I fall firmly into Camp 2 (don’t hike).

Interestingly enough, there’s still a 26% chance of a hike on May 3rd, which would push FF to 5.25%. But then the bottom falls out, with a zero percent chance of Fed Funds being at 5% or higher by September.

There’s also a 66% probability that FF finishes the year at or below 4%.

For those that believe SVB was largely a one-off outlier and we will return to our normally scheduled programing, I ask, “Can you tell me a time when markets reacted this violently that turned out to be an overreaction?”

I can’t.

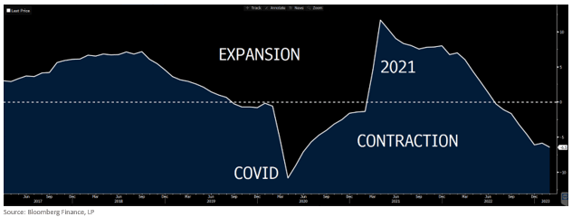

And using forward looking data, like the Leading Indicators Index, suggests the economy was already downshifting materially before the SVB collapse.

What Toilet Paper and Vol Have in Common

Despite front end rates plunging more than 100bps, cap prices actually went up. And that’s assuming you could get a quote at all. There were banks telling us flat out they would not trade last week. We got a bunch of caps done, but it wasn’t easy.

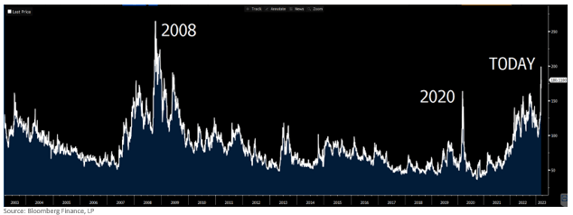

Looking at rate volatility, it’s not hard to understand why. The only other time rates have been this volatile was in 2008.

When you buy a cap from a bank, that cap trader has to hedge two components:

- Rates

- Vol

You already know the rates part. Volatility, or “vol” if you want to sound cool at a cocktail party, is bought and sold just like Treasurys or gold stocks.

To hedge the vol component of your cap, they need to buy vol in the market. During crazy periods like last week, the value of vol spiked. That would translate into a nice profit for the seller of that vol. They make money, the trader you are dealing with hedges their position, and you get your cap. Everyone wins.

But right now, traders don’t want to sell their vol holdings, no matter how attractive the profit looks. They are worried about survival, not making a little bit of profit this month. Those vol holdings are protecting them from getting steamrolled right now. This leads to vol hoarding.

Remember how in 2020 you couldn’t get toilet paper? Some selfish people (not me), bought as much as they could and just stockpiled it. Those same people (again, not me) weren’t interested in selling it for a profit on Ebay, they just wanted it for survival. That hoarding caused toilet paper markets to stop functioning properly until the logjam cleared. By the time those hoarders (definitely not me) were willing to sell toilet paper, markets had largely returned to normalcy.

Last week, vol hoarders refused to sell at any price. This meant the cap provider had no way to hedge the cap you were trying to buy. This led to:

- Refusal to trade, particularly on bigger caps

- Cap providers self-insuring by charging you so much extra it provided enough cushion to get them by until markets calmed

By Friday, vol markets had begun to settle and banks were mostly open for business. But if, like me, you assumed cap prices would be down, you were disappointed.

As/if markets settle further, cap prices should come down to reflect the much lower rate trajectory (unless that reverses course as well). I doubt vol settles ahead of the FOMC meeting, but maybe by week end?

In a totally unrelated story, if you want the deal of a lifetime on toilet paper, please visit my Ebay site…

Week Ahead

FOMC on Wednesday. The banking system on the verge of collapse. Penn State winning an NCAA tourney game. March Madness indeed.