When was the first time you heard your kid drop the F-bomb? Mine was Friday. Well, really my wife heard it. At 12, he’s our youngest, so we’re probably holding on to his childhood a bit more than the others and this stung. It seems like only yesterday he was booing Tony Romo out of the Linc (what would end up being his final game)…the good ole days…

He’s in sixth grade, which means he moved up to middle school this year. His elementary school mascot was the Rockets, and his middle school mascot is the Wildcats. Apparently during the daily announcements, the principal likes to sign off with, “Once a Wildcat, always a Wildcat!”

My son takes grave offense to this. Over pancakes covered in 3 quarts of syrup, he says to her, “I am a Rocket, too, f*ck that!”

She froze. How would you have responded? My wife wanted to exact harsh discipline immediately. Send a message. That sort of language will not be tolerated. And in public no less!

But she also didn’t want to overreact and give him a response that might feed into it. She has exponentially more patience than me because that thought would never have occurred to me as I was grabbing him by the scruff of the neck. So instead she just said, “Buddy, we don’t use language like that, ok?” A simple, “OK” from him, and they went about their day. She’s so wise.

She was recounting this to me Friday night as we are prepping to head to the airport for another sports weekend. My phone gets a message, “Your flight to Orlando has been cancelled.”

It’s too late to rebook, and we need to be there at 7am Saturday morning.

“We need to drive,” she says.

“That’s eight hours!” I am incredulous. This isn’t the Olympics.

“If we leave right now, we can be there by 1am, let’s go. We’re already packed.”

“Drive eight hours!? Tonight?!”

“F*ck that,” I said.

From the mouths of babes.

We drove.

Last Week This Morning

- 10 Year Treasury fell 14bps over the shortened week to close out at 1.68%

- German bund also fell 12bps, closing at -0.34%

- Japan 10yr returned to negative yields, -0.02%

- 2 Year Treasury dropped back below 1.50%, closing at 1.495%

- LIBOR at 1.66% and SOFR at 1.54%

- The US had its first confirmed coronavirus case

- ECB held rates steady, but new president Christine Lagarde indicated that the persistent lack of inflation meant the ECB would remain accommodative despite seeing less downside risk now that the Phase 1 trade deal had been struck

Rate Decisions 2020 – The Three Most Important Factors

The Fed isn’t changing rates on Wednesday and Powell is going to talk (again) about how the committee considers current monetary policy as appropriate.

What the market really wants to know is – what are the long-term plans for the repo and why isn’t the Fed calling it QE? I don’t have an answer, and neither does the market. But the Fed’s balance sheet is ballooning again but according to them it is definitely not QE.

The market still expects a cut in Q4, while the Fed expects to begin hiking again next year. Either way, floating rate borrowers should not be concerned about materially higher rates anytime soon.

This year and next, here are the three most important factors driving an FOMC rate decision:

- Inflation

- Inflation

- Inflation

Yeah, that’s probably a cop out because I didn’t have to come up with a second or third one, but that doesn’t mean it’s any less accurate.

Expect Powell to highlight inflation as the driving force behind rate decisions in 2020. And while every client I have starts screaming about construction costs, just keep in mind it’s not popping up elsewhere.

Wage growth, in particular, has been stagnant. Although unemployment is at an all-time low, many people would consider themselves underemployed.

The Phillips Curve has been wrecked. Unemployment no longer has an inverse but stable relationship with inflation.

Continue watching for signs of inflation, but without we don’t need to worry about low unemployment alone causing the Fed to hike.

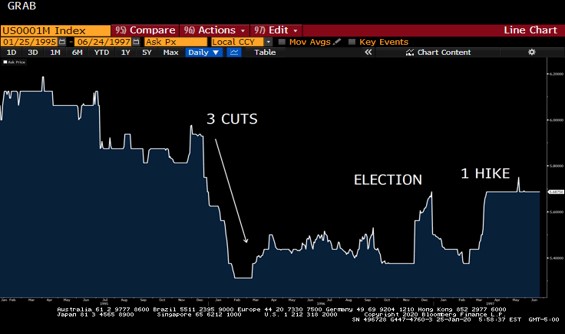

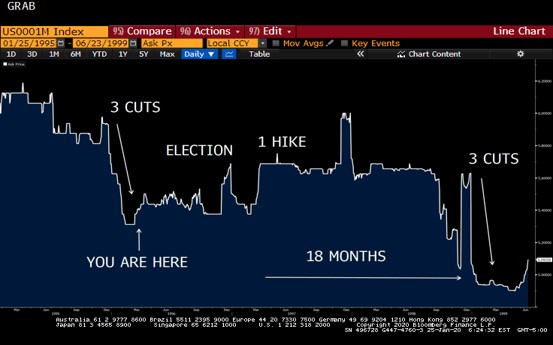

1996 or 2020?

We’ve highlighted this before, but it bears repeating. The similarities between this cycle and the 1996 cycle are striking.

- Following a significant tightening cycle (hiking rates), the Fed began cutting rates less than six months after the last hike

- The Fed quickly cut three times for a total of 75bps, and then remained on hold for most of the year leading up to the presidential election

- The sitting President’s re-election odds looked bleak, with consistently weak polling and a mid-term election butt kicking in Congress

- The opposing party’s challenger was an uninspiring 70+ something year old whose debate gaffes were the stuff of meme lore

- The sitting president won in a landslide (TBD)

- Both presidents were impeached (one after the election, the other before)

Four months after the election, the Fed hiked one time.

Eerily similar, right?

If the Fed can remain on hold this year and begin hiking next year (as they currently forecast), Powell would be ecstatic.

But keep in mind that 18 months later, the Fed had to cut another 75bps to avoid a recession.

Over the next two years:

- the upside risk of LIBOR is probably 2.25% (up 0.75%)

- the downside risk is 0% (down 1.50%)

Asymmetric risk/reward. Plan accordingly.

This Week

Potential for a volatile week as the coronavirus outbreak continues to develop, news on the trade deal continues to trickle out, and the FOMC meeting. You’ll note that impeachment news is unlikely to be a driver of rates because markets (and most people) don’t care. It’s a foregone conclusion, let’s move on.

Economic headlines will be dominated by finalized Q4 GDP as well as Core PCE, the Fed’s preferred measure of inflation. We just talked about how important inflation will be this year, so Thursday’s number could carry significance.

Oh yeah, England is set to finally leave the EU on Friday, January 31st.