Floating rates have risen rapidly over the course of 2022, naturally bringing loan floors higher with them. With markets suggesting we may be approaching the peak, negotiating floors out of the loan, or at least lower, has become increasingly critical. Said another way, if you wish you bought a cap a year ago, you might wish you considered the floor on a new loan a year from now.

Before we dig into the impact it could have on your financing, let’s take a look at how floating rates typically behave following a tightening cycle.

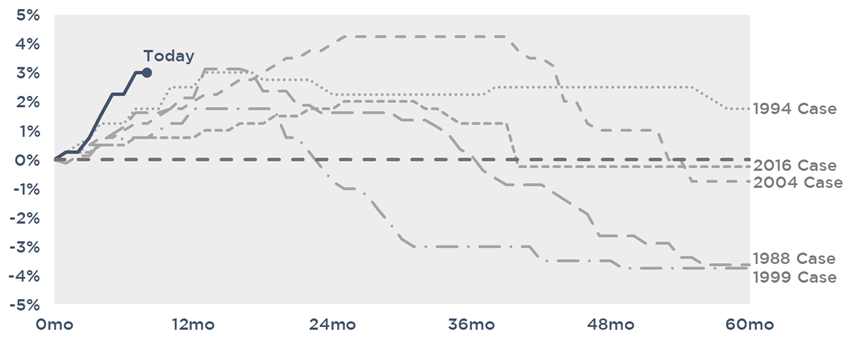

Rate Expectations

The below graph illustrates the path of Fed Funds during the previous five tightening cycles. In each case, with the exception of the 1994 cycle, the Fed cut dramatically an average of about nine months after they stopped hiking.

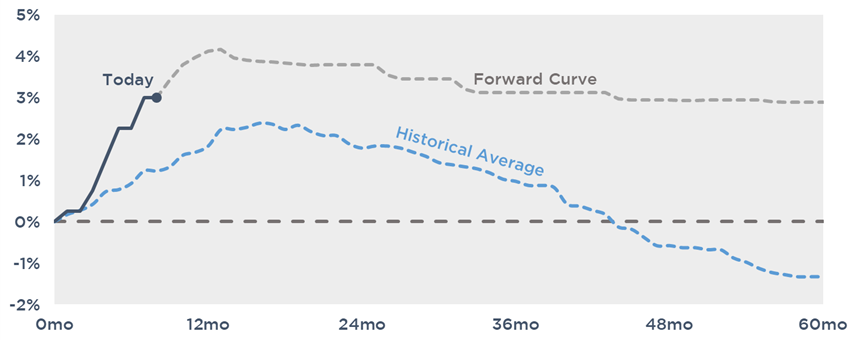

Now, let’s compare that to today’s cycle, where markets are projecting the Fed to hold rates above 3% after they’re expected to stop hiking in the first quarter of 2023.

Assuming the rates level off early next year, will the Fed actually be able to maintain a higher rate environment, or will they wind up slashing rates below expectations as they have in previous cycles? If this tightening cycle behaves in line with historical trends, we could wind up in a materially lower rate environment over the next few years.

Impact on Floating Interest

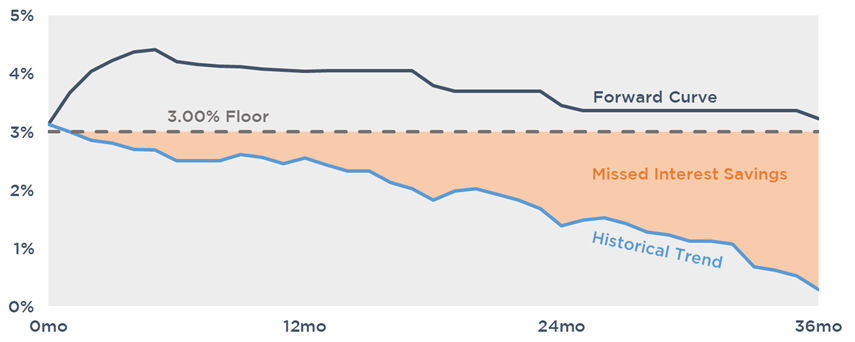

By way of example, let’s assume you recently closed on a $25mm three year floating rate loan with a floor set at SOFR at the time of closing, or 3% in this case.

If rates follow expectations, you’d be indifferent to the floor since markets are expecting floating rates to remain above 3.00% through loan maturity. However, take a look at what happens if rates were to instead fall back in-line with historical trends. Over time, SOFR would become further and further below the floor, leaving considerable interest savings on the table since you’d still be paying 3.00%.

In this example, the floor would wind up adding $850k of interest expense over a three year period. If rates follow today’s expectations, the total interest expense is projected to be $2.935mm. However, if rates follow the historical trend and you have no floor, that total is closer to $1.5mm, or about $1.4mm less.

Conclusion

Although they’re frequently overlooked or downplayed, negotiating loan floors has become especially important as floating rates potentially near their peak. For help identifying how your loan floor could impact your floating rate financing and solutions to negate its impact on your rate, reach out to the experts at pensfordteam@pensford.com or (704) 887-9880.