I work hard to not turn these newsletters into advertisements. Every once in a while, however, I cash in those chips and ask a favor and today is one of those days. It’s only 60 seconds of your time and then we’ll get back to the interest rate stuff.

Two years ago, we launched LoanBoss with the following quote: “If I had asked people what they want, they would have said a faster horse.” – Henry Ford.

Since then, LoanBoss has become the #1 rated debt management software in the industry. This is not a cute experiment or a little app. This is enterprise software that runs over 1 million calculations a day. Live interest rates. Loan abstract templates with 344 fields. Fully customizable BI tools. We have borrowers, brokers, and lenders all using the software. Asset managers are the primary users, but more and more capital markets teams are using the pipeline tools. If you’ve ever asked yourself, “Shouldn’t this have been automated by now?”, you should check it out.

The #1 thing we hear on demos is, “Wow, this does way more than I was expecting.” Seriously, schedule a quick demo and see for yourself. Not one single person, ever, has said, “I don’t see it.” One good friend in the business said, “Honestly, I checked this out as a favor to you, but this is incredible. This is going to change the industry.”

We recently polled our customers of their favorite features. I am fan of the complex calculations and whiz bang What If Analyzers, but sometimes it’s the blocking and tackling that people love.

- Don’t scroll past this one. Never pull loan docs again – just click a button and the section you need pops up.

Think about every asset you own or are chasing. Every financing. Every deadline. Every calculation. The complexity is mind boggling, yet the system of record is…Excel? With all the advancements in technology, can you really envision a scenario where you aren’t managing your debt in a software platform five years from now? How much data will flow in and out of your firm during that time that will be lost?

Check out our website and I bet you’ll see something that resonates. Heck, we even have self-guided demos so you millennials don’t have to talk to a pesky human until you are ready.

Optimize your debt. Win more deals. Preserve institutional history.

Thank you for indulging me. We now return to our regularly scheduled programming.

Last Week This Morning

- 10 Year Treasury broke 1.50% before settling in at 1.46%

- German bund up 6bps to -0.22%

- 2 Year Treasury up 1bp to 0.26%

- LIBOR at 0.08%

- SOFR at 0.05%

- Core PCE (Fed’s preferred measure of inflation) came in at 3.6%

- University of Michigan Inflation Expectations

- 1yr: 4.6%

- 5-10yr: 3.0%

- Durable Goods surprised to the upside

- Debt ceiling isn’t a thing…or wait, it still is? I can’t stay on top of it

- PSU might be #3, but it’s a steep drop after #2. Let’s face it – it’s Bama and UGA this year

10 Year Treasury

First thing’s first – Biden’s budget isn’t causing the 10T to spike because of its absurd name it will be paid for with tax hikes rather than issuance. I’m not going to fall down the rabbit hole of whether he should be hiking taxes right now, but just know that the market’s non-reaction is attributable to that. Compared to Covid stimulus, which was entirely funded by Treasury issuance, the impact on future issuance is muted. Therefore, the market response has been as well.

Now, with that out of the way, the recent jump in yields has many borrowers asking, “Should I lock in before the 10T climbs higher?” Maybe. If you plan to be in the financing for the long term, of course it makes sense to lock for 10yrs with a 1.50% T10.

But keep in mind that the 10T tends to climb in anticipation of the hike, then waits for the front end to catch up. This is the steepening you have been reading about (the spread between the T2 and T10 widens).

But once the Fed actually starts hiking, the 10 Year Treasury doesn’t necessarily keep climbing. It was already pricing in some number of hikes, so it moves based on changes to those expectations. If the market has done a good job of pricing in the right number of hikes, the 10T stays flat while the front end of the curve catches up. This flattens the curve.

We are in the “front running the hike” phase – the 10T is trying to figure out the ultimate path of Fed Funds. It will settle in and wait for Fed Funds to catch up.

Source: Bloomberg Finance, LP

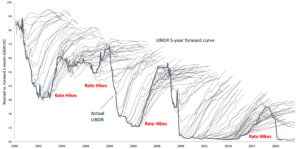

In our (in)famous Hairy Graph below, you the grey hairy lines represent market expectations for the path of LIBOR at any given moment. The solid dark line is what actually happened. The market almost always overestimates the path of Fed Funds.

Do you know when the market underestimates the path of LIBOR? When the Fed actually starts hiking.

Bottom line – Generally speaking, the best time to lock is right before the Fed starts hiking.

- You avoided paying up a bunch when the 10T front ran the tightening cycle

- You lock in at a time when the market is underestimating the path of floating rates

Where do we go from here?

I think the 10T may struggle to breach 2.0% until the market feels confident rate hikes are on the table. A range of 1.50%-1.75% feels about right. Here’s Bloomberg’s forecast for the 10T. If you’re still considering floating rate debt, you can probably pick up 150bps or more for the next few years.

Week Ahead

Big news this week will be the jobs report on Friday, with a forecast of 470k jobs gained and a 5.1% unemployment rate. It would take a huge deviation from expectations to shift the Fed’s tapering plans, but the Fed’s increased focus on jobs means every number carries extra significance.