As expected, the Fed hiked 50bps but signaled we should expect 0.75% more early in 2023 (up from 0.50%). This would push Fed Funds to 5.00%-5.25%.

Powell used “as of today” so much it feels like he’s:

- downshifting to 25bps on Feb 1

- despite the change to 75bps, he’s leaving the door open for maybe doing less

- hedging the back half of 2023 in case the Fed has to cut rates

When asked if the Fed would hike 50bps on Feb 1 and 25bps in March, he said it is no longer about the pace of hikes. Going forward, it is more important to focus on when they can stop hiking and how long they stay at that level.

While claiming we will narrowly avoid a recession, the forecasted unemployment rate implies 1.5mm Americans will lose their job over the next year.

“We are getting close to sufficiently restrictive levels,” Powell said. “We will stay the course until the job is done.”

Rates

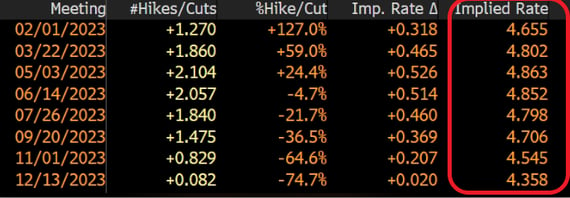

The Fed’s blue dots suggest Fed Funds will end 2023 at 5.1%, half a point higher than projected at the September meeting. Higher for longer has replaced transitory as the buzz phrase at the Fed.

The Fed expects to cut 1.00% in 2024, while the market thinks the cuts will come in the second half of next year. Even if Powell believed that, he can’t say that today. He has to keep inflation expectations in check.

On the likelihood of rate cuts, ”I wouldn’t see us considering rate cuts until the Committee is confident it sees inflation moving down towards 2%.” So as soon as the lagging shelter component starts showing up?

The Fed projections and remarks were hawkish, but the market interpreted it as slightly dovish. In fact, the market is pricing in 2-3 cuts late next year.

Source: Bloomberg Finance, LP

I think the Fed will be cutting at some point within the next 18 months, but suspect the Fed will keep rates elevated for longer than usual to really drive down inflation. Don’t be surprised if a lot of the Fed-speak in the coming weeks tries to change the market’s reaction.

Rates are mostly unchanged.

10T 3.50% (not a coincidence it sits atop a key level)

2T 4.24%

Cap Costs

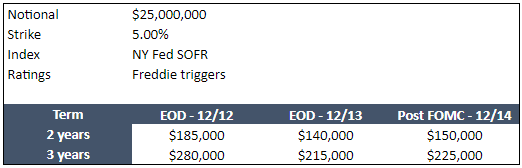

Cap prices fell following yesterday’s CPI print. Today’s hawkish-ish meeting pushed costs back up a little, but not back to last week’s levels. Sample $25mm 5% cap over the last three days.

Inflation

When asked whether the Fed would consider changing the 2% inflation target, Powell said, “Absolutely not.” Cool.

But then he said, “Not now…but it may be a longer run project at some point.”

What?!?! Powell just acknowledge the Fed may move the goal posts! I don’t think they will change it outright, but we might hear more talk next year about inflation averaging 2%.

Summary of Economic Projections (SEP) Today vs September

Everything was revised worse. Yay.

- Fed Funds up from 4.6% to 5.1%

- GDP revised down from 1.2% to 0.5%

- Unemployment up from 4.4% to 4.6%

- Core PCE up from 3.1% to 3.5%

Takeaways

- We are close to the end of the tightening cycle

- The Fed seems very committed to keeping rates higher for longer to beat inflation

- Cap costs are down over the last three days

- 2024 outcomes are incredibly uncertain