On April 27th, I wrote a newsletter entitled, “What do Georgia and Sweden have in common?”1 Something about shutdowns (and to a lessor extent, masks) bothers me at a deeply intuitive level. I am biased towards Sweden’s approach and am rooting for them to overcome covid in the hopes it leads to a more reasonable approach here. That’s my disclaimer. Everything that follows should be viewed through my lens of rooting for Sweden like it’s Nick Foles running the Philly Special (41-33 Never Forget). Plus, my wife is Swedish.

On July 7th, the New York Time’s headline read, “Sweden has become the world’s cautionary tale.”2

Two weeks ago, CNN ran an article entitled, “Sweden pays human and economic cost for not locking down.”3

On July 21st, USA Today published an opinion piece by 25 Swedish doctors, “Sweden hoped herd immunity would curb COVID-19. Don’t do what we did. It’s not working.”4

This one just came out Saturday, “Sweden’s unorthodox response to COVID-19: What went wrong?”5

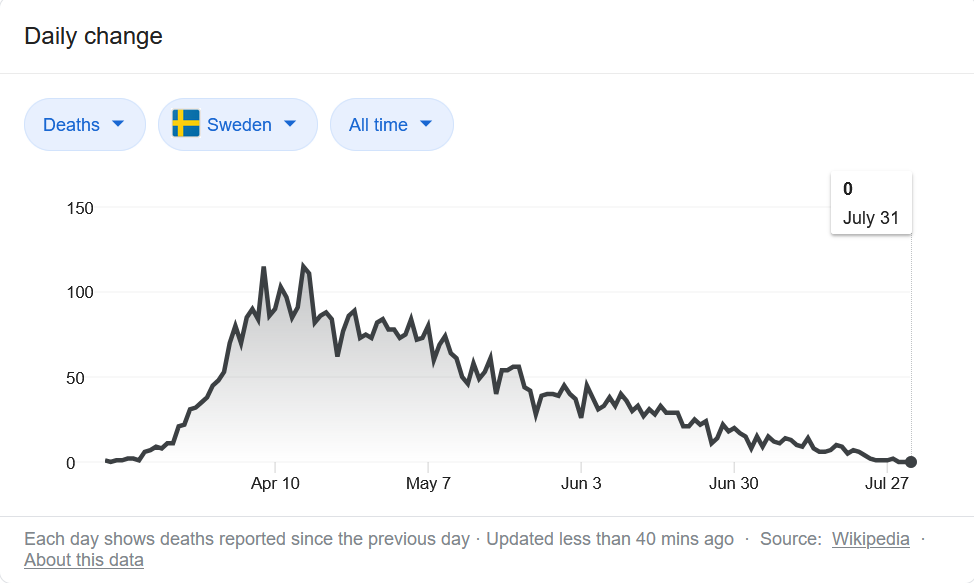

This most recent one was the first story to pop up when I Googled “Sweden Covid”. I honestly haven’t been staying on top of Sweden’s daily numbers, so my first thought was they must have had a brutal July. I was bummed. I clicked on the Google graph of Sweden deaths, preparing for the worst…

Zero.

I actually went to other sites to double check because I assumed it must be wrong. But it wasn’t. Sweden had zero deaths on Friday. And has been averaging less than two deaths a day for over a week now.

Surely there must be articles out there like, “Sweden reverses course, shut down saves lives.” Or, “Sweden requires masks and deaths fall to zero, so there!” Nope, nothing.

In fact, that search led to a Fortune article from last week quoting the Swedish lead epidemiologist Anders Tegnell, “With numbers diminishing very quickly in Sweden, we see no point in wearing a face mask in Sweden, not even on public transport.”6 Good luck saying that in America right now Anders.

Hello, rabbit hole…

Wait wait wait, don’t go! I’m not going to drag you down that rabbit hole with me. Just take a peek down the hole for a moment.

Wikipedia tells me that the University of Uppsala is the oldest university in Sweden and generally considered one of the top 100 universities in the world, just ahead of Duke and about 95 slots behind UNC (I can hear the Dukies furiously googling world rankings).7

Researchers at the University of Uppsala published a report in early April forecasting Swedish deaths, largely as a critique of the country’s approach.

Our model predicts that, using median infection-fatality-rate estimates, at least 96,000 deaths would occur by 1 July without mitigation. Current policies reduce this number by approximately 15%, while even more aggressive social distancing measures, such as adding household isolation or mandated social distancing can reduce this number by more than 50%.8

So at least 96,000 deaths without mitigation? And Sweden’s then-current policies (eg, bans on gatherings of more than 50) could reduce that 81,000 deaths?

Actual Swedish deaths as of July 1? 5,514.9

Well, I’m sure the researchers allowed for some uncertainty in those forecasts?

Our model for Sweden shows that, under conservative epidemiological parameter estimates, the current Swedish public-health strategy will result in a peak intensive-care load in May that exceeds pre-pandemic capacity by over 40-fold, with a median mortality of 96,000 (95% CI 52,000 to 183,000).

Even allowing for a two standard deviation miss, the low-end forecast was 52,000 deaths. The real number was just 10% of that.

How can an estimate be so wrong?

I have no clue. But they are being used to make policy decisions as if they are foolproof.

In this day and age when we have access to an insane amount of data, let’s not forget that forecasts are just forecasts. We’re all suddenly amateur statisticians, none more guilty than me.

Can’t we have a reasonable discussion (and minor celebration?) around why Sweden is doing so well? Are we potentially missing an opportunity to improve our own approach? Isn’t this a good thing? If you want me to consider why Vietnam is doing so well, can you also consider why Sweden is doing so well?

Are the countries we believe are doing the best in the world actually doing the best? Or are they doing the best using the approach favored by our preferred media outlet? Echo chamber and all (that’s a critique of both sides, Fox has too many examples of questionable journalism to even cite). I seek out Sweden. You seek out Switzerland. Maybe we learn from each other.

And if you’re thinking, “Sure, but Sweden is different than the US,” I agree 100%. Just like NC is different than CA. And NY is different than TX. A targeted approach makes all the sense in the world. Why is the MLB cancelling games when 25 year old professional athletes have as little risk as anyone out there? If they were being played by 70 year olds with diabetes? Sure. But they aren’t.

But why are we treating every person the same when the coronavirus isn’t?

Last Week This Morning

- 10 Year Treasury closed at an all-time low of 0.528%

- German bund -0.52%

- 2 Year Treasury also set an all-time low of 0.10%

- LIBOR at 0.15%

- SOFR is 0.10%

- Q2 GDP contracted the most in history, -32.9% (yet somehow “beating” forecasts of -34%)

- Consensus forecasts for Q3 are +18%

- Atlanta Fed GDPNow forecasts Q3 GDP as + 11.9%

- The FOMC meeting was as ho-hum as expected as it committed to keeping rates low forever the foreseeable future and extended emergency lending programs through year end

- Another 1.4mm Americans filed for unemployment last week

- Core PCE (Fed’s preferred measure of inflation) came in at -1.1%, reminding everyone that is concerned the stimulus will lead to inflation that we can worry about that later

- Powell said as much in the post-meeting Q&A, calling covid, “fundamentally a disinflationary shock”

- This means negative real rates have arrived in the United States!

- Apparently the MLB had gone all-in on the “we won’t have a single case but if we do we will cancel” strategy

- Bill Belichick is definitely not encouraging players to opt out so that the Pats can tank in order to get Trevor Lawrence

- TikTok gets banned just as I perfect my dance moves…classic 2020

That Stimulus Tho…Or Not

At the FOMC on Wednesday, Powell said, “on balance it looks like the data are pointing to a slowing in the pace of recovery.” That does not bode well for the standoff between Republicans and Democrats. While Congress can retroactively apply, each additional week will create ripple effects into the future.

As we highlighted last week, June consumer spending was only down 0.6% from pre-covid levels. That’s because the stimulus substituted as payroll. Lack of stimulus will have an immediate effect on this and dampen any potential recovery.

It also risks weighing on consumer sentiment. Following the financial crisis, it took seven years for consumer sentiment to return to pre-crisis levels. We are likely to experience a lengthy climb back, and delaying stimulus that helps pay the bills when the government is keeping businesses closed will only deepen the downturn.

Negative Rates

In May we discussed why interest rates could go negative in the US.

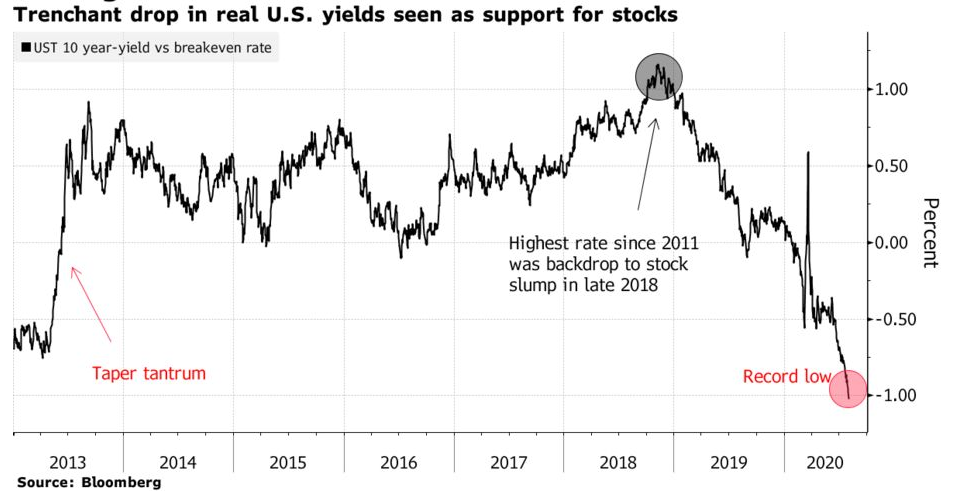

Once adjusted for inflation, real rates are already negative (although not as low as March).

When compared to the 10 Year Breakeven rates, real rates are at historical lows.

We are likely dealing with low (and negative) interest rates for a while.

But I’ve Been Wrong Before

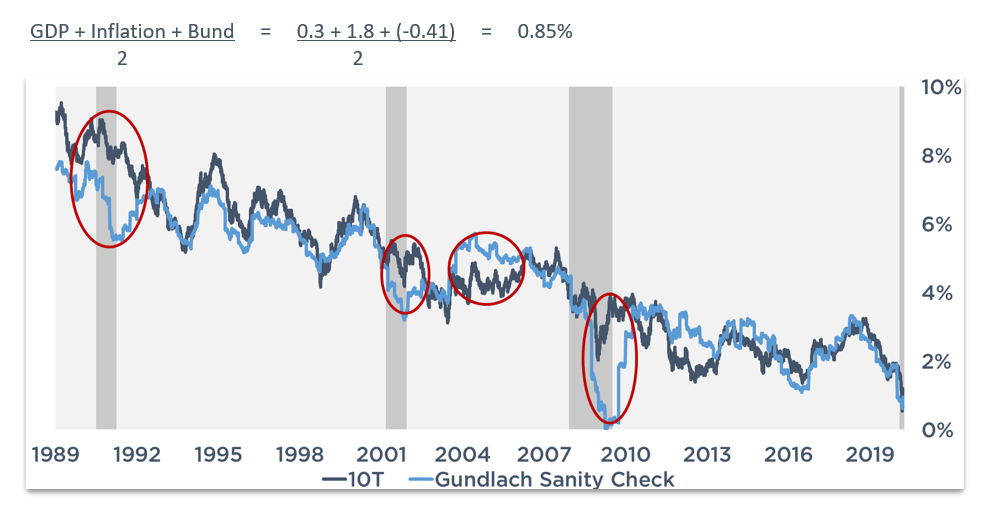

Remember that nice sanity check for the 10T we use from DoubleLine’s Jeffrey Gundlach? It works really well most of the time, except during periods of extreme GDP swings (usually a recession). In the graph below, the dark blue line is the actual 10 Year Treasury and the light blue is his calculation. Pretty correlated.

During the last three recessions, it took about 18 months for the relationship to return to normal and his sanity check to have some value again.

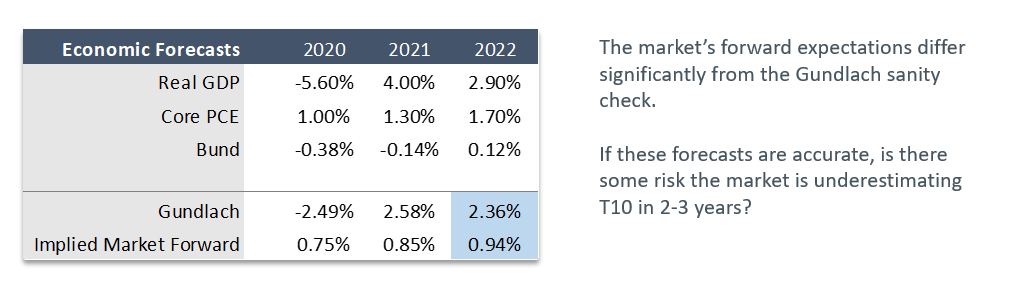

In the boxes below, we take a look at forecasts for the three components of his sanity check. As you will see, his math suggests the 10T should be at -2.49% (not happening) this year and 2.58% next year (never say never, but…that’s probably not happening).

But, stretch that timeline out 18 months and look at the 2022 forecasts. His math suggests a 2.36% 10 Year Treasury, while bond futures suggest 0.94%.

With a Fed committed to keeping rates low until we are well into the recovery, the 10 Year Treasury is likely to remain low for the foreseeable future.

But I can’t shake this feeling that the market is underestimating long term rates 2-3 years from now.

Not a 5.00% 10 Year Treasury, but 2.0%? Or 3.0%? Just something higher than 0.94%.

Week Ahead

Stimulus (or lack thereof) will be the biggest headlines of the week. The jobs report is due out Friday, with a consensus forecast gain of 1.5mm jobs. With so much volatility in the data, it’s tough to put too much stock in these releases right now.

Sources

- https://www.pensford.com/what-do-georgia-and-sweden-have-in-common/

- https://www.nytimes.com/2020/07/07/business/sweden-economy-coronavirus.html

- https://www.cnn.com/videos/world/2020/07/20/sweden-coronavirus-covid-19-economic-pain-black-pkg-intl-hnk-vpx.cnn

- https://www.usatoday.com/story/opinion/2020/07/21/coronavirus-swedish-herd-immunity-drove-up-death-toll-column/5472100002/

- https://www.aljazeera.com/programmes/talktojazeera/2020/07/sweden-unorthodox-response-covid-19-mistake-200730093401428.html

- https://fortune.com/2020/07/29/no-point-in-wearing-mask-sweden-covid/

- https://en.wikipedia.org/wiki/Uppsala_University

- https://www.medrxiv.org/content/10.1101/2020.04.11.20062133v1.full.pdf

- https://www.statista.com/statistics/1105753/cumulative-coronavirus-deaths-in-sweden/