The 10th annual newsletter that answers the question no one asked – what if markets played in bowl games? We also visit how we did on last year’s predictions, because who doesn’t like to see in writing how wrong they were?! Just remember – 60% of the time, my predictions are right every time. Let’s do this.

Tax Slayer Bowl

Real Matchup – Texas A&M vs NC State

Markets Matchup – Current Inflation vs Future Inflation Expectations

A battle between schools with an intrastate inferiority complex. Texas A&M wishes it was Texas (but not Texas Tech), while NC State wishes it was UNC (but not UNC-Charlotte).

The Aggies have to be happy with Jimbo Fisher’s first season. While finishing 8-4, two of those losses came to Alabama and Clemson. Who plays the best two teams in the regular season!? Of course, the highlight was the 7 overtime win against LSU. That game went on so long that it was still playing when I woke up. NC State’s athletic department hasn’t been relevant since Jimmy V, usually referenced only in its relationship to UNC and Duke. Their record is horribly inflated from playing in the ACC, a conference where the best football players at the school play basketball instead.

On paper, Texas A&M should destroy NC State. But on the field, Texas A&M should really destroy NC State. The Wolfpack’s only hope is the Aggies’ remarkable commitment to disappointing fans. With Notre Dame in the playoffs this year, the Aggies take the mantle of “Team That Gives You Some Hope Before Smashing Them Into a Million Pieces”. That may make this game closer than expected, but Texas A&M is a legitimate college football team while State is glorified high school squad.

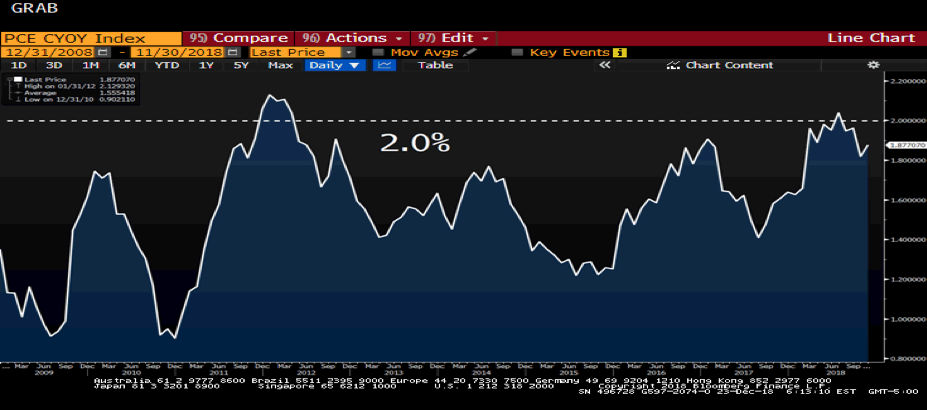

Core PCE, the Fed’s preferred measure of inflation, steadily climbed most of the first half of the year. It peaked in the July 31st report, briefly touching 2.0%. It has since retreated slightly, bouncing between 1.8% and 1.9%. Here’s a ten year graph of this inflation measure. While 2.0% is still the Fed’s target, it’s not hard to conclude that NC State has a better shot of winning than inflation has of breaching 2.0%.

But the Fed also has to consider future expectations, particularly as it relates to inflation. Inflation is one of those quirky data with a quasi-self-fulfilling prophecy aspect to it. If you think something will cost more in the future, you buy it today. That increases demand, driving up prices. Voilà – inflation!

But the opposite is true as well. If you think something will cost less in the future, you hold off on the purchase. Lack of demand pushes down prices. This explains why the Fed wants 2.0% inflation…just enough to prompt you to buy today and keep the economic engine churning. If you stop buying stuff today because you believe it will cost less in the future, then prices fall, the economy slows, which in turn further drives down expectations and we enter a vicious downward cycle.

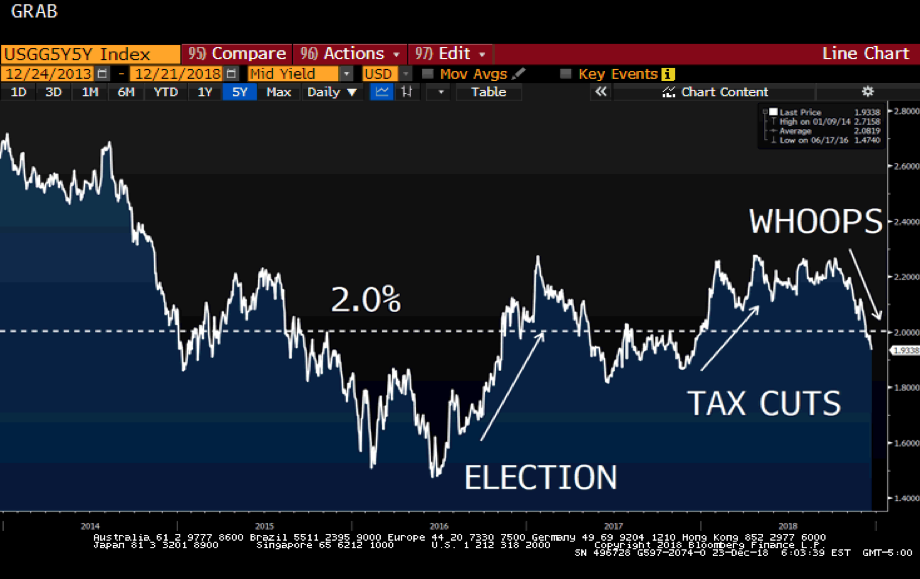

Here’s a five year graph illustrating future inflation expectations (as opposed to Core PCE, which measures how much inflation we’ve seen over the last year or quarter).

Following Trump’s election, inflation expectations climbed more than actual inflation. The same thing happened after that tax cuts a year ago. We might see a similar response if some sort of infrastructure bill gets passed. But in the meantime, expectations are falling…and the Fed should be taking notice. This is bad juju because if it continues its slide, consumers start holding off on purchases, further exacerbating the problem.

Prediction – Core PCE struggles to break through 2.0%, but hovers around this level for most of 2019.

Inflation expectations, however, will have a more volatile year.

– if pessimism continues and the Fed keeps sending messages about hikes, expectations will fall

– if we can put the trade war with China behind us, the Fed pauses, or an infrastructure bill passes, these expectations could climb above 2.0%

Belk Bowl

Real Matchup – South Carolina vs Virginia

Markets Matchup – jk, no one cares about these teams

Citrus Bowl

Real Matchup – Penn State vs Kentucky

Markets Matchup – Reverse QE vs German Bund

I know few things as well as I know PSU football, which is probably a sad state of affairs. Last year’s team was a legitimate contender for national champion. Two losses by a combined 4 points in back to back road games. If we hadn’t choked to Ohio State, I think we make the playoffs…Bama probably beats us, but I’m telling you we would have had a shot. We were that good.

This year’s team was overrated right out of the gate, and not just because Saquon left (the best PSU football player I’ve ever seen). Most importantly, the offensive coordinator left to be head coach at Miss St. That left us totally disjointed. Our scoring dropped by 7 points a game, but it was worse than that. Totally ineffective at times against even bad defenses. Secondly, the defense lost 8 starters. We were lucky to go 9-3.

Kentucky is a basketball school and I won’t commit the energy to their football team here. And no, it’s not because they just beat UNC again this weekend and I’m still mad. But they should stick to what they know. You don’t see me going off on political or sports tangents, do you?

PSU wins. McSorley refuses to lose his last game. Never plays a down in the NFL. Similarly, Kentucky fades back into irrelevance.

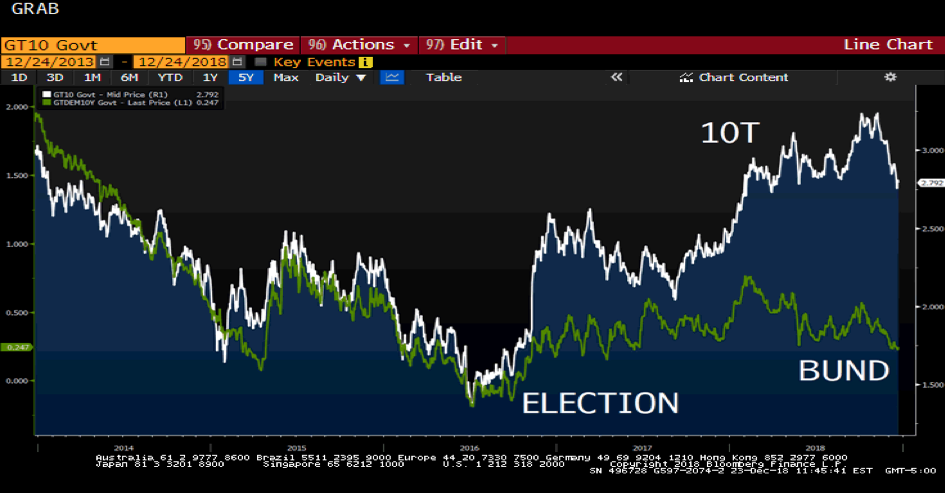

Like PSU, Reverse QE (aka Balance Sheet Normalization) came into the year over-hyped. In the same newsletter last year, we wrote, “balance sheet normalization will have a relatively minor impact on rates in 2018 as the Fed dips its toes into the balance sheet normalization water and the ECB slows the pace of purchases.”

While it is difficult to measure the impact on the 10 Year Treasury, it certainly had an impact on tightening financial conditions. The Fed is now on cruise control, reducing the balance sheet by $50B per month as originally envisioned a year ago.

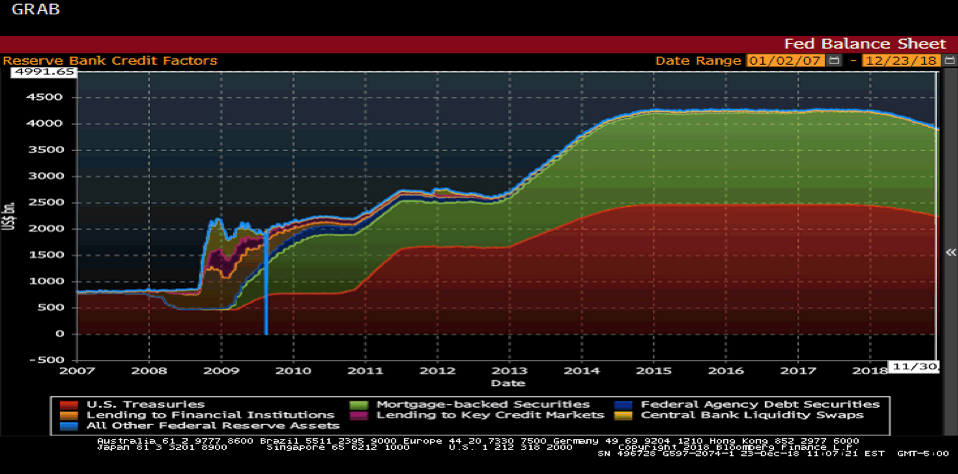

As you can see from the graph below, this is going to be a very lengthy process. The Fed is allowing maturing holdings to roll off rather than reinvesting the proceeds. It can’t actively sell Treasury holdings without spooking markets and causing massive Treasury selling, so it is gradually and passively allowing the balance sheet to shrink.

If the pace continues, a year from now the balance sheet will have reduced from $3.9T to $3.3T. At this pace, the Fed’s balance sheet will be back to pre-crisis levels in 2025. The Fed knows this is an unlikely scenario, but instead is simply trying to make room to enact another round of QE. It’s basically the same thing as hiking to get away from 0% – create some room for accommodative measures when needed.

Because the Fed spent more than a year signaling this process, and because it is so gradual, and because it is on autopilot, the market had it pretty effectively priced in. That’s why the impact has been muted.

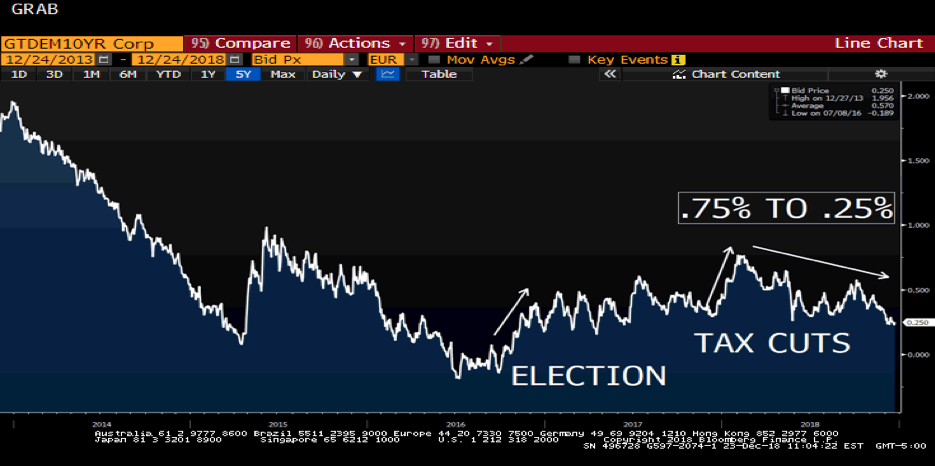

Like Kentucky football, no one had heard of the German bund a few years ago. Now most observers realize it is one of the biggest influencers on the 10T. As the bund yield moves up, the 10T has room to move up as well. And when the bund moves down, it tends to drag the 10T with it or at least serve as a leash on the 10T from moving higher. It peaked mid-summer at 0.75%, and has since fallen to 0.25%.

The ECB is a few years behind our Fed, so QE tapering was on the table for some point. That announcement came over the summer and QE officially ends (for now) on December 31st.

Notice how highly correlated the bund and 10T were until the election. Then the relationship broke down dramatically, with optimism that the US could decouple from the lagging eurozone.

Prediction – Reverse QE will continue to have some impact on Treasury yields, but not a dramatic one. It will, however, have an outsized impact on financial conditions. There will be a lot of market chatter about the Fed pausing its balance sheet normalization process, but they won’t actually do it in 2019.

The ECB will start discussing rate hikes at some point in the first half of the year, which could drive up the bund. For the second year in a row, we are 100% confident the bund will finish the year above 0.60%. On a long enough time line, my predictions come true!

Rose Bowl

Real Matchup – Ohio State vs Washington

Markets Matchup – Republicans vs Democrats

The granddaddy of them all, the Rose Bowl! I couldn’t name one player on Washington, but I will be pulling for them hard. I never understood people that root for their archrivals out of conference loyalty. Not me. I can’t spend 364 days a year rooting for a team to go winless and then flip a switch. I want Ohio State to lose. Badly. There is no score where I would say, “Gee, I wish that had been closer.” Remember when Clemson beat OSU 31-0 in the playoffs? Waaaaaay too close for my liking. That sounds like a good first quarter.

But I got an early Christmas holiday present. Urban Meyer resigned. And this is no joke, he will be teaching a class in the spring called, “Integrity and Leadership.” That’s about as appropriate as a politician teaching a class on bipartisanship.

Like Meyer, many GOP incumbents are throwing in the towel. Fighting Trump populism is exhausting. There’s a long list of distinguished political servants that are stepping away. That isn’t a coincidence. I chastised the GOP in last year’s newsletter, “I don’t think Republicans are adequately pricing in the long-term damage to the GOP of a Trump presidency.” Everyone was willing to look the other way on all sorts of chaotic/racist/misogynistic/populist policies when the markets were doing well, but those chickens might be coming home to roost now. National security is now defined as building a concrete wall between us and a neighboring ally, but what do a couple generals know about national security? I hope it was worth it GOP.

Democrats are a dumpster fire. They can’t even agree on the Speaker of the House. Bernie Sanders and Joe Biden are leading early 2020 polls. They will be 79 and 78 years old, respectively, in two years. The party that has traditionally hung its hat on youthful charisma like JFK, Clinton, and Obama are now looking to octogenarians for inspiration. Good plan.

Prediction – Trump will be impeached by the House. I don’t think Pelosi really wants to do this, but the Mueller investigation has brought so many convictions that it seems highly unlikely Trump isn’t involved on some level. The division in power means little legislative progress, but the economy keeps chugging along.

Trump has enough die hard supporters in the Senate to avoid being removed from office. And spare me the comparisons with Bill Clinton. I don’t care any more about Stormy Daniels than I did about Monica Lewinski. Those behaviors might influence my vote, but are not impeachable offenses. Coordinating with an enemy for personal gain, however, is. If it is proven that Trump put his own personal gain before the country (shocking, I know), Mitch McConnell is going to have his hands full. There’s a reason we haven’t seen tax returns.

Sugar Bowl

Real Matchup – Texas vs Georgia

Markets Matchup – Tightening Financial Conditions vs Recession

Texas looks to be fully on the road to relevance again, beating USC and TCU and playing competitively against Oklahoma and the thriller against West Virginia. But they also lost to Maryland. In football. UGA lost at LSU and then gave away a W against Bama in the last game of the season by following the James Franklin Chokebook, available now on Amazon Prime. Highlights include prevent defense with 10+ minutes remaining, questionable clock management, and the crowd favorite bubble screen telegraphed so beautifully even 11 year olds at home can see it. “I loved the sweep right on page 39 – 4th and 6, go with the handoff when you’ve rushed for 5 yards all game. Gutsy. Genius.” – Urban M., Ohio. 3.5 out of 4 stars.

Texas is playing for a lot, while UGA is sulking after missing out on the playoffs. UGA is the better team on paper. By a lot. I think this could be closer than expected, but UGA could make an argument for being the second best team in football right now. Talent wins out, and I’m pretty sure I could still walk on to the Longhorns if I promised to fetch water and lead the crowd in chants of “Lock Her Up!”

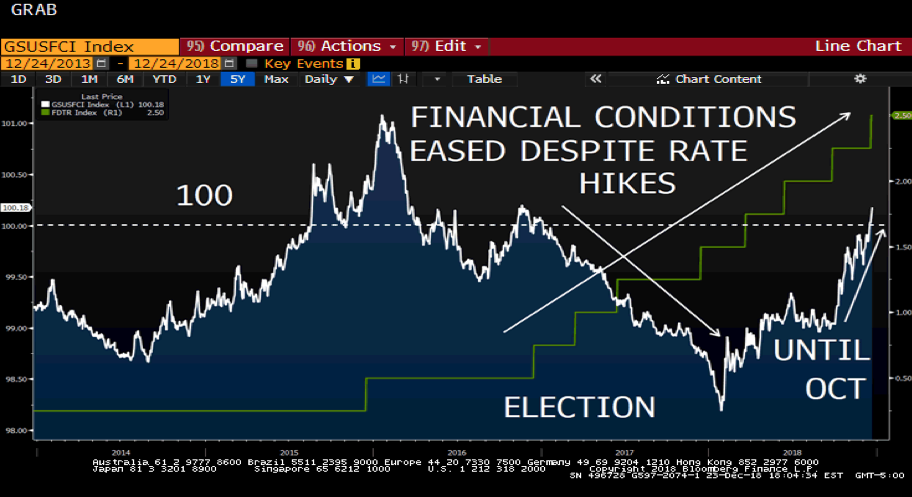

Like Texas, Financial Conditions is gaining prominence. In the graph below, a score of 100 means financial conditions are neutral – neither accommodative nor restrictive. When conditions are above 100, conditions are restrictive to growth. When the measure is below 100, conditions are accommodative and encourage growth.

For much of this Fed tightening cycle, financial conditions were actually easing. That shouldn’t happen. Raising rates should tighten financial conditions. That’s probably why Powell was comfortable hiking – it wasn’t working like it should. Do more!

So what influences financial conditions? Fed monetary policy is at the top of that list, but it isn’t just rate hikes. Quantitative Easing (QE) seems to materially ease conditions. But so do strong stock and credit markets. Fed forward guidance. Stuff like that.

So while the Fed was hiking, conditions weren’t tightening because many of the other factors were conspiring to keep conditions accommodative. But that all started to change recently. Have you read any negative headlines about stocks lately? Or credit spreads widening out?

If you’re still reading this War and Peace treatise on markets and bowl games, write this down somewhere – Financial Conditions is going to be a YUUUUUUGE deal in 2019. I can’t stress this enough.

If Powell doesn’t respond to this shocking tightening we’ve experienced in the last three months, the odds of a recession will jump dramatically. Trump could help by negotiating a deal with China or coming up with an infrastructure bill, but I’m not holding my breath.

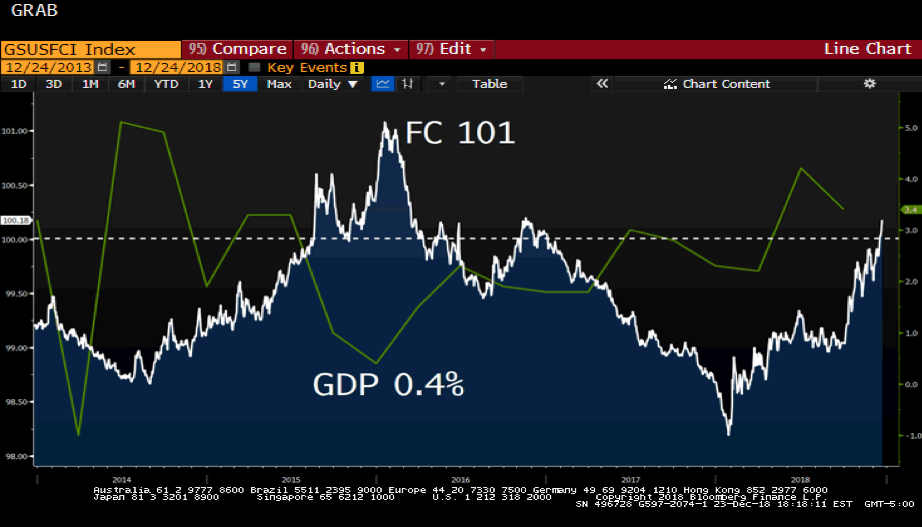

Check out the inverse relationship between Financial Conditions and GDP over the last five years. When conditions are tight (above 100), GDP drops. Conversely, when conditions are loose (below 100), GDP climbs. This is not a coincidence. And the sharp increase in Q4 spells trouble for early 2019.

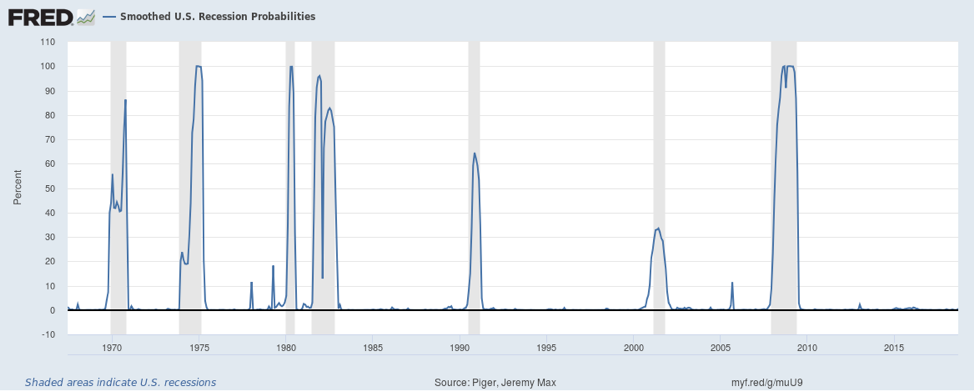

Lee Corso – “Not so fast!” The Fed has a recession probability model, and it puts the odds of a recession in the next year at less than 1%. Historically this model has done a pretty solid job of forecasting a recession once odds break through 20%, but it doesn’t give much warning. Therefore, a 1% reading today could increase dramatically in the coming months, but until then the Fed isn’t seeing many warning signs.

Prediction – Powell reacts to the sharp tightening of financial conditions and slows the pace of hikes while also sending the appropriate amount of dovish signals. Financial Conditions level off and hover around neutral for most of 2019.

Powell has consistently been hawkish on the US economy, while highlighting the risks from exogenous shocks, like a trade war or geopolitical event. In other words, if left alone the US economy is unlikely to experience a recession in the near future. The US does not enter a recession in 2019, but we see more and more flashing yellow lights.

Orange Bowl

Real Matchup – Alabama vs Oklahoma

Markets Matchup – Swaps vs Caps

I haven’t figured out why Nick Saban doesn’t demand $20mm a year. Or $30mm. What leverage does the Bama administration have exactly? The football program generated 62% of all Alabama sports revenue and $46mm in profit. Since the total athletic department reported $15mm in profit, that means football single handedly offset $30mm in losses by the rest of the sports. How do those numbers look the year after Saban retires?

Meanwhile, Oklahoma has back to back Heisman winners and is somehow in the college football playoffs yet again. Maybe it’s because the Big 12 is the only conference that can match the Big 10 for overhyped big, traditional programs? They gave up 40 points to Kansas. In football. And this isn’t your dad’s Alabama team, these guys were consistently dropping 50 on SEC teams. And Tua deserved the Heisman, so I suspect he will be playing with a chip on his shoulder. Alabama is going to win this one convincingly.

Like the Tide, caps have been the market powerhouse since the financial crisis. But 2018 was a different year.

Check out how much volatility a 3 year cap at 3.00% has experienced over the last year. This assumes a $50mm structure. At the Money (ATM) is simply the 3 year swap rate.

Date Cost ATM

December 2017 $100k 2.05%

October 2018 $425k 3.00%

December 2018 $200k 2.60%

So, if you had bought a 3 year cap last December instead of locking in a 5 year swap at 2.30%, do you regret the decision?

Well, you paid $100k for the cap and it hasn’t provided any protection.

But, you saved about $150k in interest expense by floating, so the cap still looks good.

But how about going forward? LIBOR is now 2.50%, costing you about 0.20% per month, or $8,333, while LIBOR stays at current levels. That means if the Fed doesn’t hike again, you’ll hit the breakeven point in 6 months.

The swap is currently worth about $500k to you, while the cap is worth about $80k.

Since the market was underestimating Fed hikes by 0.50%, and the Fed ended up keeping its word, the swap looks better. This also assumes rates don’t fall.

Caps tend to look better when the market is right about the number of hikes (basically every year before this year). Swaps look better when the Fed is right about the number of hikes.

The Fed is projecting two hikes in 2019, while the market is predicting almost no hikes. That means there’s a 0.50% discrepancy again, just like last year. If the Fed ends up being right again, we could see a similar trend over the next 12 months.

Prediction – a year from now, a swap may outperform a cap in a similar fashion but to a smaller magnitude. Current market pricing is exceptionally pessimistic. If bad news fails to materialize, markets may have to correct over the course of the first half of 2019 and catch up to the Fed. Locking a swap now could end up looking attractive.

But…but…but…if the Fed has to cut rates at some point in the next five years the cap could end up looking significantly better.

Cotton Bowl

Real Matchup – Clemson vs Notre Dame

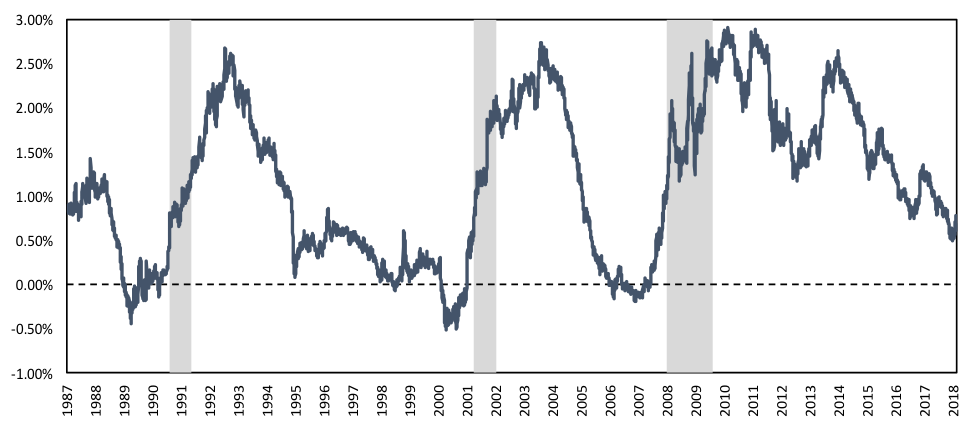

Markets Matchup – 2 Year Treasury vs Inverted Yield Curve

Clemson is the only team that can compete talent-wise with Alabama every year. The Irish are usually the only team that can compete with Ohio State for the coveted “Most Overrated and Overhyped Program Still Riding on the Coattails of History and a Fat Television Package from NBC” title.

I love Dabo Sweeney. He’s my favorite coach in college football. And he puts some serious NFL talent onto the field each week. Brian Kelly has typically underwhelmed me. That being said, there is something different about this Irish team. I didn’t buy into them after they opened with a W against Michigan because, well, Michigan. But they have been dominant from the beginning and belong in the playoffs.

Clemson is 2 TD favorites…TWO TOUCHDOWNS! That is bonkers. Notre Dame is undefeated. This isn’t a totally undeserving Ohio State team from two years ago (can you tell how I feel about OSU?). And who has Clemson beat this year? NC State? Syracuse?

No doubt that Clemson is the more talented team. And they have the better coach. But I can’t shake this feeling that Irish are going to pull an epic upset.

The Irish are like the inverted yield curve, frequently dismissed but ready to make a statement in 2019. We did a really in-depth analysis on an inverted yield, so I won’t rehash it all here. Some key takeaways:

– the last seven yield curve inversions preceded a recession

– from the first inversion, a recession typically took 1-2 years to materialize

– the yield curve flip flops positive and negative

Powell has been shockingly dismissive of an inverted yield curve. It is my single biggest complaint about his tenure thus far. It takes a lot of nerve to say, “This time will be different.” Here’s the NY Fed probability of a recession in the next 12 months based on Treasury yields. Bond yields are starting to signal a warning.

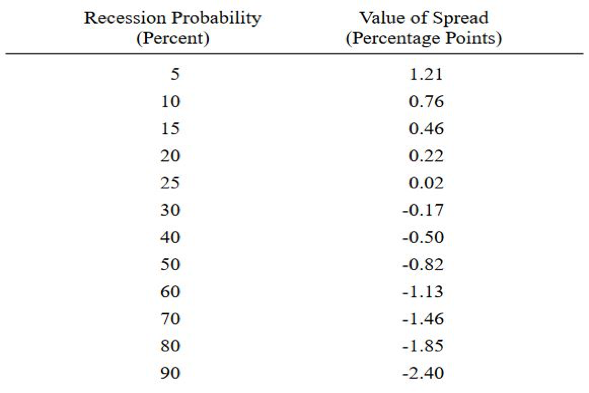

The NY Fed also released a report in 1996 that attributed a probability of a recession within the next year to the severity of the inversion. At current steepness levels (<0.10%), there’s a 25%-30% probability of a recession in 2019. That’s about the same odds Notre Dame has of beating Clemson. Coincidence?

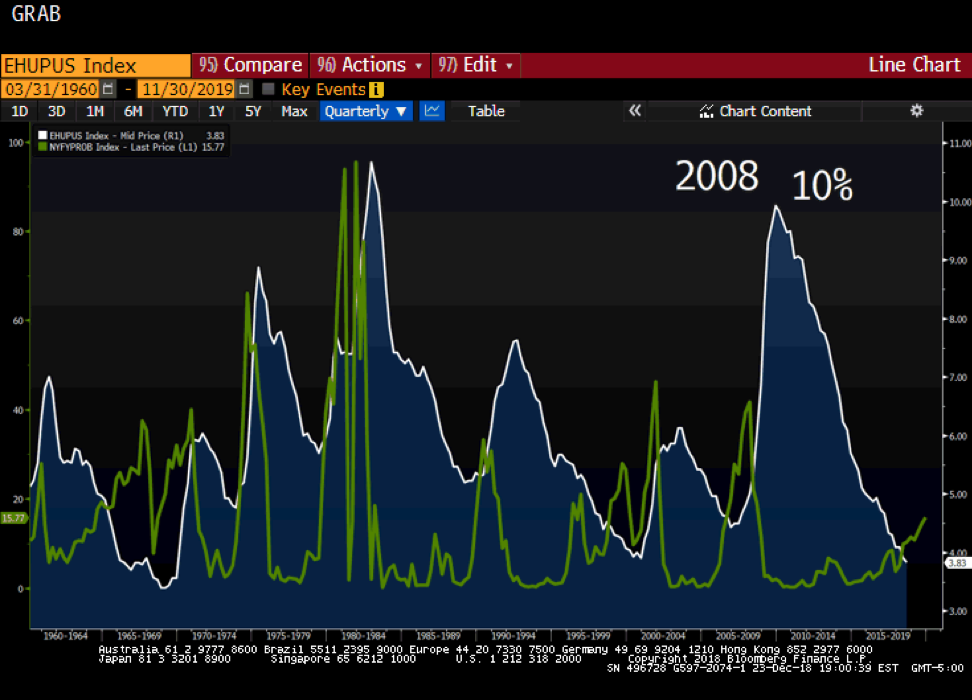

This graph below is not visually appealing, but humor me. The green line is the NY Fed probability of a recession odds from above. The white/blue line is unemployment rate. Intuitively, it just feels hard to have a recession with sub-4.0% unemployment, right?

But note how when the green line jumps, the unemployment rate tends to spike shortly thereafter.

Like many other signals, this is more of a warning shot across the bow then a full blown “Alert!” signal. But this is something we will be watching very closely.

And if unemployment starts climbing, buckle up.

The 2 Year Treasury had an eventful year. This yield is considered the benchmark for Fed policy expectations. It’s yield 2.64%, which roughly means the market thinks LIBOR will average 2.64% over the next two years.

With LIBOR at 2.50% right now, it doesn’t take a Stanford MBA to conclude the market is pricing in nearly zero hikes over the next two years. The market was wrong this time a year ago.

Prediction – The yield curve will invert in Q1 2019. Powell will be slow too slow to send reassuring signals to the market. Talking heads and Powell spend a lot of time explaining why this time will be different. This time will not be different. Cue recession in 2020 or 2021.

The 2 Year Treasury will finish 2019 below 2.75% and Clemson loses unexpectedly. Like Clemson, the 2 Year Treasury’s time in the news is largely done for now.

National Championship

Real Matchup Prediction– Alabama vs Notre Dame

Markets Matchup – LIBOR vs 10 Year Treasury

Maybe the most storied programs in college football history meet for the title, so it’s only fitting that the grand finale match-up pits LIBOR vs the 10 Year Treasury.

LIBOR started the year at 1.56% and will finish just above 2.50%. The Fed did exactly what it said it would do – hike 4 times (1.00%). The market (and we) we caught offsides. Two hikes seemed more reasonable, which would instead have put LIBOR around 2.00%.

The last time the Fed was increasing rates to 2.50% was January 2005 – 14 years ago. Think about that for a minute. You have some pretty senior colleagues that have never experienced a rate hike taking Fed Funds to 2.50%. People with a decade of experience have never dealt with floating rates at this level.

The 10 Year Treasury is a conundrum. A pretty healthy economy, fiscal stimulus, 50 year low unemployment, Reverse QE, record breaking Treasury issuance, etc.

And for most of the year, that mattered. The T10 started the year at 2.40% and almost immediately broke the key technical level of 2.82% that had held for 4 years. It spent the rest of the year above that, getting up to 3.25% in October before collapsing heading into year end. Trade war fears and an aggressive Fed will do that.

Prediction – Notre Dame is like LIBOR – it has outperformed expectations but the ride stops here.

The Fed is done or nearly done hiking. If it gets a hike in, it will be in June. Powell needs to reassure markets before he moves again. He finally threw in the towel after the markets spent two months puking over his comment about rates being a long way from neutral. Now he believes rates are about neutral. LIBOR finishes 2019 at 2.75%-ish.

The 10 Year Treasury was 3.25% six weeks ago, now the world is suddenly ending? I don’t buy it. Just like I don’t buy that Alabama is a college football team. More importantly, Powell has learned a valuable lesson over the last few months. I am betting that Powell will ease up on the rate hike talk, which in turn will allow some risk taking psychology.

The curve will invert in Q1, but Fed-speak will eventually allow the T10 to climb. The 10 Year Treasury yield finishes 2019 between 3.15% – 3.35%. Alabama wins another title. Gross.

Last Year’s Predictions – 12.26.17

Yellen vs Powell

Prediction – “He will continue the gradual pace of tightening while rolling back the more onerous DF regulations that have stifled traditional lending activity. One potential concern is Powell’s lack of a PhD in economics, which may mean he leans on the other Fed members more than his predecessors. If Trump appoints deeply hawkish members, rate hikes could come faster than the market is prepared for.”

What Actually Happened – Reasonable start to the recap, but we thought “gradual” would be more like 2 hikes instead of 4 hikes.

Inflation vs Swap Spreads

Prediction – “like the Missouri football program, swap spreads are unlikely to generate many headlines in 2018. We expect spreads to remain close to 0% and won’t climb significantly positive unless there’s a shock to the markets.

Inflation won’t blow through 2.0%, but it will climb higher and apply pressure to the Fed. Inflation is a greater threat than last year and there is upside risk of exceeding 2.0% that has been missing for five years. Global (cough cough Eurozone) economies are seeing signs of inflation, which may increase expectations.”

What Actually Happened – inflation hit 2.0% but didn’t blow through it and when was the last time you read a story on swap spreads? 10yr swap spreads finished the year at positive 0.04%.

Inverted Yield Curve vs German Bund

Prediction – “unlike most economists, we believe the threat to an inverted yield curve is in the second half of 2018, not the first half. This is based on the theory that the Fed will only hike if the 10T has already climbed.

We think the Fed, under Powell’s leadership, will be very slow to hike for this very reason. A sudden jump in the 10T doesn’t mean it will remain at those levels.

The yield curve will not invert in 2018 and the Bund will finish above 0.60%.”

What Actually Happened – pretty good on the yield curve, particularly even calling for the threat of an inversion in the second half of the year.

Not so good on the bund, which is around 0.25% as of this writing. But you can’t get them all right, right?

Republicans vs Democrats

Prediction – “The Democrats will win the House in November while the Republicans retain control of the Senate. Talk of impeachment will heat up after the mid-terms; however, as long as Trump is at the helm, businesses will generally feel like the government will not be out to get them. A Republican-controlled Senate gives business assurance that legislative gridlock will not interfere with the economy. Markets generally cool off, but don’t stall entirely. Democrats fail to appreciate the irony as they focus on a sweep in 2020.”

What Actually Happened – someone get me an agent, I need a spot on CNBC or something…

Bonus Prediction – “Mueller completes his investigation before the mid-terms. President Trump is implicated, but not directly so. Republicans dig in their heels to hold the line at all costs, galvanizing the left. No impeachment until after the mid-terms.”

What Actually Happened – Mueller still not done, so a whiff there…

Future Prediction for 2019 – The Democratic-controlled House will pass Articles of Impeachment and the Republican-controlled Senate will not convict. All legislative progress grinds to a halt and we relive 2014-2016.

What Actually Happened – I feel pretty good about this one…

Inflation vs Global Removal of Accommodation

Prediction – balance sheet normalization will have a relatively minor impact on rates in 2018 as the Fed dips its toes into the balance sheet normalization water and the ECB slows the pace of purchases…but this is a theme that could dominate markets for the next several years. More people will have heard of “balance sheet normalization” this time next year than today. Central banks are trying to unwind the emergency policies from the 2008 crisis. There is risk this doesn’t go smoothly, but we believe that is a bigger threat in 2019 and beyond.

We think the 2 Year Treasury climb will cool off. This is a bold prediction, even if it doesn’t feel like one. We are basically suggesting the Fed will slow its pace of hikes, which in turn will dampen 2T rate movements. The 2T finishes 2018 between 2.00% – 2.25% (this one could sting in next year’s review).

What Actually Happened – ouch. The 2T is 2.64%, but just a few months ago it was almost 3.00% so I missed this one by a mile. Does it help that I had a sense that prediction could sting?

LIBOR vs 10 Year Treasury

LIBOR Prediction – Powell is a continuation of Yellen and sends all the right dovish signals the market needs to avoid a meltdown. Powell will be very sensitive to the possibility of an inverted curve and will suggest the Fed is turning its attention to the long end of the curve through balance sheet normalization and may even suggest Fed Funds is at/near neutral rate.

The Fed hikes twice in the first half of the year, moving opportunistically with a steeper yield curve (a la post-election) to restock the ammo bin for the next recession. But the Fed does not hike a third time.

LIBOR finishes the year around 2.00%.

What Actually Happened – ugh. Powell turned out to be more hawkish than expected and is on record saying an inverted yield is not a concern for him. LIBOR is around 2.50% at year end. Not good.

10 Year Treasury Prediction – “For the first time in a long time, we think the 10T tests 3.00% in the first half of the year, maybe even spending some time north of there. While many economists are calling for an inverted yield curve in the first half of the year, we think markets will be feeling optimistic with the tax cuts, possible infrastructure bill, and generally strong data. The four factors we addressed (QE reversal, low growth, global yields, inflation) conspire for a general upward trend on long term rates.

The 10T finishes 2018 between 2.75% – 3.00%.”

What Actually Happened – boom goes the dynamite! Way to go out on top! Please don’t send me the “3.05% is the New Floor” newsletter, let me bask in my glory. Plus, I’m sure one of my kids will have it in my stocking tomorrow.