Borrowers comparing term sheets often come across two options with similar terms – a balance sheet fixed rate and bank floater with a swap. In the past we’ve seen instances where the swap option had a lower rate while the fixed option had a declining flat percentage prepay schedule.

“Should we take the lower rate with the uncertain prepay penalty or opt for the higher rate with a defined penalty?” you might ask.

By leveraging a cancellable swap, you may be able to get the best of both worlds.

Below, we’ll look at how a swap can be structured to include a declining flat % penalty to rival that of the balance sheet fixed option.

Example

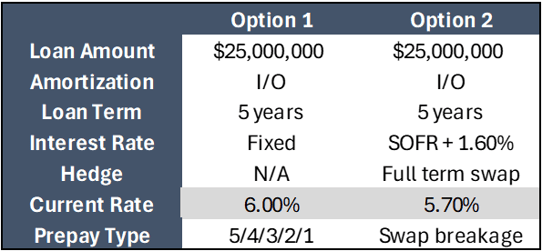

Assume a borrower is comparing two term sheets with the following high-level terms.

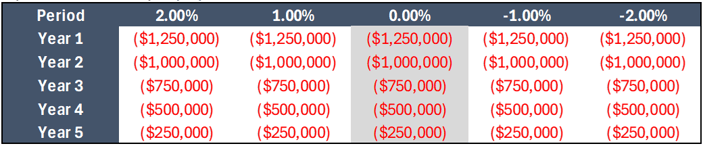

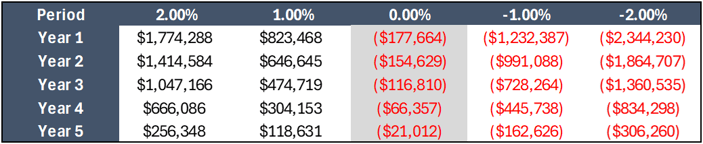

If the borrower goes to prepay in the future, here’s how the two options compare. Note, both assume a mid-year payoff.

Option 1 – flat % prepay

It doesn’t matter what rates do, the penalty only changes if you wait longer to prepay.

Option 2 – swap breakage

The breakage is a factor of the rate you locked in, replacement swap rate, and remaining term.

In other words, the flat % option is always known whereas the swap can be meaningful asset or liability to the borrower. Here’s where the cancellable swap comes into play. If you’d like the 101 overview of a cancellable swap, check out our resource here first.

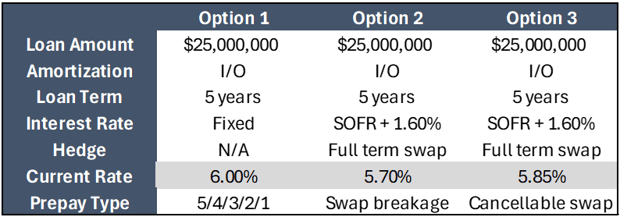

Cancellable swaps are extremely flexible and can be structured in countless ways. One potential option is a termination feature that provides a max penalty that declines each year. Said another way, a swap with a 5/4/3/2/1 structure can be set up to rival the balance sheet fixed option.

The rate on that option would be around 0.15% higher today. Here’s our new comparison.

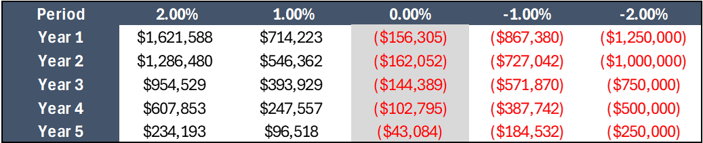

And here are the breakage scenarios for the 5/4/3/2/1 cancellable swap

-

If rates are higher, the borrower can terminate the swap and still get to recognize the upside

- If rates are slightly lower, the termination option has value that’s recouped as part of the unwind and the penalty is still lower than the vanilla swap

- If rates are much lower, the option is exercised and the borrower pays the flat % penalty to get out of the swap

Side note, yes, we know your lender wants you to do swaps with them. We’re not here to replace them, we’re bringing our expertise to your side of the table. That includes pricing discussions, ISDA negotiation, verifying the rate when you go to lock, and strategic dialogue to dial in on the optimal structure for your scenario.

For context, here are the approximate premiums for a few other cancellable swap scenarios:

- 3/2/1/0/0 – 0.43%

- Swap breakage years 1-3, 2.00% years 4-5 – 0.10%

- Swap breakage years 1-3, 1.00% years 4-5 – 0.18%

- Swap breakage years 1-3, 0.00% years 4-5 – 0.33%

- 2.00% all 5 years – 0.29%

- 1.00% all 5 years – 0.53%

- 0.00% all 5 years – you don’t want to know!

Interested in discussing cancellable swaps further or weighing other potential strategies for one of your upcoming financings? Give us a call at 704-887-9880 or email us at pensfordteam@pensford.com.

Helping negotiate and place swaps directly with the underlying lender is one of our core competencies. Your lender’s swap desk is looking out for their interests. Let us help you look out for yours.

Pensford has been a trusted partner of real estate investors for over 17 years. Our deep industry expertise and transparency enables our clients to make informed decisions, helping to protect their investments from market volatility and ensure stability.