If you’re currently weighing sale/refi options or are looking at an acquisition and would like to run a prepayment penalty, we have calculators that can help.

Fixed Agency Prepayments – Yield Maintenance

If you’re an Agency fixed borrower, then you’ve likely been subject to a yield maintenance (YM) penalty or two. While many borrowers know where to go for a defeasance calculator (there’s no shortage out there), there’s only one online YM calculator that uses the Fannie/Freddie methodologies and can be used to forecast penalties on outstanding or prospective loans.

This write up is specifically intended to walk through how to use our Agency YM calculator. Before we dive in, here’s the link you’ve all been looking for: Pensford Agency Yield Maintenance Calculator

What Do I Need?

In order to run an Agency style YM, the following info will be needed:

- Loan Amount

- First Payment Date

- Note Rate

- I/O Periods / Amortization Terms

- Minimum Penalty (it’s almost always 1.00%)

- YM Period Term

On Fannie loans this info is frequently found in Schedule 2 (near the end of the Loan Agreement). It’s common that Freddie senior loans are subject to defeasance, but fixed supplemental loans are frequently YM and the details for the calculator can be found in the Note.

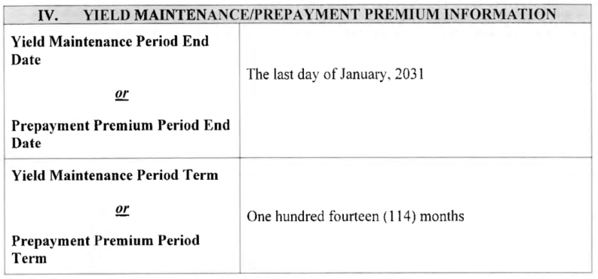

If you’re wondering what “YM Period Term” is, it’s the number of months that yield maintenance applies to the loan and tells the calculator how far to go as well as influences what the “replacement rate” used in the calculation is. Most 10-year Agency loans have 9.5 years YM, meaning the YM Period Term is 114 months.

We’ve included a sample from a Fannie loan document below to illustrate this data point.

I’ve Got the Terms, Now What?

The prepayment penalty will generally be the greater of (i) 1.0% of the outstanding principal balance, or (ii) YM as calculated per the terms in the Loan Agreement. We won’t bore you with all the math, that’s why we built a calculator to take care of the heavy lifting. We just want you to know how to use it.

Now that you’ve gathered your terms, you’ll want to make it over to our calculator and input the relevant data. We’ve included an image and text explanation of the fields below.

.png?width=700&height=634&name=image%20(3).png)

- The YM Prepayment Date will typically fall on the last day of the month you wish to prepay, just prior to the next payment date.

- The Loan Amount and First Payment Date will establish the proper dates and balance for the commencement of amortization.

- The YM Period Term will tell the calculator how far out to go. Once you input the term, the YM Period End box will populate the date which should correspond with your loan documents.

- The Rate is used alongside the Day Count to properly amortize the loan. Once you input these factors, the calculator will build an amortization schedule which should result in Balance at Prepayment which ties out with your loan.

- As mentioned previously, the Minimum Penalty is almost always 1%, but be sure to check your loan terms in case your loan falls outside standard assumptions.

- Just like the YM Period Term, the Amort Term and Interest Only Period will establish the proper amortization.

At this point, all your inputs should be entered properly and all you have to do is hit the fancy gold “Calculate” button and voila! Like magic, you now have a detailed breakdown of your prepayment penalty along with a burndown chart displaying your projected penalty as time progresses, based on forward rate projections.

If you like to save calculations, a download of the output is available outlining all of the relevant loan and property details entered. Just click download and it’s yours.

Bonus – we promise that a pesky sales guy won’t start calling you just because you downloaded an estimate!

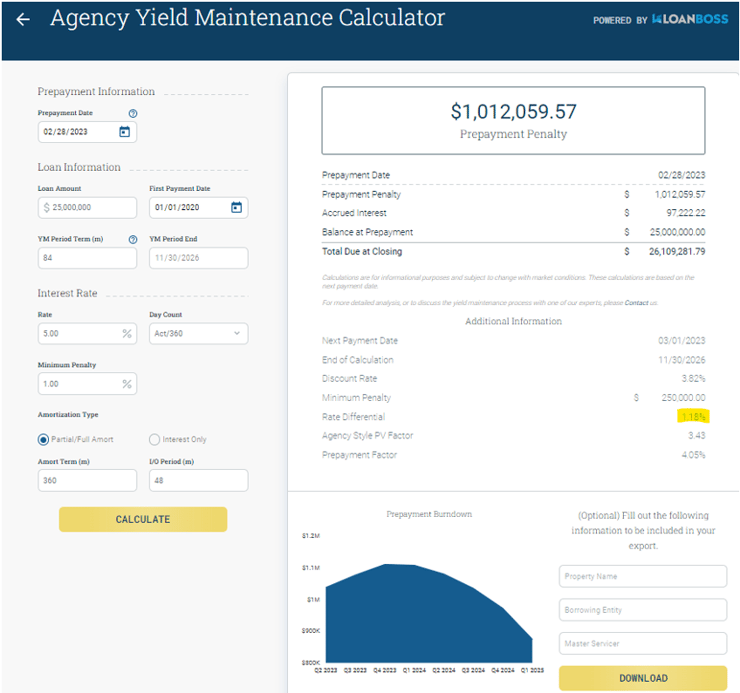

Let’s look at an example:

As you can see in the below screen capture, the inputs spit out a rate differential that is higher than 1%. Therefore, this loan does not qualify for the 1% minimum and a $1.01mm YM penalty would be due.

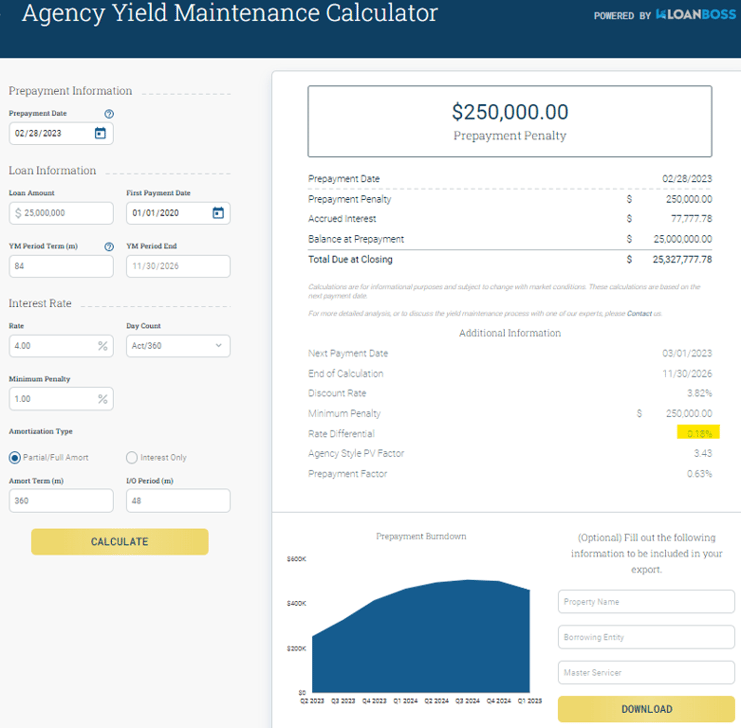

Here’s an example where the 1% minimum penalty applies:

As seen in the image below, the difference between the Note Rate and Replacement (discount) Rate is 0.18%. Therefore, the penalty in this example is 1% of $25mm, or $250k.

Some Key Notes/Caveats

- The replacement Treasury rate used in an Agency YM calculation is determined 25 Business Days prior to the prepayment. Our online calculator uses spot rates, so if you’re within 25 BD from your closing, let us know and we can run a more precise number for you offline.

- If all the details from the Loan Agreement/Note are input into the calculator correctly, the “YM Period End” our calculator spits out will match the YM Period End listed in the Loan Agreement. This along with the balance at prepayment should be a good sanity check that you have it built up correctly.

- The YM calculator only applies to loans that are no longer in lockout but are still within the YM Period. If the prepayment date is outside of the YM Period End, then either a flat 1.00% penalty or prepay at par applies.

Conclusion

If you’re currently weighing sale/refi options or are looking at an acquisition and would like to run a prepayment penalty, we have calculators that can help. Check out Pensford Calculators to get a feel for what your prepayments could look like.

We encourage you to reach out with any questions surrounding prepayments at PensfordTeam@Pensford.com or feel free to give us a shout at 704-887-9880.