We survived.

Seven days, 2,500 miles, 100 degree temps, and 5 grown people in less square footage than a Manhattan efficiency. We drove an average of 8 hours a day and the three boys slept an average of 15 hours a day. We developed quite the gas station palate – gas station charcutier, gas station sandwiches, gas station drinks, etc. Little known fact – RV beds closely mimic laying on a bed of mulch, so at least we could always look forward to a good night’s sleep…

Some highlights:

Favorite event – Fort Worth Stockyards Rodeo

Favorite scenery – Monument Valley

Favorite dinner – Vegas steakhouse

Most impactful stop – Montgomery Civil Rights Museum

Most underwhelming stop – Four Corners

Last second decision highlight – Mardi Gras World, where they made the floats

Hottest temps – New Orleans/Texas/Arizona/Nevada/New Mexico (basically 90% of the trip)

Cheapest gas – Georgia

Most expensive gas – CA (by a mile, nearly every other stop was between $3.19-$3.49)

Worst roads – Alabama

Hardest roads – tossup between Atlanta and the mountains in Arizona/Nevada

Biggest Surprise – two dudes blasting Mary J Blige at 6am at the base of the Edmund Pettus Bridge (Selma)

Best RV Park – split vote, I say Santa Fe but wife says New Orleans

Worst RV Park – Arlington

Favorite quote – our 14yr old son, after struggling to get into the restroom of a restaurant, came back to the table exasperated. Just before he sat down, he says aloud to himself, “Wait, maybe it’s a pull…” meaning, he had only tried pushing the door open…

Breaking point – Day 2. New Orleans. 100+ temps. “How are we going to make it 5 more days?”

Top 3 Rookie Moves

- Unplugging the electricity while coffee was still being made

- Not giving the generator/AC a break, thus leading to them breaking in 100 degree temps with two days left

- Driving off with the side door wide open. Our son later recounted, “I felt a breeze on my feet but I didn’t think anything of it.” Future leader of America right there.

Are we glad we did it? Yes. Would we do it again? NFW.

My first day back in the office, my legs and feet start cramping. I figured it’s like one of those ghost injuries when someone loses a limb and it still feels like its there. My body still felt like it was driving for 10 hours. The next morning I wake up feeling sick. I dutifully take a covid test and sure enough, positive. Never mind I was just boosted a few months ago.

My wife wants to get me a t-shirt: I drove 2,500 miles with 5 people in an RV in 100 degree temps and all I got was this stupid covid.

Last Week This Morning

- 10 Year Treasury up to 3.04%

- German bund up to 1.40%

- 2 Year Treasury at 3.40%

- LIBOR at 2.52%

- SOFR at 2.28%

- SOFR will be above 3.0% within a month

- Term SOFR at 2.46%

- The market now has SOFR peaking at 3.83% in March

- Markets digested hawkish commentary from Fed Chair Powell as the Jackson Hole Economic Symposium

- PCE (month-over-month) came in at -0.1% vs expected 0.0%

- Core PCE (month-over-month) came in at 0.1% vs expected 0.2%

- PCE (year-over-year) came in at 6.4% vs expected 6.4%

- Core PCE (year-over-year) came in at 4.6% vs expected 4.7%

- Revised GDP (Q2) -0.6% vs expected -0.5%

- UMich 5-year inflation expectations came in at 2.9% vs expected 3.0%

- Debt forgiveness is absolutely definitely not inflationary

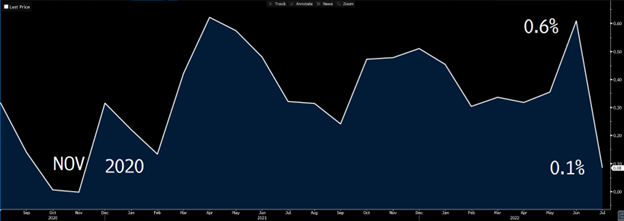

Inflation Still Showing Some Signs of Progress

M/M Core PCE showed the slowest pace since November 2020.

Source: Bloomberg Finance, LP

Source: Bloomberg Finance, LP

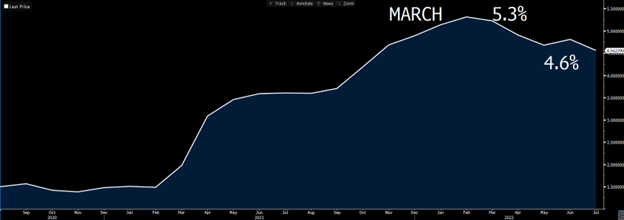

Annual Core PCE came in at its lowest level in almost a year.

Source: Bloomberg Finance, LP

Source: Bloomberg Finance, LP

September 21st Rate Hike – 50bps or 75bps?

Friday was a big morning. First, we got the Fed’s preferred measure of inflation, Core PCE. Then, Powell spoke at 10am.

At the last FOMC meeting, the debate was between 75bps and 100bps. The September 21st meeting debate is between 50bps and 75bps. Here are what the odds of a 75bps hike looked like Friday morning.

8:00am – premarket open, 68%

8:40am - after cooling PCE, 48%

10:30am - after Powell’s speech, back up to 60%

We get job data this Friday and another round of CPI data in two weeks before the September 21st FOMC meeting, so a lot can change before then.

I still think 75bps is the default right now. That would put SOFR around 3.25% within a month.

We will still have two meetings remaining before year end, so unless the Fed downshifts to 25bps hikes or pauses all together, SOFR will be at 4% by year end.

Jackson Hole – We Will Not Blink

So much for a soft landing…

Powell disappointed markets by telling us higher rates “will bring some pain.” Stocks plunged.

I think maybe we’ve forgotten that the Fed isn’t supposed to bail us out of the slightest hint of economic pain. Over the long term, corrections are healthy. Let the market do its thing. We need to get off this toxic cycle of the Fed intervening at the drop of hat. Then again, we’re forgiving debt in exchange for votes so maybe I’m the outlier here…

Powell continued, “Reducing inflation is likely to require a sustained period of below-trend growth.” Welp, so much for that soft landing.

He made it clear – the Fed is not stopping any time soon. It will not blink in the staring contest with inflation.

The risk of stopping too soon exceeds the pain endured to win. And if the Fed pulls back too soon, inflation expectations will start climbing again and become more firmly entrenched.

Here are inflation breakevens, both 5yr and 10yr. They peaked in March right before the Fed start hiking. In June, the Fed hikes 75bps and expectations plunge. The Fed is beginning to win the battle.

But look at what started happening this month. Expectations started climbing again. The market, prematurely, began pricing in a Fed slowdown. Powell sees this, and decided to send a message on Friday. I would expect these to trend back lower next month.

Source: Bloomberg Finance, LP

Source: Bloomberg Finance, LP

The market has cuts priced in beginning the middle of next year. If inflation continues to be slow to cool, the market may eventually change its tune and push the first cuts back into 2024. If this happens, it suggests higher floating rates and cap costs for more of 2023, and likely results in more dramatic rate cuts on the backside.

Week Ahead

Jobs report Friday. You may recall that last month’s report was a hugely positive surprise when we added 528k jobs. The consensus this month is a gain of 300k. Although inflation is the Fed’s sole focus, Powell has indicated that wage inflation within the broader inflation bucket is his primary concern. That puts the job reports squarely on the table.

And college football is back! Finally, something other than heat and rising cap costs I can hate.