Let’s see how many Cowboy fans we can get to unsubscribe today…

The Eagles just won the Super Bowl against the greatest QB of all time and the greatest coach of all time with a backup QB coached by a guy whose only previous head coaching experience was high school football. Imagine what we’ll accomplish next year with Wentz back at the helm! Colonize Mars? Easy. Control construction costs? Piece of cake. Help Dallas advance to the second round? You got it Jerry. Is there an Intergalactic Bowl? I feel like playing other humans isn’t challenging enough at this point…yeah, we’re going to be even more insufferable than you feared. We don’t know how to handle winning and it will show.

Last Week This Morning

- Not sure if you heard, but the Eagles won the Super Bowl, causing mass panic and an immediate flight to safety Malcom Jenkins.

- The 10 year Treasury plummeted like Tom Brady’s stock as a wide receiver, dropping from 2.84% to 2.70%.

- On Tuesday, the 10T climbed higher than Nick Foles’ trade value and was back in the 2.80%’s.

- The 2 year Treasury started the week at 2.18%, plummeted to 2.02%, and then rebounded to 2.07%.

- Carolina treated Duke like it was Brandin Cooks. There hasn’t been a knockout like that since Debo demanded his bike back. Have I mentioned that it was a great sports week?

- German Bund hit 0.77% and finished the week at 0.75%.

- Budget deal was signed through the midnight hours Friday night, which includes a debt ceiling increase and a sweet Super Bowl ring for the Iggles from Philly.

- The Patriots didn’t punt the ball…and lost.

Vicious Monetary Cycle

In last week’s newsletter, we talked about the march to 3.0% on the 10 year Treasury. The very last sentence of the newsletter read, “Keep an eye on stocks, as a sell-off could be the only thing preventing a continued march higher by rates in the near term.”

We didn’t have to wait long, as Monday morning brought out a mini flash crash that sent equities plummeting and the 10T back down to 2.70%.

Order was quickly restored once it became clear the movement was largely algo-driven and the T10 rebounded into the 2.80%’s.

It is important in moments like this to remember that there is a difference between markets and the economy. Nothing has changed with the underlying economy, so we do not expect a sharp reversal in the near term. A 3.00% is still firmly in the crosshairs.

Will the Fed suddenly change its tune about a march hike? Probably not – not as long as we don’t continue to see volatility like we saw last week. But it likely sat up and started paying attention. If markets start to protest three hikes this year, Powell may be tested earlier than anticipated.

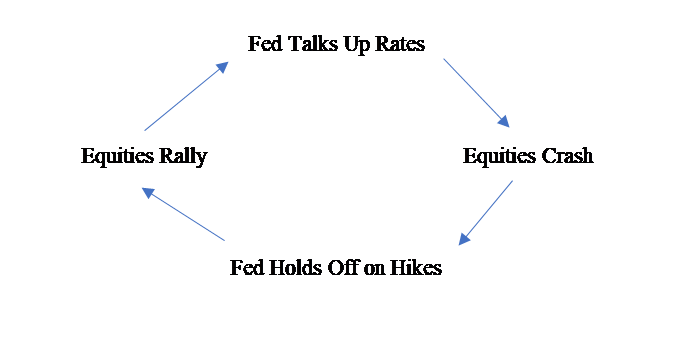

We have included the following graphic a few times over the last few years and it feels appropriate again now. This sums up the monetary policy cycle of the last decade pretty well.

Monday’s crash alone isn’t enough to cause the Fed to pause, but too many more sessions like that could. More likely, a correction of, say, 15% could result in the kind of grind lower that would force the Fed to reevaluate the projected pace of hikes. At a minimum, last week’s selloff reduces the probability of the Fed bumping up its projected number of hikes from three to four at the March meeting.

We don’t expect the Fed to hold off on rate hikes…yet. GDP and labor markets are strong and the tax stimulus has yet to work its way into the system. More likely, we envision this sort of vicious cycle later this year when some of the optimism has worn off. Or if inflation really struggles to climb.

But…the market has only recently begun buying what the Fed has been selling. The market did not expect three hikes last year even though the Fed kept reiterating its plan to do just that. This year, the 2 year Treasury has spiked to 10 year highs as the market finally threw in the towel and fell into line with Fed-speak about 3 hikes this year.

The market could quickly revert to its prior position of just two hikes or fewer this year if given an excuse. The two primary culprits for a change to market sentiment?

- Equity sell off

- Lack of inflation

A paradox of this type of cycle is that good news is bad news, and vice versa. Remember a few years ago when a really strong data point pushed rates lower because the market interpreted it as leading to a tightening cycle? If the recent market movements are attributed to the potential for a hawkish Fed, we may start seeing that same sort of response again.

If the Fed reduces the projected pace of hikes, we think it will more likely reduce the number of hikes in 2019 and beyond. For example, the Fed could stick to three hikes this year while promising no further hikes in 2019 and the market would probably take the news in stride.

Powell will do well to remember the late MIT economist Rudi Dornbusch’s remarks on economic cycles:

None of the post-war expansions died of old age. They were all murdered by the Fed.

Balance Sheet Normalization

We are four months into the Fed’s reverse QE program, reducing its balance sheet of Treasury and MBS holdings to allow for future purchases if needed.

The Fed’s balance sheet is now at its lowest level since August 2014.

The T10 is at its highest level since the spring of 2014.

Even Gronkowski could find a relationship there.

But there’s more…

Q4 2017 saw a reduction of $10B per month, with that amount stepping up each quarter this year towards an ultimate goal of $50B/month.

That schedule called for $20B/month in Q1 2018, with approximately $12B/mo attributed to Treasurys and $8B/mo attributed to MBS.

But in January, Treasury holdings actually dropped by $18B – a greater amount than expected.

So what about MBS? Through a quirk in the Open Market Operations where MBS is bought in a TBA (to be announced) format, actual declines aren’t fully known until as much as two or three months later.

This means we are just now getting a full understanding of December’s unwinds, which show a reduction of $9.5B.

Let’s pause for a moment to think about this.

- The Fed was projecting a reduction of Treasurys in January of $12B, but it actually dropped by $18B.

- We don’t have January data for MBS, but the December numbers that just rolled in suggested a reduction of $9.5B vs a projected $4B.

- The $9.5B already exceeds the level that the reduction was supposed to step up to in January.

The balance sheet normalization is actually occurring faster than announced and the government is set to issue massive amounts of new debt to help pay the current bills as well as to compensate for the immediate shortfall in receipts from the tax cuts.

Moody’s sent a warning shot across the bow on Friday, indicating “the stable credit profile of the United States (Aaa stable) is likely to face downward pressure in the long-term, due to meaningful fiscal deterioration amid increasing levels of national debt and a widening federal budget deficit.” That doesn’t sound like a downgrade is expected, but it does sound like Moody’s might be preparing to put the US on “negative” watch (lowered from “stable”).

Purely speculating, but we believe the Fed would prefer the 10yr Treasury north of 3% but below 4%. This would be a sufficiently steep yield curve to absorb up to six hikes over the next 24 months.

Asset Price Correction

Another reason for markets to take Monday’s crash seriously is that the last two recessions have involved asset price correction.

A large asset price correction could dampen the flow of funds from savers to investors, thus creating a drag on investment…and then growth.

Massive liquidity has distorted equilibrium prices and artificially depressed volatility. In a distorted market like this, pricing feels more random (bitcoin could be a microcosm of this). Markets get away with it during periods of low volatility, but we have new factors that could be upsetting recent experiences. Things such as:

- Fed tightening cycle

- Reverse QE

- Eagles Super Bowl win

- Higher long term rates

For the last several years, asset pricing could still rely on low interest rates and low volatility. But change some of these assumptions, and the market oscillates in search of equilibrium.

Then toss in the possibility for something like higher inflation, and the models start puking.

While we do not believe Monday’s flash crash was a recessionary signal, it should not be ignored, either. It could suggest something bigger happening across the asset spectrum.

Central Bank Dilemma – The Philly Special

What a bind Jay Powell may find himself in early in his tenure. Stick to the forward guidance even in the face of increasing market temper tantrums? Back off three hikes and appear bound to market sentiment? Even then, backing off could actually have the opposite effect if the market believes it will put the Fed further behind the curve.

This transition is likely to be painful – it’s really a matter of how much the Fed can limit the damage. Considering how last week’s correction seemed to come out of nowhere, there is a very real possibility of a bigger correction now that everyone is awake to the possibility.

Will Powell have the…wherewithal…to dial up his own Philly Special? Hike Hike Pause…slight of hand see you in the Operation Twist endzone?

Treasury Yields

In the near term, we still believe 3.00% on the T10 is a very real possibility, but after such a sharp movement higher it’s not uncommon for the market to settle down a bit. In other words, the T10 may keep climbing but not by leaps and bounds.

The German bund has plenty of room left to climb, with 1.00% on the near term horizon and 1.50% a very real possibility by year end.

If the spread between the 10T and bund remains constant during a bund spike, this would imply a T10 that could be testing 3.25%.

The possibility of an inverted yield curve is still more likely to come later in the year. The most likely scenario is that the Fed hikes twice while the yield curve is at current steepness levels, and then the T10 doesn’t need to fall as much later in the year if there’s a downturn.

This Week

Wednesday brings CPI and retail sales data. An outlier report from either could provide insight into how fragile market sentiment is right now.

Maybe Game of Thrones should just pan to Doug Pederson sitting on the Iron Throne and then fade to black…AND GREEN!!!!!!!!!!!