With the Fed on hold and cap pricing elevated, more borrowers are revisiting costless hedge structures, whether that’s a swap or a traditional collar. Both put a ceiling on rates without an upfront premium, and both come with similar risks - potentially miss out on floating lower and/or owe a breakage if the trade is unwound early.

The staggered collar is a structure built around that exact concern. It preserves the costless nature of a vanilla collar but engineers an “open window” later in the term. Once the floor expires, the loan is effectively open. For borrowers drawn to the costless nature of a collar but worried about prepay flexibility in the back portion of the loan, it’s worth a look.

A Quick Refresher on the Vanilla Collar

In a costless collar, you simultaneously buy a cap and sell a floor to the bank. The premium received from selling the floor offsets the cost of the cap, leaving you with a $0 net premium. The cap protects you above its strike. The floor obligates you to pay the bank if SOFR sets below the floor strike.

For a deeper walkthrough of the mechanics, see Collars 101 and What About Collars?.

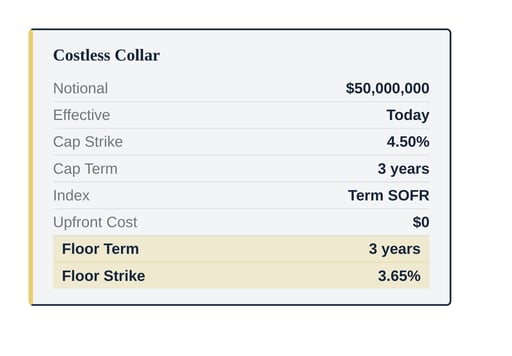

Below, we’ve outlined sample pricing for a vanilla 3 year costless collar. A borrower wanting to purchase a 4.50% strike cap today would need to sell back a floor around 3.65%.

Sample Vanilla Collar Pricing

The Prepayment Risk

Like swaps, collars have a two-sided value. If you exit early and rates have fallen, the floor you sold has gained value while the cap you bought has lost value, and the difference is what you’ll owe to terminate. The good news is that a collar’s breakage is almost always less than an equivalent term swap. The bad news is that it’s still nonzero, and it scales with how far rates have fallen and how much term remains.

Below is the estimated breakage over time and under different rate environments for the buy 4.50% / sell 3.65% vanilla collar.

Vanilla — buy 4.50% / sell 3.65%

- The 0.00% column shows what the breakage would be if today’s forward curve plays out.

- With 1 year remaining and the forward curve unchanged, the breakage would be roughly $58k.

- If rates are 1.00% below current expectations, implying a ~2.73% 1 year swap rate, the breakage increases to roughly $446k.

The prepayment risk in the final months is the risk a staggered collar is designed to remove.

Enter the Staggered Collar

A staggered collar is structured so the floor matures earlier than the cap. The cap stays in place for the full hedge term, but once the floor expires, the loan is effectively open. Recognize any upside from floating below the floor over the remaining term and there’s no prepay penalty if you exit. Only the cap remains, and a cap’s value can never be negative to you.

The trade off is straightforward. Shortening the floor reduces the premium received from selling it, so the floor strike must move higher to keep the structure costless.

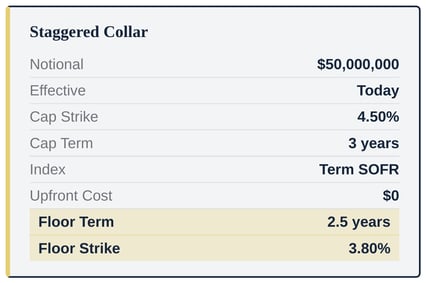

Building on our example, if the borrower wanted to sell back a 2.5 year floor but still obtain the same 3 year 4.50% cap, the floor strike would need to be around 0.15% higher.

Sample Staggered Collar Pricing

The Benefits

- Costless at execution. Same $0 premium as the vanilla collar.

- An open window later in the term. Once the floor matures, you have full prepay flexibility since there’s no breakage.

- Ceiling protection stays in place. The staggering only affects the floor. The cap continues to protect you for the full hedge term.

Here’s the estimated breakage profile of the same structure with the floor shortened to 2.5 years:

Staggered — buy 4.50% 3 years / sell 3.80% 2.5 years

- The 6-month row tells the story. At that point the floor has terminated, leaving just the cap, and there’s no rate scenario that results in a liability to the borrower.

- The staggered breakages are also tighter than the vanilla throughout the floor period, since the staggered floor has less remaining term.

- At 1.00% below expectations the staggered collar MtM is effectively $0 whereas the vanilla collar has a ~$220k liability.

Higher Floor Risk vs. Prepay Risk

The risk of the staggered collar is the higher floor. If rates are below expectations, you’ll pay up to 0.15% more over the first 30 months of the loan. That’s up to ~$188k of additional interest over the life of the hedge. Let’s compare that to the potential breakages at month 30.

Vanilla — buy 4.50% / sell 3.65%

Staggered — buy 4.50% 3 years / sell 3.80% 2.5 years

In order for the vanilla collar breakage to exceed ~$188k, rates would need to be roughly 0.85% below current expectations. This shorter floor term also means a lower breakage at most other points throughout the loan too.

The flip side is also worth considering. If rates remain firmly above the floor and the loan isn’t prepaid, the staggered collar structure costs the same as the vanilla collar ($0). Even in a world where rates quickly move below the floor, the staggered structure provides an opportunity to recognize some of that upside during the final 6 months of the hedge.

Bottom Line

A vanilla collar gives you costless protection with prepay risk. A staggered collar gives you costless protection, full term ceiling coverage, and an open prepay window later in the deal, in exchange for a higher floor while the floor is active.

Interested in discussing costless collars further or weighing other potential strategies for one of your upcoming financings? Give us a call at 704-887-9880, email us at pensfordteam@pensford.com, or respond directly to this.

Helping place swaps and collars directly with the underlying lender is one of our core competencies. Your lender’s derivatives desk is looking out for their interests. Let us help you look out for yours.

Pensford has been a trusted partner of real estate investors for over 17 years. Our deep industry expertise and transparency enables our clients to make informed decisions, helping to protect their investments from market volatility and ensure stability.