A breakdown of the risk borrowers face on their interest rate hedges.

Can My Cap Provider Afford to Pay Me?

The surge in rates over the last year has many borrowers wondering if their Cap Provider can afford to pay them. This concern is exacerbated by the fact that a single Cap Provider largely dominated the interest rate cap space over the last decade. Here we will examine the potential counterparty risk.

Q: Do Banks Hedge Their Risk when I Trade with Them?

Yes.

The Hedge Provider is not making a bet against you - they are playing the role of middleman. They want to make some markup on each trade, but hedge the underlying risk so they are indifferent to rate movements just like you.

This is even more true after Dodd-Frank, which put tighter controls on risk taking by banks.

Q: How do they hedge it?

A trader’s primary job is to manage the bank’s risk as:

- Rates fluctuate

- Customer trades come in and out of their book

Interest rate traders don’t manage their risk on a trade-by-trade basis. They generally view their risk by size and term (duration). Cap traders have the added complexity of also managing where the trade falls on the vol surface. But even for billion dollar hedges, traders still view any new trade through the lens of how it effects their overall position, not as a single trade.

Traders view this risk as a net Mark to Market (MtM) risk. If you do a $50mm 3yr hedge with them and 10 minutes later another customer unwinds a $50mm 3yr hedge, they are back in neutral. There’s no need to chase each trade when they are managing a portfolio of hundreds of billions of dollars in net short/long positions. Their view is much more macro than your individual hedge.

Q: If my Hedge Provider lays off the risk to another bank, does this mean I should be worried about who my Hedge Provider hedged with?

No.

You only face your counterparty, and in the unlikely event one of their trading partners defaults, that doesn’t necessarily mean your Hedge Provider will default on payments to you.

Although you view the trade as one that will be on your books for 3 years, they don’t. When you hang up the phone, you carry that cap for the next three years. When they hang up, they hedge the risk based on the impact it had on their overall book.

It’s critical to understand that traders don’t view their risk on a trade by trade basis like you do.

- You view it as a cap you will own for three years

- They view it as a cap with a 3 year duration that impacts their overall risk

Although they hedge the risk your trade creates, they don’t hedge your cap individually. Over time, the 3 year risk your cap created is lost in the wash of thousands of hedges that the bank manages in the 3 year bucket at a macro level.

Q: Sure, but if other banks down the line default, doesn’t that create a potential domino effect that ultimately leads to my Hedge Provider not paying me?

Anything is possible, but keep in mind that interest rate desks collateralize each other at the end of each day by posting Treasurys to secure the net exposure.

Unlike credit default swaps, interest rate derivatives performed very well in the Financial Crisis from a systemic risk perspective. If Bank A had a net exposure of $100mm to Bank B yesterday, Bank B had to post $100mm in Treasurys to secure the exposure. If Bank B fails to deliver the Treasurys, Bank A stops trading with them immediately and can limit the exposure to the $100mm. Bank A would then take further steps to manage the interest rate risk (not the default risk) of that $100mm in exposure, driving it down as fast as possible.

The posting of Treasurys limits the potential damage, which in turn limits the likelihood that you won’t get paid. This process is managed through the ISDA Agreement and a Credit Support Annex, which spells out the terms of the collateral posting.

Dodd-Frank also created a Swap Data Repository that all hedges must be recorded in to help provide greater transparency and ensure regulators can better track systemic risk. All that paperwork you have to fill out for pre-trade helps facilitate this oversight.

Q: You spelled Treasuries wrong. The plural of Treasury is Treasuries, right?

No. We know it looks wrong, but when speaking about actual US Treasury obligations, the plural of Treasury is Treasurys. Use that at your next cocktail party. You’re welcome.

Q: OK smart*ss, thanks for the financial linguistics lesson. So what’s my real risk?

Setting aside outright fraud, which we have no reason to expect from any Hedge Providers and couldn’t control anyway, we view a more likely risk to be one of slow response time from a Hedge Provider. If they are downgraded, and thousands of ratings thresholds are triggered, they could be overwhelmed with trying to provide a remedy on all those hedges. This creates a logistical risk, but not a systemic one.

Please note that a rating downgrade does not mean they stop paying you. They may keep paying but be slow to remedy the downgrade trigger because they are simply overwhelmed.

In the unlikely event a Hedge Provider simply does not pay under a hedge and don’t remedy, they will be in default. This is where we pass the baton to a securities attorney.

Q: What are typical remedies?

Generally, these come in the form of:

- Posting collateral to you (either directly or to a trust account)

- Providing a guaranty from a counterparty that meets the rating requirements

- Assigning the cap to another bank that meets the rating requirements

Q: How do I best manage my risk?

Understand the rating triggers and remedies associated with each Hedge Counterparty and implement a process to monitor this. We do this for all our clients. We automatically track rating downgrade warnings, have the remedies clearly outlined, and contact information for each bank. We annually run a “In case of emergency, break glass” drill.

Or just work with us and we will take care of it for you (shameless plug).

Takeaways

- Your trade is managed by the impact it has on the overall risk profile

- Banks collateralize each other by posting Treasurys each day

- Regulators have created much better oversight and transparency via Dodd-Frank

- The plural of Treasury is Treasurys, not Treasuries

- If your Hedge Provider gets downgraded, it does not necessarily mean they stop paying you. They most likely keep paying you, but have to pursue a remedy since they no longer qualify based on rating requirements

Stop here if that did it. Keep on reading if you want to fall a little bit further down the rabbit hole and play trader for a day. Come on, take the blue pill…

Congrats - You’re a Trader for a Day!

Let’s make you a trader for a day. You sit down with 3 coffees, a WSJ, and an air of superiority.

What follows is so overly simplistic that it’s borderline offensive. Because caps have added layers of complexity involving vol surfaces and strike matrices, I am going to use plain vanilla rates trading for illustration purposes, but the concept applies to option trading as well.

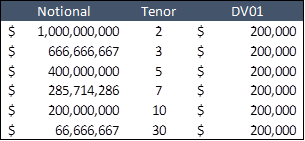

This first thing you must understand in trading rates is that duration (term) has a huge impact on your book. This is measured via a Present Value of a Basis Point calculation. I will ignore the pv impact to simplify things and use Dollar Value of a Basis Point for illustration purposes.

From a risk perspective, it would take 15 trades in the 2 year bucket to match a single trade in the 30 year bucket. This is a reason why traders generally focus on one part of the curve, but you are a super trader and are given free rein to trade wherever you see fit.

A trader’s house limit is generally referred to in terms of basis points. Let’s assume your DV01 limit per tenor is $150k and net overall $300k.

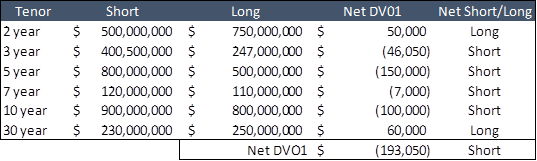

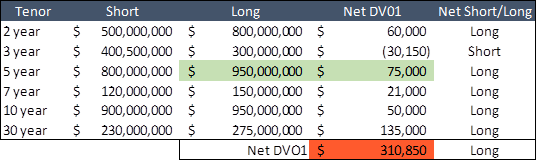

When you left yesterday, here’s how your book looked.

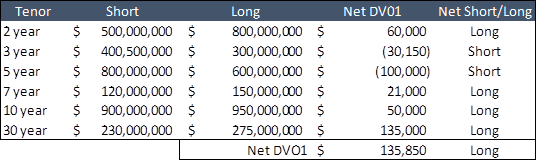

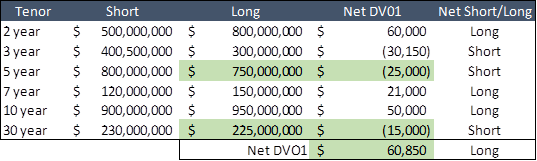

Your net risk was within authorization, but your 5 year bucket was right up against house limits. As rates moved up and down overnight, your position would have changed. You need to make sure you’re still within limits. European markets have pushed US rates around while you were sleeping, so here’s your current book:

The change in rates swung you from net short to net long, but still within limits. No need to immediately start hedging your book. As rates move up and down throughout the day, you will adjust your positions by buying or selling in the respective buckets to maintain a relatively neutral position and keep your bank safe.

You await the 8:30am data release, talk to your institutional team to see if there are any big trades expected, and talk condescendingly to your junior trader for botching your breakfast burrito order.

Then a pesky sales person says they have a real estate borrower that wants to lock a $50mm 5 year swap. Remember, the impact to your book will be largely based on notional and term:

DV01 = $50mm * .0001 * 5yrs = $25,000

If the salesperson is trying to sound cool, they might say, “I’m getting you longer $25k in the 5 year.”

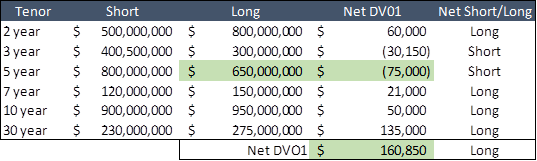

You instinctively know this won’t effect your position enough to matter, but here’s how it would look using our Excel trading book. You got longer (net less short) in the 5 year bucket and longer overall (but still within limits).

Note that you don’t care who the counterparty is - you only care about the DVO1 and the term. At no time did you ask, “who’s the borrower?” Their trade effected your 5 year bucket and that’s all you care about.

Because the impact is small, for the time being you don’t adjust your position. But as rates fluctuate throughout the day, your risk changes. You hedge that risk by laying it off to other traders. They have their own trading book and own risk, and it’s one big ecosystem of managing risk.

Throughout the day, the sales team brings you a lot of borrowers locking five year fixed. Even if rates haven’t moved, this gets you much longer in the 5 year bucket. You started the day with a 5 year bucket that was short $100k. Now you are long $75k. More importantly, you have now exceeded your net DV01 risk allowance. You are too long. With each basis point movement higher, you could lose a lot of money for the bank.

You have some discretion on how to get back within limits. The fact that you started the day $100k short in the 5 year part of the curve probably means you have a general thesis that 5 year rates will go up, and being $75k long stands in contrast to that. Plus, you aren’t an active player in the 30 year part of the curve and you could make that bucket less long, too.

You start pinging other trading desks, looking for someone to hedge with. Ideally, you will find someone that wants to get longer in the 5 year and 30 year part of the curve because they will charge less. In trading parlance, that’s called having an “axe”.

Your axe is to get shorter 5 and 30 years, so if you hear a trader calling around looking to get longer, they are a natural fit for your axe. You’ll try to trade with them before someone else does. If you can’t find someone that fits like a glove, you just have to pay a small bid ask spread. One way or another, within the next few minutes you will be selling 5s and 30s.

You are now back in a more neutral position and your bank is shielded from wild interest rate swings.

Now repeat hundreds of times and this is what you do all day long. A day in the glamorous life of a trader!

Before you close your book for the day, answer this: do you even remember that first trade at 8:30am this morning? No. It’s lost in the wash of that re-balancing you did all throughout the day.

And that's how traders view your hedges, too.

Takeaways

- Traders care about the impact a trade will have on their existing risk position, not the trade itself

- Banks manage this risk at a macro level, not trade by trade

- Being a trader is probably less glamorous than you think