Overview

Over the past couple years many lenders have allowed borrowers to defer the purchase of a cap until SOFR hits a certain level, a “springing cap”. For example, the lender sets a trigger on SOFR at 2.00%. If SOFR exceeds 2.00% for five consecutive business days, the borrower must purchase a cap at a pre-determined strike through the initial term of the financing.

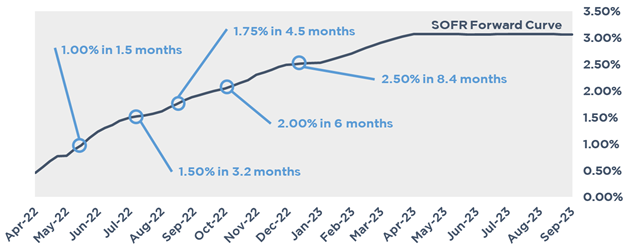

Many borrowers have appreciated this provision because it avoids a perceived unnecessary expense to fulfill the lender’s hedge requirement at closing. However, the Fed and market have made a quick 180, with y/e 2022 rate expectations jumping more than 2.00% in just six months. This means that many springing caps are about to be “sprung”.

Current Environment

SOFR is currently 0.47%. The Fed has opened the door for 0.50% rate hikes, which the market gives a 94% probability of occurring at the May meeting and 77% probability of again in June.

Many borrowers have springing cap requirements that are triggered at 1.00%, 1.50%, and 2.00%. Based on current market projections, all of these are expected to be breached before year end.

If you’ve got a springing cap requirement with the trigger set at 2.50% or less, you may have to purchase that hedge at some point this year.

Many borrowers are now asking, “when is the best time to buy my cap?” Should they move forward now while SOFR is low? Or are they better off waiting until they have to buy?

Wait or Buy?

Here is an example of a borrower that closed on a financing six months ago that must buy a cap through the initial term (Oct 2024) if SOFR exceeds 2.00%.

Loan Amount $50,000,000

Effective Date 10/15/2021

Maturity Date 10/15/2024

Floating Rate Index Term SOFR

Borrower must purchase a 2.50% cap through maturity on the full loan amount if SOFR reaches 2.00%. The cost of that cap today - $930,000.

Assuming rates follow expectations and similar volatility, in 6 months the cap is expected to be $815,000, or about $115,000 cheaper.

This is because cap costs increase exponentially with term as the market becomes increasingly uncertain of the path of rates the further out it looks and charges you a premium for that uncertainty. In this scenario, you’re comparing a 2.5yr cap today against a 2yr cap in 6 months. By waiting to buy, some of that uncertainty premium has the opportunity to bleed off.

But what happens if things get worse? Holding everything else constant, rates would need to increase an additional 0.16% above current expectations before you wish you had bought the 2.5yr cap today.

One other thing to consider is how market volatility has impacted cap costs. Uncertainty premium climbs in volatile market environments, and by some measures, short term volatility has exceeded levels seen during the peak of the Great Recession.

To illustrate the impact on pricing, we’ve broken out how much of that 2.50% cap is attributable to uncertainty premium below.

Economic Value $403,000

Uncertainty Premium $527,000

Total Cost $930,000

By waiting to execute, there is a chance of volatility easing which could also help lower cap costs. However, the inverse is possible as well.

Conclusion

Based on the Fed’s latest messaging and current market projections, it’s less “if” many requirements will be triggered and more “when”.

If you have a springing cap that you’d like to run this analysis for or begin monitoring the cost on, please don’t hesitate to reach out. We’re happy to set clients up to begin receiving monthly updates on rate movements and cap pricing to enable them to be in a position to move forward quickly if/when they chose.

If you're a LoanBoss user, you can set alerts to go off on deals with springing cap requirements so you know when your floating rate is about to cross that threshold. If you're not a LoanBoss user, why not? Check it out here.