For the first time in 7 weekends, I am not writing this from a hotel lobby at 4am in the morning. That also means we finally got to eat dinner at home. My wife is a great cook and somehow manages to put food on the table for all seven of us pretty much every night. She’s a saint. We are her cross to bear.

Keeping everyone happy all the time is impossible. Every once in a while, a complaint bubbles up. And every once in a while, she actually gets a compliment. Or, at least what is supposed to be a compliment. On Saturday, our twelve year old decided to let her know she had done a good job.

“You know what saved this? The butter.” Remember, this is a 12 year old. That was a compliment in his book.

“Gee, thanks.”

“You’re welcome.”

“……………Tell me what you really think……….” she said under her breath.

Finally picking up on what she was putting down, he chose his words carefully. He was trying to make her happy…

“I mean, it’s not not good…”

And that is how a 12 year old compliments his mom’s cooking in my household.

Last Week This Morning

- 10 Year Treasury had a rough week, plunging to 1.47% on coronavirus fears

- German bund down 3bps to -0.43%

- Japan 10yr at -0.06%

- 2 Year Treasury sharp drop to 1.35%, nearly 30bps below LIBOR

- 30 Year Treasury hit an all-time low of 1.90% and closed the week at 1.915%

- Think about that for a second – 30 Year rates are just 0.30% above one month rates

- LIBOR at 1.63% and SOFR at 1.60%

- Michael Bloomberg, we hardly knew you

- A big thank you to Trump for draining the swamp of all those unfairly convicted federal prisoners that also just happened to contribute to his campaign

Yield Curve Control

I have a confession to make – I have failed you. About two years ago, we started keeping tabs on the German bund each week because the 10 Year Treasury was so closely correlated. I even added a little snippet in the “Last Week This Morning” section of each newsletter. We watched the Bund plunge from 0.60% to -0.40%, all feeling very relevant to domestic yields.

Then last summer as rates were plunging, I added a snippet on Japan’s 10 Year Bond in the newsletter. It felt like a good time to monitor their yields as the Japanification of our economy became increasingly more likely.

Each week, I would update Germany’s yield, which typically swung in lockstep with the 10T.

And each week, Japan’s bond would barely flinch.

And each week I would briefly wonder, “How come?” before I dismissed it as something about lack of growth, not being a legitimate alternative to the 10T, etc. Then I would move on to taking pot shots at Democrats and Republicans or my kids sports and forget about it until the next week when I repeated the cycle.

Until last week, I had no clue Japan had instituted a policy of Yield Curve Control in September 2016. I am in the interest rate business and I wondered weekly why Japan yields never moved, and I still didn’t figure it out until Friday. I am having a Brené Brown shame moment.

So what was my lightbulb moment?

FOMC Board of Governor Lael Brainard made a speech at the US Monetary Policy Forum that called for Yield Curve Control in the US if the Fed is forced to cut rates to 0% again and needs additional monetary tools to fend off a recession (https://www.federalreserve.gov/newsevents/speech/brainard20200221a.htm)

Ummmm…what’s Yield Curve Control? I’m glad you asked, because I have the answer!

We all know the Fed manipulates the curve (forward guidance, Fed-speak, cutting/hiking rates, QE, Reverse QE, Operation Twist, etc). But this is something much more specific.

In short, YCC caps the 10 Year Treasury yield at a certain level by actively buying/selling Treasurys to hold the yield constant or below a certain level. As with most monetary tools the US has been experimenting with over the last decade, Japan has tried this out before us.

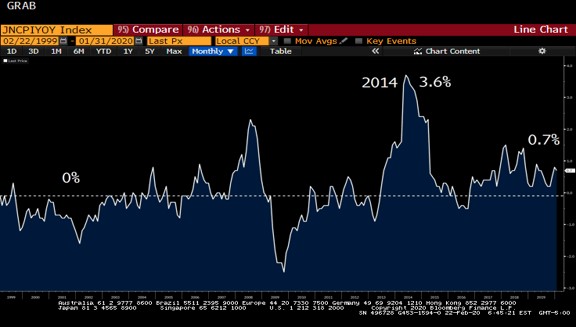

Before we take a closer look at this policy, take a look at Japan’s GDP and inflation, which are most closely linked to the term Japanification.

Here’s Japan’s GDP over the last 20 years – an average of just 0.2%.

Here’s Japan’s inflation over the last 20 years. A peak of 3.6% in 2014 driven by an increase in sales tax (I Googled it), with an average of just 0.1%.

Average GDP of just 0.2% and average inflation of just 0.1% – Japanification. Two lost decades.

In September 2016, Japan’s central bank decided to anchor the yield at 0%. Yield Curve Control.

So how has it worked out? Let’s zoom in.

I mean, it’s not not working…

But a negative curve out to 10 years for over three years and all Japan has to show for it is 0.7% inflation? Not exactly a smashing success, either.

This is different than Quantitative Easing. With QE, the Fed buys a set amount of Treasurys and mortgages each month. The goal was to keep a lid on yields, but that was really a byproduct of Treasury purchases. In fact, QE frequently results in higher rates because Fed accommodation leads to risk taking.

Yield Curve Control would involve capping rates out to a certain point on the curve. A Fed trader actually buys Treasurys each day if the yield gets close to the cap. Some days they do nothing, others they buy a ton to prevent rates from breaching the cap.

This could also steepen the curve because the Treasurys outside the caps get left out. If the Fed is focused on capping 3 year yields, the 5 Year Treasury may bump up a little bit.

Brainard’s comments are a shot across the bow. A lot has to happen before we end up in a position where the Fed is putting a cap on Treasury yields. Downturn. Slashing rates to 0%. Tepid response by growth/inflation.

But it’s clear the Fed is sending the market a signal. We have more tools in our toolbox than you are giving us credit for. They will focus on short term Treasurys first, matching duration with their own inflation expectations. If the Fed believes inflation will run below target for 3 years, they will put a cap on 3 Year Treasurys and less. Fortunately for us, the Fed does a great job of forecasting inflation…

But inflation has failed to breach 2.0% for a decade. How long before the Fed puts a cap on 10 Year Treasurys?

She also highlighted that aggressive forward guidance would provide market certainty and avoid repeating past mistakes by waiting too long. In fact, her speech is likely Exhibit 1 in the “Fed’s Next Economic Downturn Playbook.” Get out in front of it, send a signal, let the market digest, allow plenty of time to massage the message. And by saying this is on the table now, it likely keeps a lid on yields today as her speech serves as a type of forward guidance.

The fact that she is saying it at all means the Fed believes there is a scenario where it will need it.

Some quotes from her speech you will care about:

- First, in some cases around the world, unconventional tools were implemented only after long delays and debate, which sapped confidence, tightened financial conditions, and weakened recovery. The delays often reflected concerns about the putative costs and risks of these policies, such as stoking high inflation and impairing market functioning. These costs and risks did not materialize or proved manageable, and I expect these tools to be deployed more forcefully and readily in the future.

- Second, forward guidance proved to be vital during the crisis, but it took some time to recognize the importance of conditioning forward guidance on specific outcomes or dates and to align the full set of policy tools. In several cases, the targeted outcomes set too low a bar, which in turn diminished market expectations regarding monetary accommodation. In some cases, expectations regarding the timing of liftoff and asset purchase tapering worked at cross-purposes.

- Today’s new normal calls not only for a broader set of tools, but also a different strategy.

- The lessons from the crisis would argue for an approach that commits to maintain policy at the lower bound until full employment and target inflation are achieved. This forward guidance could be reinforced by interest rate caps on short-term Treasury securities over the same horizon.

- To strengthen the credibility of the forward guidance, interest rate caps could be implemented in tandem as a commitment mechanism.

- Based on its assessment of how long it is likely to take to achieve full employment and target inflation, the Committee would commit to capping rates out the yield curve for a period consistent with its expectation for the duration of the outcome-based forward guidance.

The Japanification of the United States officially takes another step forward…

There has been a lot of Fed accommodative/intervention in the last six months. Rate cuts. Not QE Repo Facility. Forward guidance saying no hikes this year.

Federal Reserve monetary policy should be like bumper bowling, intended to keep the economy out of the gutters. On one side, the bumper keeps us out of recession. On the other side, the bumper keeps us out of hyperinflation. The ball gently (or not so gently) bumps against either side from time to time as it rolls down the lane.

But the financial crisis changed that. The Fed had to take extreme measures to avoid a depression and total financial market collapse. Since then, we have become addicted to accommodative policies. Congressional policymakers have become overly reliant on the Fed Put instead of reaching across the aisle to create structural improvements to our economic system. But monetary policy can’t fix all ills.

In summary, the Fed now controls:

- short term floating rates like LIBOR through Fed Funds

- overnight repo (and by extension SOFR) through Not QE 4.0

- long term fixed rates through QE

- your 401(k)

And now introducing…Yield Curve Control!

The Fed is openly talking about buying Treasurys to keep a lid on yields while stocks are at all-time highs and unemployment is below 4.0%.

I’m not sure how we extricate ourselves from this addiction to Fed accommodation. If we can’t do it now, when?

Week Ahead

Investors will continue to monitor the coronavirus as its spread continues to pick up pace. Lots of economic data due out as well:

Monday – Chicago Fed National Activity, Dallas Fed Manufacturing

Tuesday – Consumer confidence

Thursday – GDP, PCE, Consumer Comfort

Friday – Personal Income and Spending, PMI, Consumer Sentiment