Last Week This Morning

- 10 Year Treasury up 15bps to 1.61%, the highest level since June and puts the March high of 1.75% in the crosshairs

- German bund up another 7bps to -0.15%

- 2 Year Treasury up 1bp to 0.32%

- LIBOR at 0.08%

- SOFR at 0.05%

- We added 194k jobs last month, well below the 500k expected

- The previous two months were revised higher by 169k, probably stealing from this month’s report

- Unemployment rate dropped to 4.8%

- That drop is artificial, caused by a drop in the labor force participation rate

- Average hourly earnings up 4.6%, right on top of forecasts

- Durable Goods came in as expected

- The debt ceiling was raised long enough to punt until December, when we will deal with it all over again

- Apologies to Bama fans for giving them the kiss of death last week

Jobs

Enhanced unemployment mercifully ended and drove 7mm job seekers back to the labor market, resulting in a gain of… 194k jobs. So… maybe not?

Last month’s gain was the slowest of the year and the first back-to-back monthly decline since the pandemic began. The Washington Post ran an article entitled, “America’s unemployed are sending a message: They’ll go back to work when they feel safe – and well-compensated.”1

Maybe I’m just cranky about job seekers dictating terms, but I want WaPo to ask a follow up question – “how exactly are you paying your bills?”

Unemployment insurance? Eviction moratoriums? Student loan forbearance? What, precisely is enabling allowing people to pay the bills if they aren’t working? Huge bitcoin gains?

Cynically, I believe the fear of covid preventing someone from working is directly correlated to someone’s ability to pay the bills without working. If you are able to make ends meet without working, you are more likely to cite “safety” as a reason for not going back to work.

I’m reminded of the Chris Rock bit on the convenience of food allergies. “We got so much food in America we’re allergic to food. Allergic to food! Hungry people ain’t allergic to sh*t. You think anyone in Rwanda’s got a lactose intolerance?!”

We’re so spoiled we can be allergic to food! I can’t help but wonder if the same is true for work.

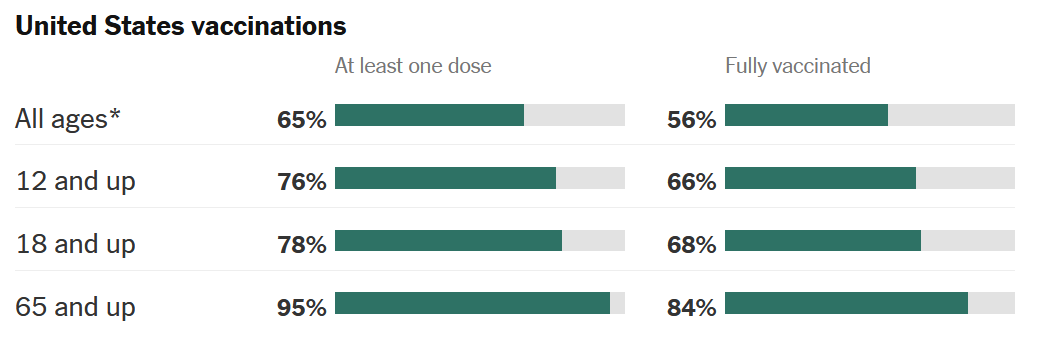

Furthermore, vaccines have been available for over six months now and almost 70% of the adult population has been fully vaccinated.

According to a NYT article, approximately 20% of the adult population is adamantly opposed to receiving the vaccine.2 Those people are unlikely to cite covid fears as the reason they aren’t looking for work. That means nearly 90% of the population is either fully vaccinated or not concerned, so the remaining 10% is what is preventing a full labor market recovery.

When I decided to get vaccinated, I recognized it didn’t make me immune from covid. In fact, three months later, I would be among the super special group to have a breakthrough case. But it was incredibly effective at taking hospitalization and death off the table (which was highly unlikely for me anyway). You know what – it worked! I got sick but thought, “Wow, how much worse could that have been?” But I never worried I was going to the hospital. It did its job. If I believe in the science that led me to being vaccinated in the first place, I shouldn’t also be able to ignore that science when determining my level of fear.

Very simplistically, a vaccine felt like a way to diminish covid to the severity of the flu. I never worried about getting the flu at a job, so the vaccine should help me get return to normalcy. If someone is fully vaccinated but opts out of working, what is their fear exactly? Maybe a loved one at home they worry about – sure. But that graphic above illustrates that the most at risk are also the greatest percentage vaccinated. There will always be unique cases that warrant that caution, but I don’t think it can explain the majority of labor shortages.

In case you haven’t picked up what I’m putting down, I’m not buying what the WaPo is selling. I don’t think fear of covid is preventing many people from returning to work.

There are theories floating around the people are re-prioritizing work life balance. Some are calling this the Great Reassessment. The Great Reevaluation. I worry it’s becoming The Great Justification. Potential job seekers are only as introspective about their careers as the government sponsored financial safety net allows them to be.

If someone is waiting on jobs that pay them more – good for them! Go get it! But we shouldn’t be footing the bill via unemployment insurance while they do so. They shouldn’t be allowed to skip lease payments while they live their best life. I get a sense that we’ve made it too comfortable to be out of work. There are more job openings than people unemployed, yet the number of people not in the labor force who cited covid as the reason they didn’t look for jobs rose last month for the first time since January, reaching 1.6 million.

While the cessation of enhanced unemployment didn’t cause a surge of job gains in September, I think it was unrealistic to expect 7mm job seekers to connect with employers in a single month.

I also think things like the labor force participation rate among women, at just 55.9%, is a far more likely, and legitimate, explanation for the sluggish job gains.

As the financial safety net is withdrawn, as money is spent on things or experiences the reality of paying the bills will gradually return. This will be a slow process, but I still think we will see strong monthly job reports for the foreseeable future.

10 Year Treasury

The 10T is testing a key technical level of 1.60%. Ultra-short ETF inflows exceeded $2B last month, the most since January 2020. The general market sentiment is higher yields.

We are approaching a point where convexity hedging could become an issue.

- If mortgage traders throw in the towel and hedge their books, we could see a run up to 1.80%.

- Alternatively, a failure of yields to climb could result in a short squeeze and the 10T fall back down to 1.40%.

Clear as mud, right?

I actually think the 10T is just about right, but those sorts of technical factors could cause a sharp movement one way or another in short order.

In the grand scheme of things, however, the market is not that concerned about sharply higher yields. Here are implied 10T forwards for the next three years.

y/e 2022 1.90%

y/e 2023 2.05%

y/e 2024 2.13%

Week Ahead

CPI and PPI data due out this week, as well as University of Michigan Inflation Expectations. All of these could certainly feed into a big 10T move. FOMC Minutes on Wednesday could also drive rates learn more about the discussions behind closed doors.

And since Penn State got ripped off by losing their starting QB in the second quarter, I really need the Eagles to beat the Panthers this week. I’m going to the game and can’t stand the thought of an office full of Panther fans mocking me all week. Fortunately, there’s also a NASCAR race today in Charlotte, so the fan base at the football game will be more…tolerable.

Sources: