I lived in Dilworth for a long time, a suburb of Charlotte that was originally built for WWII veterans returning home. It was initially very small homes and correspondingly small lots. As Charlotte exploded, the homes were torn down and replaced with McMansions.

The streets were never designed for families with three or four cars and certainly hadn’t anticipated the giant SUV/truck craze. My chief complaint of Dilworth was how much of a hassle it was to get around, even on my own street. With all the cars lining the streets, it was a constant game of, “ok, you go no wait is it my turn ok you are going but what about the 3 cars behind you?” But I dealt with it because I loved the area.

Once I decided to move to the sticks, however, my resentment grew stronger. It was like a countdown clock. “Only 30 more days of dealing with this.” As my moving date approached, the tiny streets were all I noticed. I was increasingly frustrated having to wait to navigate around a parked car. I would get agitated with even a 10 second pause, dreaming of the day I would escape this hassle.

I am starting to feel the same way about COVID safety precautions. I’ve been vaccinated. Everyone in the family has been vaccinated. We’re rapidly approaching the point where everyone that wants to be vaccinated will be vaccinated. After that, why should I keep wearing a mask? Why should indoor events have limited capacity? Why are firms working remotely through year end?

I wonder how much we will tolerate as we re-open? Will we push back when preventive measures are about appeasement rather than actual safety? Or will we be conditioned to just accept the new “precautions”? Will temporary measures become permanent? Why do I still take my shoes off to go through TSA security again?

There’s a light at the end of the tunnel. Let’s finish this and then get back to normal.

Last Week This Morning

- 10 Year Treasury fell back to 1.65%

- German bund up 3bps to -0.30%

- 2 Year Treasury down to 0.15%

- LIBOR at 0.11%

- SOFR at 0.01%

- PPI came in higher than expected, suggesting producers are paying more, but can they pass this along to the consumers?

- ISM Services Index came in at a record 63.7

- Mortgage applications fell for the 5th week in a row

- CA Governor Newsom announced a potential re-opening date of June 15th and in no way was this influenced by his potential recall

- Indeed reported a 16% increase in job listings as compared to February last year

- My family found the American Kennel Club Agility Championship (where dogs run an obstacle course) infinitely more enjoyable than the Baylor drop-kicking of Gonzaga

- Gonzaga consolation prize was honorary induction into the Big 10 Chronically Overrated Club

- Anecdotal evidence with no supporting evidence (the kind of stuff I hate)

- My wife flew to NYC on Thursday and there were 25 people on standby

- Every person at our company that plans on being vaccinated has been vaccinated, much sooner than expected.

- One employee that was vaccinated last month ate out with his family for the first time in a year

- What a perfect time for Matsuyama to win the Masters. I was half-jokingly going to add, “Then again, the Americans that would benefit the most from watching an Asian win the prestigious green jacket probably aren’t big golf fans,” but I’m not sure that’s a true statement. Unfortunately, it’s my own demographic that has a lot of personal growth to do.

That Stimmy Tho

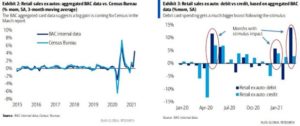

Retail sales is poised to have one of its best months ever. The consensus forecast is 6.5%, but BofA economists are projecting a print north of 11%. The all-time high was May last year following the April shut down.

This forecast heavily incorporates spending on BofA credit cards, which surged 67%. In other words, the BofA team has some insight on how consumers are spending that helicopter money stimulus.

From the same report, BofA also noted how spending is transitioning to brick and mortar and away from online. People want to get out and about.

All of this spending is likely to contribute to one of the strongest quarters on record. Consensus forecasts keep moving higher, with firms like JPM jumping in to call for 9.5% Q2 GDP.

CPI this week is expected to come in at 1.5%, but only because that stimmy effect hasn’t had time to show up in the numbers. Inflation will jump in the coming months, but the Fed will work hard to reassure everyone that the increase is temporary and not to expect a hike anytime soon.

10 Year Treasury

Supply, tapering, and inflation. Those are driving rate swings more than economic growth.

- Supply – the government already has to fund a $3.8T deficit with about $3T in supply. If Biden’s infrastructure plan can’t be paid for through tax hikes, supply could increase. Otherwise, the infrastructure bill is net neutral here.

- Tapering – the Fed is signaling a start to tapering in early 2022. Strong GDP could potentially increase the odds of a sooner-than-expected tapering announcement, but I don’t think so. The Fed won’t veer off course just because the stimmy artificially pumps up spending for a short period of time.

- Inflation, or inflation expectations, will absolutely drive rates. In the coming months, there is bound to be headlines of price spikes. But will it persist? The market is pricing in a “yes” to that question. If those fears fail to materialize (like they have over the last 20 years), the market may need to back that risk out and rates retrace.

Jaime Dimon said, “I have little doubt that with excess savings, new stimulus savings, huge deficit spending, more QE, a new potential infrastructure bill, a successful vaccine and euphoria around the end of the pandemic, the US economy will likely boom. This boom could easily run into 2023 because all the spending could extend well into 2023.”

Thus far, discussions around an infrastructure bill, corporate tax hikes, and herd immunity have been theoretical. But at some point in the coming months, they will become more concrete. As that dialogue heats up, volatility may increase and we may experience more swings (up or down).

Week Ahead

Earnings season kicks off. CPI. Retail Sales.