Last Week This Morning

- 10 Year Treasury at 3.73%

- German bund at 2.37%

- 2 Year Treasury at 4.75%

- LIBOR at 5.15%

- SOFR at 5.05%

- Term SOFR at 5.08%

- For about 12 hours there, it looked like Putin was done. Even though he bought himself some time, at a minimum this weekend’s events have to be the beginning of the end of the invasion of Ukraine.

- Also, how long before Prigozhin has an “accident”?

Powell’s Testimony

Twice a year, the Fed chair testifies to Congress and tolerates mind-numbing questions from people about as qualified as me. Powell spent Wednesday and Thursday last week in these sessions and unsurprisingly, he had lots of questions about a potential banking crisis and how the Fed missed the submarine boat.

Since this is a rates newsletter, I’m going to focus on his remarks about more hikes and the labor market, which he continues to hold up as Exhibit A for why more hiking may be necessary. Turns out there are people way smarter than me that also disagree.

An economist with the San Francisco Fed, Adam Shapiro, recently published a study entitled, “How Much Do Labor Costs Drive Inflation?”

Tight labor markets have raised concerns about the role of labor costs in persistently high inflation readings. Policymakers are paying particular attention to nonhousing services inflation, which is considered most closely linked to wages. Analysis shows that higher labor costs are passed along to customers in the form of higher nonhousing services prices, however the effect on overall inflation is very small. Labor-cost growth has no meaningful effect on goods or housing services inflation. Overall, labor-cost growth is responsible for only about 0.1 percentage point of recent core PCE inflation.

Dr. Shapiro concludes, “Overall, the results highlight that recent labor-cost growth is likely to be a poor gauge of risks to the inflation outlook.”

If the Fed continues to obsess over the perceived tightness of the labor market, it will mistakenly keep hiking for the wrong reasons. The backside of the curve will be that much steeper to compensate for overdoing it on this side of the curve, but it will be longer before we get there.

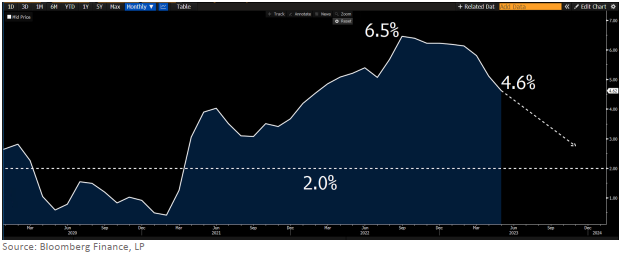

Not surprisingly, Powell didn’t reference this recent study in his testimony. Nor did he address the improvements in supercore inflation, that measure of core inflation Powell likes because it tries to account for the lag in housing costs.

Last fall, Powell spent a lot of time convincing us we should be ignoring the falling prices of goods and focus on services since those are driven by labor costs. In fact, he said supercore inflation, "may be the most important category for understanding the future evolution of core inflation.”

Given his hawkish comments, supercore must look worrisome, right?

Not so much. In the last eight months, it has fallen nearly 2%. It is obviously too high, but does it really suggest the Fed needs to keep hiking? If it keeps falling at the same pace, supercore inflation will be below 3% by year end.

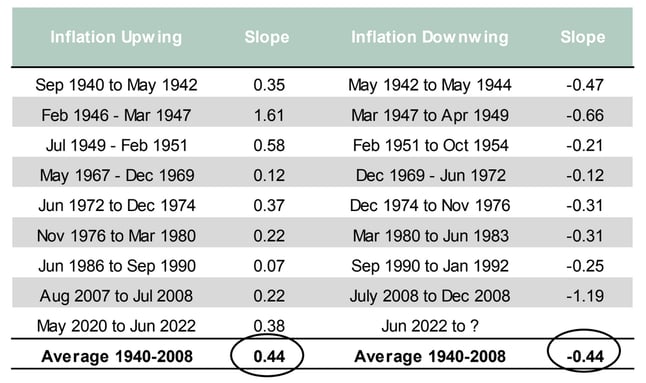

That assumes supercore keeps falling at the same rate, but what are the odds of that? SMBC recently put out a great research piece that showed inflation tends to fall at the exact same pace it had climbed. So far, inflation is falling at the same pace it had climbed.

And yet, Powell suggested that two more hikes are likely. “Now we’re moderating that pace, much as you might do if you were to be driving 75 miles an hour on a highway, then 50 miles an hour on a local highway, then as you get closer to your destination, you try to find that destination — you slow down even further,”

Or you slam into a bunch of red brake lights.

Right now, markets are pricing in a 72% probability of a hike on July 26th, but just an 11.5% probability of another hike after that.

More importantly for cap costs, the odds of Fed Funds below 5% by year end are just 6.6%. Six week ago, those odds were nearly 100%.

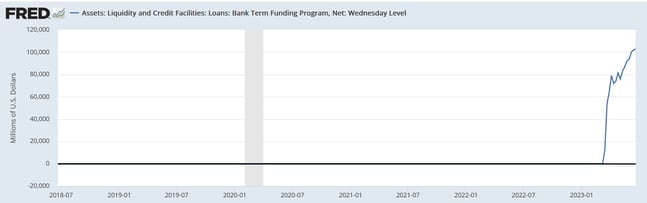

Oh, and about the banking crisis? According to Powell, everything is stable, and yet the emergency lending program to banks just crossed the $100B threshold…

I’m always amazed by how much stability a $100B can provide…

Week Ahead

Tons of data this week, headlined by GDP and Core PCE. That inflation report could lock in the odds of another hike in July.