Random thought of the day – the Fed’s most recent Summary of Economic Projections puts the Unemployment Rate at 4.5% at year end. That means they project about 1.5mm Americans will lose their job by year end.

That’s an average of 167k job losses per month…and that assumes we start losing jobs this month. So either they are dreaming…or the wheels are about to fall off.

Oh, and they are calling for a recession in the back half of the year…while still hiking.

At some point I have to wonder – do even they buy what they are selling? Is the Fed using some new FedGPT AI to craft messaging?

Last Week This Morning

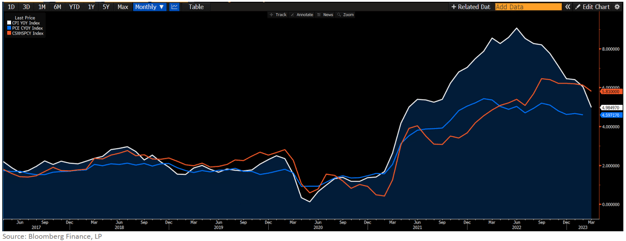

- 10 Year Treasury at 3.51%

- German bund at 2.43%

- 2 Year Treasury at 4.09%

- LIBOR at 4.96%

- SOFR at 4.80%

- Term SOFR at 4.89%

- Headline CPI

- m/m came in at 0.1% vs 0.2% expected

- y/y came in at 5.0% vs 5.1% expected

- Core CPI

- m/m 0.4% as expected

- y/y 5.6% as expected

- PPI

- m/m came in at -0.5% vs 0% expected

- y/y came in at 2.7% vs 3.0% expected

- Retail Sales MoM came in at -1.0% vs -0.5% expected

- Rents dropped for the first time since March 2020

Inflation

CPI has shown tremendous improvement in just 9 months, falling from 9.1% to 5.0%, the lowest reading in two years. Unfortunately, a lot of that has to do with oil.

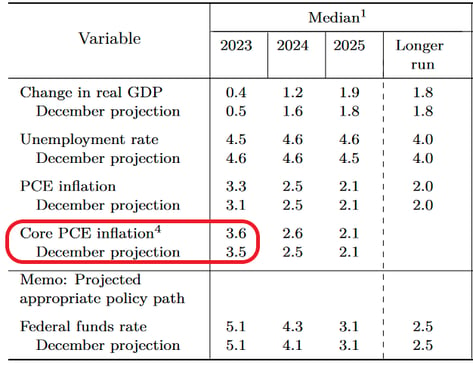

Core readings are proving far stickier. The Fed’s new preferred measure, aka “supercore”, has only improved from 6.4% to 5.8% over the same time period.

Core PCE peaked at 5.4% twelve months ago. It is down to 4.6% - an improvement of just 0.8%. Yay.

But the Fed is projecting that Core PCE will fall a full 1.0% in the next 9 months? FedGPT has some learning to do.

If the Fed hikes on May 3rd, it will be for two reasons:

- The market is expecting a hike and isn’t puking, so they might as well take advantage of it

- Inflation expectations are creeping higher

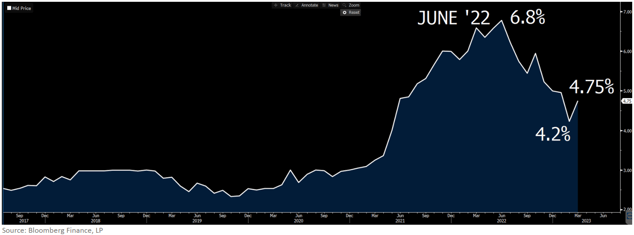

Consumer inflation expectations climbed again, likely a result of people like me conceding inflation is far stickier than originally expected. Here’s one year forward inflation expectations.

I think the Fed may hike just to combat inflation expectations from surging, hoping that in a few months the economy will have slowed so much that consumer expectations will take care of itself.

Speaking of a slowing economy…

Hello Stagflation

Recession odds continue climbing. Wells is calling for -0.5% GDP this year, while Bloomberg is down to 0.2%.

The Leading Indicator Index is updated this week, but is already at some pretty pessimistic levels.

The Cass Freight Index is showing a sharp downturn in shipping volumes. “Soft real retail sales trends and ongoing destocking remain the primary headwinds to freight volumes, and sharp import declines suggest this type of environment will persist for some time. Normal seasonality from the March level suggests 1%-3% y/y declines for the next few months.”

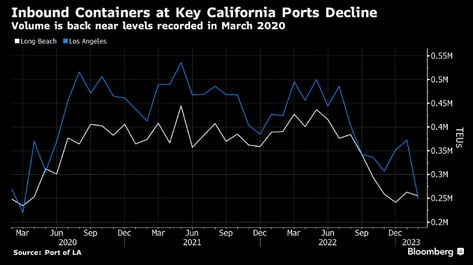

Check out the shipping volume in southern CA ports. And if you think China re-opening will take care of this, just know outbound containers from China dropped 5%.

US diesel demand is expected to contract 2%, which, outside of the first months of the shutdown, would be the biggest drop since Bloomberg started tracking it in 2016. We are “assuming one of the worst economic climates in recent memory outside of the 2008-2009 financial crisis and the pandemic” said S&P’s Head of Fuels and Refining, Debnil Chowdhury.

According to FreightWaves, “For the first time since the economy was shuttered in the early phases of the COVID-19 pandemic, the national Outbound Tender Reject Index (OTRI) has fallen below 3%, making early 2023 the softest sustained truckload market since the tender data history began in early 2018.”

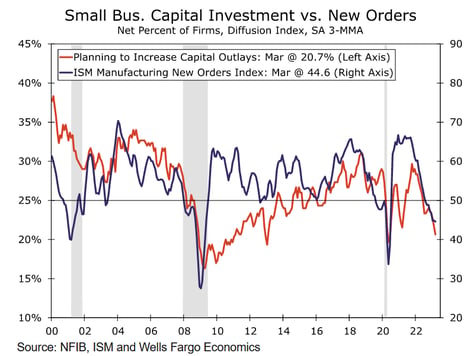

Small businesses have already downshifted investment dramatically.

Look how tight lending had become before SVB. The next survey is due out May 8th, and I have to believe it will look even tighter than today.

If there are few people in our industry that have dealt with true inflation, there are even fewer that have dealt with stagflation. If Powell’s job has been hard over the last year, it’s going to be even more challenging as the economy slows down and inflation remains persistent.

Rates

Futures put a 78% probability of a hike on May 3rd (5.25%)

- Then a pause in June

- Then a coin toss between a pause and a cut in July

- Then a 70% probability of a cut in September

- And an 80% probability of Fed Funds at or below 4.50% by year end

Oh, and a debt ceiling showdown somewhere in there. And Jackson Hole is in August, which the Fed frequently uses as a platform to announce major shifts.

Don’t forget – if the labor market weakens substantially in the coming months, it shouldn’t be interpreted as a faster path to rate cuts. The Fed is already expecting 1.5mm job losses this year.

The 10 Year Treasury may not plunge when the Fed starts cutting. Ahead of an expected tightening cycle, the 10T climbs and then waits for FF to catch up. The same is true in reverse - the 10T is already pricing in cuts and is waiting for FF to catch up.

In other words, if you are considering a fixed rate you shouldn’t assume it will get better if the Fed starts signaling cuts. And that’s before you consider that lending appetite is likely to tighten up even more in the coming months.

I think the Fed will hold on longer than usual before cutting. But that means the cuts on the other side will just be more aggressive. In an excellent piece this week, Wells is calling for FF to hit 2.50% in Q3 2024.

Whether the Fed hikes on May 3rd or is already done, they are on the clock for a cut.

And the backside is likely to be an aggressive cutting cycle.

Bank Stress

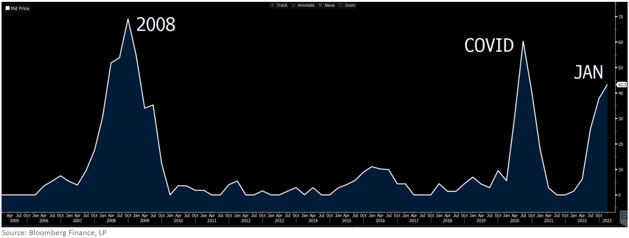

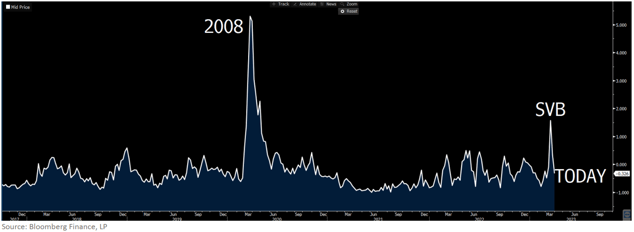

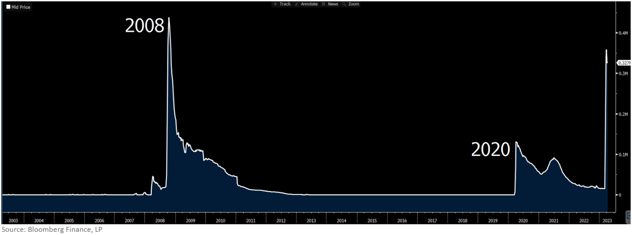

In March, the financial stress index surged to the second highest level ever before quickly retracing to more normal levels.

If the financial stress index above is a fair representation of the market, and the Fed is correct that banks are stable, then why hasn’t the emergency loan window been closed yet?

I agreed with the Fed’s emergency interventions to prevent full-blown contagion, but now it should quickly get out of the way and let free markets start doing their job.

Temporary measures should not become permanent, nor should the Fed be responsible for preventing all losses.

Bank earnings kicked off last week, with the biggest banks not surprisingly showing very strong numbers following a classic flight to too big to fail. It will be far more important to see how the more regional players did and what that fallout could look like. WSJ has a great scorecard of all bank earnings.

Week Ahead

Mostly Fed speeches as the headliners this week. Expect a lot of mixed signals because I’m not sure they have any idea what to do now. Throw in more bank earnings and volatility should remain elevated.