Our friends across the pond are having an eventful few weeks. PM Boris Johnson’s Resignation. RIP Queen Elizabeth. Newly minted PM Truss created more chaos right out of the gate by outlining massive tax cuts with added spending. England’s own William Shakespeare wrote, “We have seen better days”. So true.

In 57 days, the British Gilt (their equivalent of the 10T) climbed by more than 2.70%.

August 1 1.80%

September 1 2.88%

September 27 4.50%

When Truss took over as PM, the Gilt was just below 3.0%. In the subsequent three weeks, it climbed by more than 1.50%. On Friday 9/23, she unveiled a large tax cut that would be paid for via higher spending. Et tu, Brute? Turns out adding more debt issuance in the face of climbing inflation doesn’t soothe markets. The Gilt spiked again to 4.50%.

That’s when the Bank of England intervened and committed to buying Gilts for “on whatever scale necessary” to restore price stability. The Gilt plunged back to 4.00%, a half point drop in one trading session.

I haven’t spent this much time thinking about England since Brexit, so I am calling in some help from the Bard of Avon himself, Billy J. Shakespeare, to help this week.

With the stage set (get it?), let’s jump into our first ever Shakespearian-themed newsletter, likely “told by an idiot, full of sound and fury signifying nothing.” (Macbeth)

Yep, it’s one of those newsletters.

Last Week This Morning

- 10 Year Treasury touched 4.0% in overnight trading and finished the week at 3.83%

- German bund up to 2.10%

- 2 Year Treasury at 4.27%

- LIBOR at 3.14%

- SOFR at 2.96%

- Term SOFR at 3.04%

- Monthly PCE came in at 0.3% versus 0.1% expected

- Monthly Core PCE came in at 0.6% versus 0.5% expected

- PCE (YoY) came in at 6.2% versus 6.4% expected

- Core PCE (YoY) came in at 4.9% versus 4.7% expected

- Consumer spending came in at 0.4% versus 0.2% expected

- Household debt is at an all-time high, surging $300B in the last year

- Is this how people have avoided going back to work? How much longer can they keep this up?

- With transaction volume drying up, "Neither a borrower nor a lender be" (Hamlet) feels like pretty good advice

Inflation

“Something wicked this way comes” – Macbeth

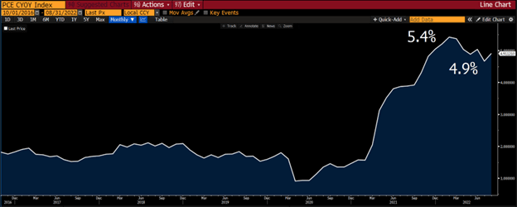

The Fed’s preferred measure of inflation, Core PCE, came out higher than forecasted on Friday. Last month’s reading was 4.6%, but this month climbed to 4.9%. This makes it incredibly challenging for the Fed to send any signals about a light at the end of the tunnel.

Source: Bloomberg Finance, LP

Source: Bloomberg Finance, LP

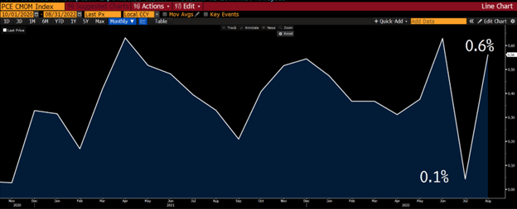

The monthly reading is worse news, accelerating from 0.1% to 0.6%. “Is this a dagger I see before me?” - Macbeth

Source: Bloomberg Finance, LP

Source: Bloomberg Finance, LP

While inflation readings are surging again, at least inflation expectations are plunging, right?

“Expectation is the root of all heartache.” Ugh.

Source: Bloomberg Finance, LP

Source: Bloomberg Finance, LP

If expectations are the root of all heartache, is Shakespeare warning us that inflation may not plunge like we expect it to?

Here’s my issue – why are we demanding the Fed keep hiking when we know there is a 1+ year lag? Powell hikes and inflation cools a year from now. Powell is aware of this, and his messaging is intended to manage inflation expectations. Powell has been winning this battle for the last six months and can’t talk about easing off the brakes yet, lest he give back this hard fought ground.

Still, Jay Money, you’re going to overdo it. Can’t you toss us a little bone? These CPI readings are backward looking!

"I am not bound to please thee with my answer." – The Merchant of Venice

Jay! You told us there’s a one year lag! Why are your decisions influenced by current inflationary readings?

"Though this be madness, there is method in it.” – Hamlet

There’s a surprise FOMC meeting today, not sure what that’s about. While I think the Fed should be leveling off so that it can transition into a “monitor” position, that’s not going to happen anytime soon.

Jay! Besides crushing demand with higher rates, what are you doing to curb inflation?

“On my knees in the night, sayin’ prayers in the streetlight” – Hamlet Coolio (RIP)

Floating Rates

“Don’t fight the Fed” – Romeo and Juliet

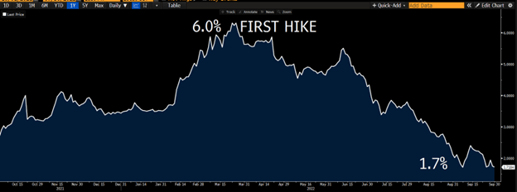

Two enormous shifts over the last two weeks for Fed Funds that you have to be aware of:

- Higher Peak

- High all of 2023

The forward curve looks totally different than a month ago. Then, it looked like a rollercoaster. Peak at 4.0%, immediately fall.

Now it peaks at 4.50% and remains elevated into 2024.

5% Fed Funds? “To be or not to be, that is the question” - Hamlet

10 Year Treasury

The 10T hit 4.0% early Wednesday morning before immediately plunging 0.30% to 2.70%. Why? England.

After rates spiked 0.50% on Monday, the Bank of England intervened to bail out Truss.

“What’s done cannot be undone” – MacBeth

“Hold my beer” - BofE

The Bank of England’s intervention caused global yields to plunge.

“Were dysfunction in this market to continue or worsen, there would be a material risk to UK financial stability. This would lead to an unwarranted tightening of financing conditions and a reduction of the flow of credit to the real economy,” the Bank of England said. “In line with its financial stability objective, the Bank of England stands ready to restore market functioning and reduce any risks from contagion to credit conditions for UK households and businesses.”

That means our own 10T is being heavily influenced by developments out of England. This could lead to very large swings overnight, rather than after our own data releases at 8:30am.

Near Term

The 10T can stay elevated while the data keeps coming in strongly. “Hey, maybe we’re gonna be ok? We’re still adding 300k jobs a month and unemployment is 3.7%.”

But that’s only because the impact of the tightening hasn’t had time to flow through. I think there’s a much greater likelihood of a 4% 10T at the end of this year than there is at the end of next year.

Longer Term

The more the Fed has to hike, the greater the pain will be next year. We’re only six months into the tightening cycle, probably about half-way. You think it feels bad now? Give it a year. “Jesters do oft prove prophets” – King Lear

Current range: 3.77% - 4.00%

Above 4%: next technical resistance is 4.26%

Below 3.77%: 3.50% and then 3.26%. Remember, 3.26% was the hugely important level as yields pushed higher, and the same will be true if we push back below it.

Source: Bloomberg Finance, LP

Source: Bloomberg Finance, LP

Week Ahead

Lots of data, including some manufacturing data that tends to be a better leading indicator than CPI.

Friday will be the fun one with unemployment numbers and NFP, which can give us insight into how the labor market is reacting to recent Fed decisions. Consensus forecast is a gain of 250k jobs, with the UR holding steady at 3.7%.

Hey JP, didn’t Hamlet say, “Brevity is the soul of wit”?

Crap.

Well, "better a witty fool than a foolish wit." – Twelfth Night

So, until next week, “parting is such sweet sorrow” – Romeo and Juliet