I have such a crush on Texas. My last trip pre-covid was Texas, and last week I circled back with my first true post-covid roadshow. Unfortunately, lending markets were just as murky as they were two years ago. Some quick takeaways from my discussions:

- Pricing is a guessing game…if you can get a quote at all

- Some lenders are pencils down right now

- Valuations are off 5%-10%

- Sellers are coming to grips with the drop in valuations faster than usual

- They are probably still getting a great return, just not as mind-blowing as it would have been 6 months ago, so they are taking what they can get

- I personally believe the abruptness of the change in markets helps with this realization

- Volatility is the primary culprit, not a belief that the underlying economy has deteriorated

I think lenders are just spooked right now. Six months ago, the Fed wasn’t hiking at all this year, SOFR was 0%, and the 10T was 1.50%. Two weeks ago, the Fed suggested it might hike 3% this year and the T10 was 3.13%. How do you underwrite a deal in that environment?

If and when volatility settles down, debt markets will follow.

Last Week This Morning

- 10 Year Treasury down to 2.78%

- German bund remained the same at 0.95%

- 2 Year Treasury slightly up to 2.58%

- LIBOR at 0.97%

- SOFR at 0.79%

- Term SOFR at 0.92%

- Retail sales came in at 0.9% vs 1.0% expected

- Retail sales excluding vehicles came in at 0.6% vs 0.4% expected

- Existing homes sales came in at 5.61 million vs 5.64 million expected

- Chairman Powell is determined to rein in inflation and aiming for a “softish landing”

- Acknowledged that the Fed should’ve raised interest rates sooner and less confident in achieving a soft landing

- Allocation to tech stocks is the lowest since 2006

- Bama vs Texas A&M just got a lot more interesting

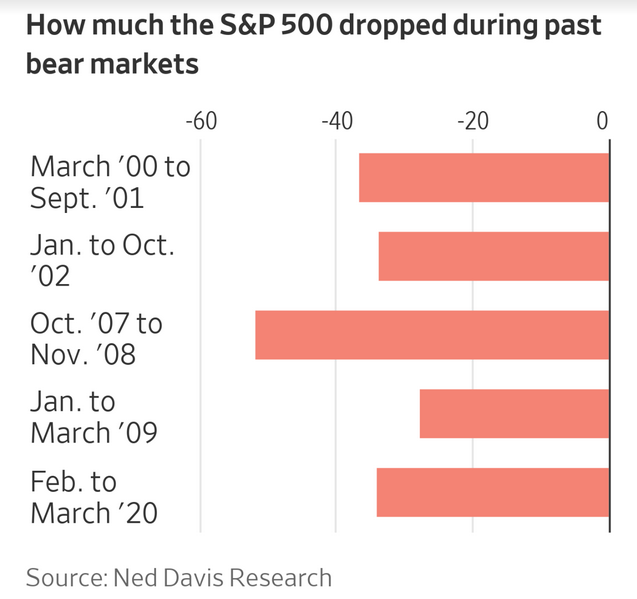

Is the Bottom Falling Out?

Stocks are flirting with official bear territory, which is generally a 20% correction. Unfortunately, that’s usually just the threshold and the drop is far worse.

The biggest reason for the selloff? The Fed.

Oil and gas up dramatically doesn’t help.

Source: Bloomberg Finance, LP

Source: Bloomberg Finance, LP

Meanwhile, small business optimism is plunging.

Source: Bloomberg Finance, LP

Source: Bloomberg Finance, LP

Europe is in or about to be in a recession.

China is cutting rates to fend off its slowest growth in over 40 years.

Good times!

But here’s the real reason the market is in such panic…I included this concept last week, but it’s probably the most important thing to keep in mind as we plow ahead this year.

When the economy turns south…when the markets tank…when unemployment spikes…the Fed bails us out with accommodation.

But now they are actively tightening as we move into restrictive territory.

Source: Bloomberg Finance, LP

Source: Bloomberg Finance, LP

And they have no choice as long as inflation remains elevated. Inflation, fueled by ongoing supply chain issues, China’s zero covid policy shutdowns, and Russia’s invasion of Ukraine, has been remarkably resilient. The Fed has to break its back.

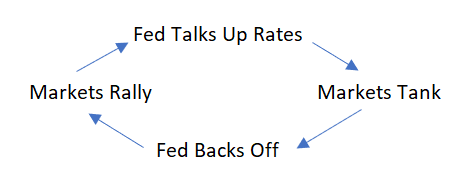

Normally, a cycle looks like this:

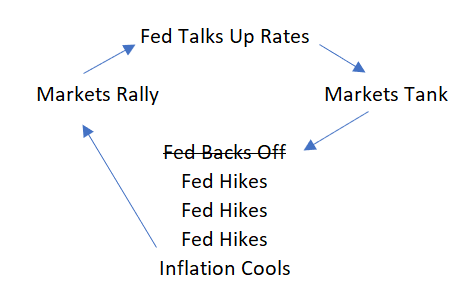

But with inflation, it looks like this:

The more hikes it takes to drive inflation lower, the more likely we are to find ourselves in a recession. Or, the deeper the recession.

How the next two years go will be largely dependent on how inflation behaves over the next 3-6 months.

In a more normal cycle, there would already be chatter about the Fed backing off the hikes. But it can’t right now because of inflation.

I think the next two meetings are nearly 100% likely to be 50bps hikes because the Fed has a meeting June 15th and July 27th. The July Core PCE will come out July 29th, two days after the Fed meeting. That means they only have this Friday and the June 30th Core PCE report to go off of over the next two meetings.

Despite markets tanking, Powell won’t change course until he sees a reassuring trend lower of inflation. “What we need to see is inflation coming down in a clear and convincing way, and we’re going to keep pushing until we see that,” Powell said in an interview last week.

Plus, we are starting from a position of strength, with the economy doing very well (much better than markets). With unemployment near all time lows, a huge amount of job openings, and far more cushion in the bank than most previous cycles, Powell will stay the course with at least two more 50bps hikes.

SOFR will be at 2.00% by August 1.

I think the economy can handle that. The seizure right now is in markets, not the economy. There’s a difference.

But after that, I think Powell is desperately hoping inflation has established a nice trend lower because the economy probably can’t handle 3.0%. And certainly not for any period of time.

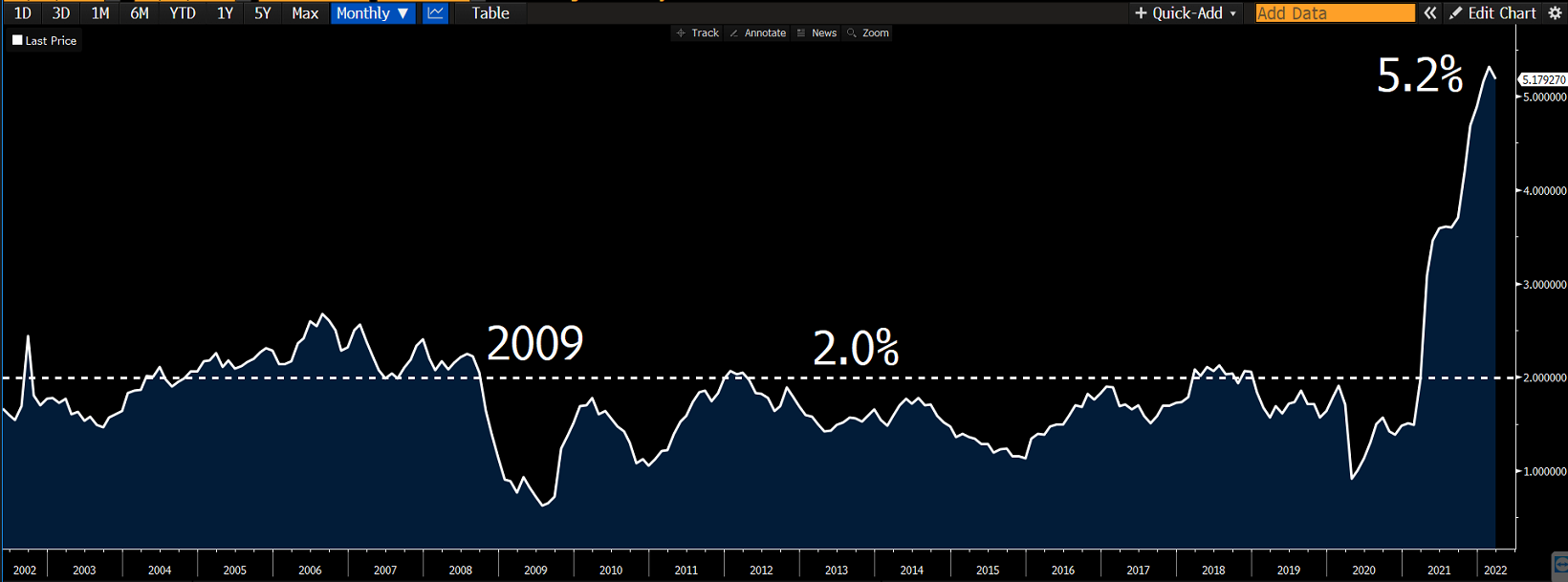

Here’s Core PCE, the Fed’s preferred measure of inflation. Do you see that tiny dip at the last reading? That was the first drop in 15 months. Will that trend continue?

Source: Bloomberg Finance, LP

Source: Bloomberg Finance, LP

Friday’s Core PCE is forecasted to come down to 4.9% (down from 5.2% last month). Simplistically, here’s the likely market reaction depending on how it shakes out:

- As expected: the market exhales, just glad that the trend lower is continuing (albeit slowly). T10 could move a little higher, but likely range-bound.

- Lower than expected: market asks, “So you’re saying there’s a chance?” Powell Top Gun high fives Brainard, T10 tests 3.0%.

- Higher than expected: market assumes the Fed will have to hike us into a recession, T10 falls. Powell calls Biden and asks how a hypothetical recession would impact mid-terms.

Markets are hoping inflation begins its downward trend soon.

Powell is hoping the all the saber-rattling hawkish rhetoric will actually work.

I’m hoping inflation drops because just 18 months ago I said it didn’t exist anymore.

But like my mentor used to say, “Hope is a terrible hedge.”

Thursday and Friday should be interesting.

Week Ahead

Wednesday brings FOMC Minutes, so we get a glimpse into the chatter amongst Fed officials.

But really, all eyes are on Thursday and Friday’s inflation data.