Regional banks have become much bigger players in the swap market over the last five years. Rather than establishing their own trading desk, they partner with a third party firm to outsource these operations. Some firms include:

DerivativePath

B&F Capital Markets

Chatham Financial

FHN

This allows the regional banks to offer a swap to compete against the larger banks, plus it creates additional revenue. This is frequently referred to as a back to back, or B2B.

Dodd Frank Mid

There’s another big difference between the regional banks and the huge bank – the regional bank does not have to disclose the Dodd-Frank mid at execution.

Prior to Dodd-Frank, banks did not have to disclose their mid-market rate. A swap marketer could simply quote a rate and the borrower either locked it in or didn’t. They had no idea whether the credit charge was 10bps, 30bps, or 50bps.

Dodd-Frank required the large banks to disclose this number. When you lock in a swap with a large bank, they will say, “Our Dodd-Frank mid is 0.75%, we have an agreed upon credit charge of 0.25%, plus a 2.00% loan spread, equals an all-in rate of 3.00%. Can we be done at 3.00%?” And then you lock in.

Sidebar – many borrowers don’t realize the credit charge is on a per annum basis. A 25bps credit charge on a 10 year swap is really 2.50%. This is present valued and recognized as upfront revenue. On a $25mm 10 year swap, that’s the pv of $625,000 as soon as you lock in the rate.

Even if you are aware of that, regional banks do not have to disclose the Dodd-Frank mid. So rather than breaking it down into individual components that might lead to you asking, “Hey, what’s the 25bps credit charge you just mentioned?”, you just hear the final rate. And you lock.

Multiple Mouths to Feed

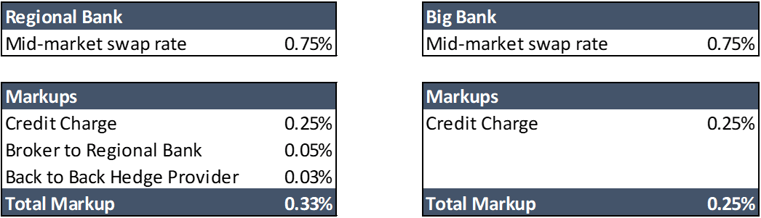

Whether you are a big bank or a regional bank, the swap creates credit risk. Therefore, banks are entitled to earn a credit charge on this risk.

For a regional bank without its own swap desk, there are some additional components. The firm that is serving as the outsourced swap desk usually receives 4-6bps in the rate. The ultimate hedge provider (a big bank) also typically receives 2-3bps.

You lock in 1.08% instead of the 1.00% you may have been quoted by a bank with its own swap desk.

In that same example as before ($25mm 10yr), that’s an additional $200k of interest expense to you.

It’s important to isolate, quantify, and negotiate each individual component.

This is especially important since regional banks are more likely to offer longer term loans (7 and 10 years) than the big banks, and this translates into much more revenue.

Credit Charge

If asked about credit charge, the regional bank will typically reference their credit charge.

“What’s your credit charge on this?” – borrower.

“25 basis points, which is normal in this market,” – regional lender.

But they avoid mentioning the total markup.

Case Study 1

Two phase mixed use in Houston, Texas. Borrower had already locked in half of the debt, was getting ready to lock in other half of debt. Borrower had specifically asked about the swap profit on the first swap and was told 25bps.

Our analysis showed that the swap was executed at least 36bps over mid, an increase of $157k of swap revenue to the bank.

The lender had not disclosed the additional 4bps to the broker and 3bps to the back to back provider. On subsequent phone calls, it was determined that the swap had generated an additional 3bps that was not rebated back to the client even though it exceeded the agreed-upon 25bps.

On the second swap, we negotiated a lower rate, received a refund from the overage on the first swap, and significantly improved the ISDA Agreement.

Case Study 2

Mid-sized office loan in the southeast. Borrower engaged us just to assist with the ISDA agreement negotiation. Our attorney quickly negotiated several key points in the borrower’s favor.

While doing that, we also determined that the lender was charging 35bps themselves, plus another 10bps between the broker and the back to back hedge provider. That was a total markup of 45bps.

We were able to negotiate the bank’s credit charge back down to 25bps, the broker’s fee to 4bps, and the back to back hedge provider to 2bps. The total savings was $140k.

Case Study 3

It was too late when we heard from this borrower. They had just locked in a 10 year swap on a large manufacturing facility in Pennsylvania. We reviewed the swap and it had generated more than $1mm of swap revenue for the regional bank.

While we couldn’t help them on this swap, we were able to illustrate the pricing to the banker. This was used as leverage to negotiate much better forbearance terms.

Conclusion

Regional banks offering swaps often involve multiple parties and additional complexities. Pensford can help negotiate the pricing and the ISDA while maintaining a strong relationship with the lender.