Last Week This Morning

- 10 Year Treasury closed at 0.67%

- German bund -0.44%

- 2 Year Treasury down to 0.15%

- LIBOR at 0.16%

- SOFR is 0.13%

- We added 4.8mm jobs last month, bringing the alleged unemployment rate to 11.1%

- Consumer Confidence came in 8 points better than expected, at 98.8

- I have to wonder if this is artificially elevated because of the enhanced unemployment benefits

- CMBS delinquencies are on the rise

- I assume the governors that have ordered businesses closed stopped taking paychecks in March so they can better empathize

- How much more evidence does Trump need before he realizes Putin isn’t his buddy?

Jobs

The headline jobs gain was good news, with 4.8mm jobs added last month and a declining unemployment rate. But permanent job losses rose by 600k to 2.8mm, and that number is likely to increase as we experience another round of shutdowns.

- Leisure and Hospitality added more than 2mm. Of that, 1.5mm came from food services.

- Healthcare added 950k

- Retail added 740k

- Manufacturing added 356k

The number of people working part time for economic reasons fell by 3.1mm, but still stands at 2x the February level.

I worry that this headline number will make additional fiscal packages more challenging to pass. The current enhanced unemployment benefits are set to expire July 31st. We are not out of the woods yet and can’t tell businesses they need to shut down without providing some type of support.

We do, however, need to stop paying more in unemployment than people were making prior to the shutdown. An additional $2,400/month creates a perverse incentive system to avoid looking for work.

Lower Rates for Longer

I guess the Fed doesn’t like the term Yield Curve Control (YCC) because they have rebranded it to Yield Curve Targeting (YCT). At its last meeting, the Fed suggested it will further investigate YCT but is not convinced it needs to implement such a policy. Instead, the consensus is to use forward guidance.

Forward guidance usually comes in two forms:

- Data – typically referencing inflation, eg 2.0%

- Calendar – this is what the Fed did in 2012 when it committed to keeping rates unchanged until mid-2015

While data-driven forward guidance is common, calendar-based forward guidance is rarely used. But if the Fed says it will keep Fed Funds unchanged for the next 3 years, it will largely have the same impact as YCT the 3 year part of the curve.

From the minutes, “Many participants remarked that as long as the Committee’s forward guidance remained credible on its own, it was not clear that there would be a need for the Committee to reinforce its forward guidance with the adoption of a YCT policy.”

In other words, maybe just talking about monetary policy will be enough to keep a lid on rates without ballooning the balance sheet further.

In the near term, the primary cause of a movement higher in 10T yields will be market sentiment. The market moves in expectation of growth/inflation/etc.

The #1 cause of higher rates? A vaccine. But we’d happily exchange a 1.50% 10T for inoculation.

The #2 cause of higher rates? Improving data.

Check out the relationship between manufacturing data and the 10T. Notice how the relationship distorted with monetary policy intervention post financial crisis, but still tracked directionally. Will the market interpret another strong month of manufacturing data as a sign of an economic pickup and push the 10T above 1.00%.

10 Year Treasury vs ISM Manufacturing

Manufacturing is just one example. At some point this year, we will likely (hopefully) see an outrageous GDP print. Do rates spike? Or will the market dismiss it as simply catching back up?

These sort of data points and headlines could cause temporary volatility, but for the most part I believe volatility will dissipate as we settle into the new normal and this starts feeling like a normal recession. A fully loaded Fed bazooka helps, too.

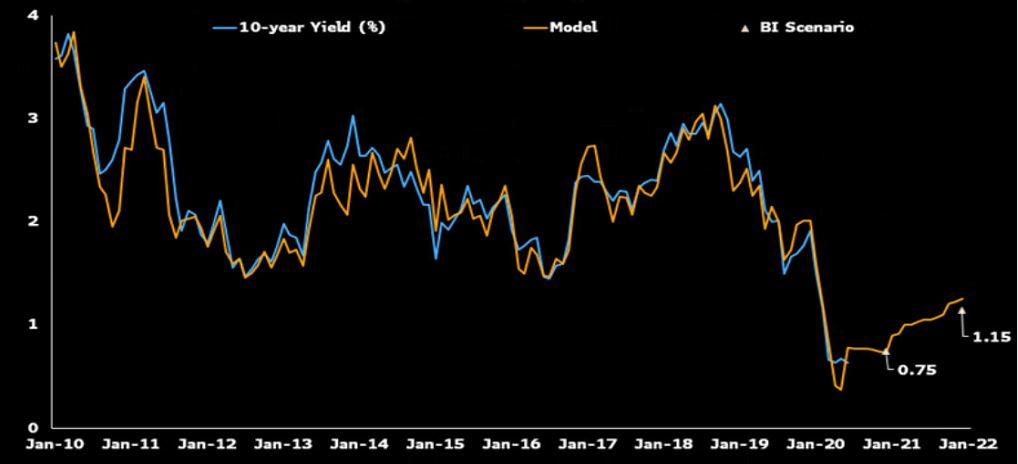

Bloomberg’s own model puts the T10 at 0.75% at year end and just 1.15% at year end 2021.

We are likely going to be dealing with low rates for a long time, and another decade of ZIRP can’t be ruled out.

Week Ahead

Pretty light data week, with some inflationary data being the primary headliners.