Last Week This Morning

- 10 Year Treasury spiked to 2.47%

o German bund spiked to 0.59%

- 2 Year Treasury up to 2.27%

- LIBOR at 0.45%

- SOFR at 0.27%

- Term SOFR at 0.30%

- Durable Goods sales were down 2.2%, quite a miss

- New home sales were lower than expected

- Citi now expects the Fed to hike 11 times before year end, putting Fed Funds at 2.75%

- UNC vs The World…now I know what it’s like to be a Duke fan

Slamming on the Brakes

Citi economists singlehandedly crushed rates on Friday by calling for 11 hikes by year end. This would put Fed Funds at 2.75% before 2023, a full 0.75% higher than the Fed is suggesting. Bank of America chimed in, revising its forecast up to 3.25% by May 2023.

We described tapering as taking the foot off the gas pedal, while rate hikes are applying the brakes. The Fed’s dramatic shift in such short order is the equivalent of slamming on the brakes.

With Fed speakers every day last week, one message was clear: the only reason the Fed didn’t hike more was because of the Russian invasion of Ukraine. Barring an escalation in Ukraine, the Fed is likely hiking 50bps at the May 4th meeting. This opens up a can of messaging worms. Once you hike 50bps, is 75bps on the table? Is 50bps the new pace?

The Fed is trying to rein in inflation expectations. Here are 1 year forward expectations. After a brief dip to start the new year, Russia invaded and concerns surged again. This shocking pivot by the Fed is intended to pull these expectations down sharply.  Source: Bloomberg Finance, LP

Source: Bloomberg Finance, LP

What if it works?

With all these Fed efforts to rein in inflation expectations, is there a point later this year they are willing to ease off the brakes?

I’ve said for years that the Fed would love to have an inflation problem. Now that they do (or believe they do), can they achieve a soft landing? Doubtful. Here are a few of the ways this plays out.

- A 3.00% Fed Funds actually is the neutral rate – the Fed hikes to 3.0% and stays at the 3.0%, the economy absorbs it well, unemployment doesn’t climb, GDP remains strong (albeit lower than current levels), and everyone is happy. Mission accomplished. The last time Fed Funds was at 3.00% was pre-financial crisis.

- Hike less than currently projected – in this scenario, the Fed adapts while hiking. Let’s say Fed Funds is 2.00% at year end, inflation is dropping consistently each month, expectations are reined in…does the Fed audible and say, “we’re good for now, we want to see how the actions of 2022 play out in 2023”? This is my scenario where a lot of the current Fed-speak is really saber rattling intended to spook markets, but the Fed secretly plans on hiking less.

- Hike aggressively, then cut a little bit – this has shades of 1994 when the Fed hiked 3.00% before quickly backing out 0.75%. This helped extend the economic expansion for a few years.

- Over hike and tip us into recession – this is what the market is pricing in and is pretty much what happens every time the Fed raises rates. The market has a recession in 2024 as the forward curve dips. Parts of the curve are already inverted, with 5yr and 7yr rates above 10yr rates.

Rising rates will clearly impact interest rate sensitive sectors. Housing is the first that comes to mind. Cars. Our industry.

But will people buy less food? Less clothing? Travel?

In March 2020, everyone stopped buying stuff, doing stuff, and making stuff – simultaneously. The Demand Spigot and the Supply Spigot were turned full off at the same time.

With the help of the government, the Demand Spigot got turned back on. Unfortunately, this came at the same time the government was keeping the Supply Spigot cut off through forced lockdowns and restrictions. Demand returned much faster than the supply could. This caused a supply/demand mismatch, and prices have been surging ever since.

We are looking for rate hikes to solve inflation because that’s how we normally do it, but I’m not sure it will work that way this time.

I think there’s a chance we keep pulling on the rates lever, frustrated it’s not having the intended reaction. In this scenario, each hike fails to curb inflation as expected, so the Fed keeps pulling the lever. Because there’s a lag between rate hikes and spot inflation, we end up hiking too much and tip into a recession. The fact that the Fed thinks it can hike rates without impacting unemployment is Exhibit A for why the market expects a recession.

Rising rates most directly impact credit and curb demand for loans, but is credit demand out of control?

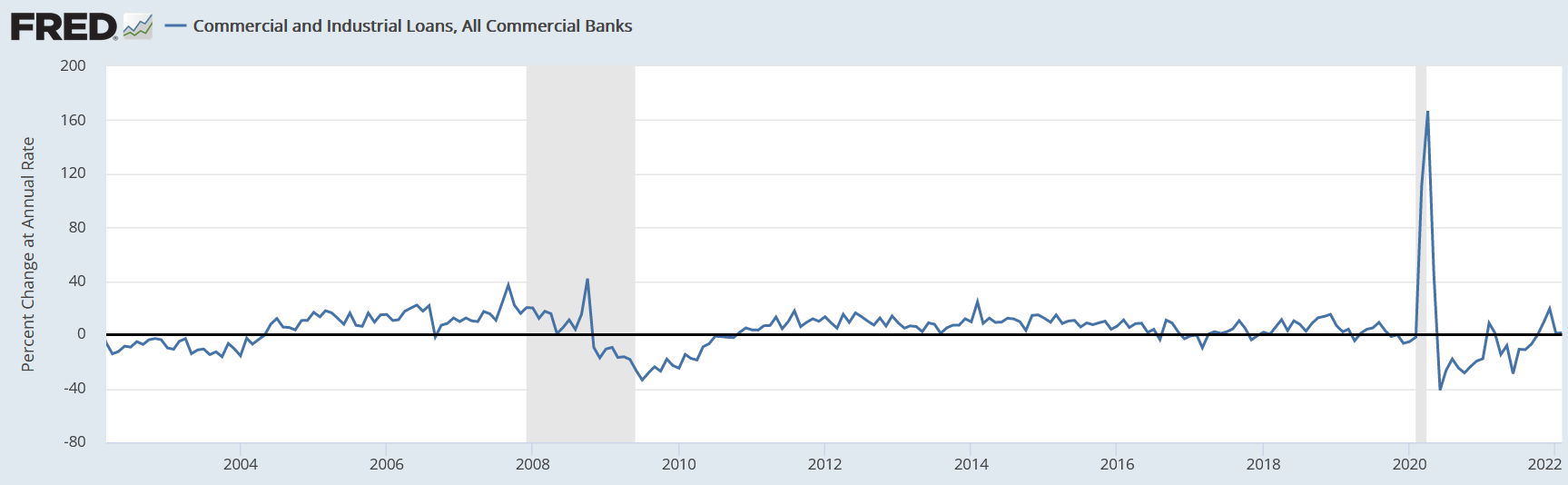

Here’s loan growth across all commercial and industrial loans over the last 20 years. Ignoring the surge when covid hit, borrowings don’t appear to be spiraling out of control. They lag the growth rates we saw leading into the financial crisis. Will rising rates dramatically dampen demand for loans that appears normal in the first place?

Impact on commercial and multi? You understand the impact of rising rates on our industry better than me, but I will actually be watching two things more closely than short term floating rates to determine if there’s a correction on the horizon:

- Lending appetite

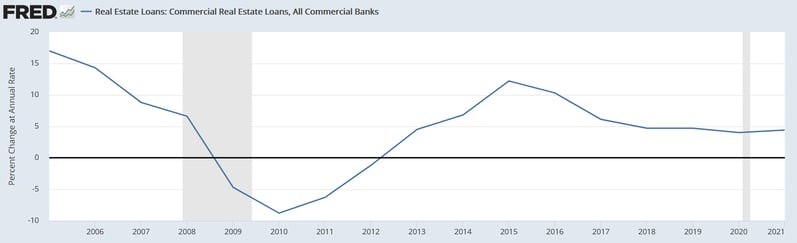

a. While lenders are temporarily pulling, particularly involving securitized debt, I think this is out of an abundance of caution rather than the first stage of credit tightening. Lenders have been very disciplined relative to 2005. Look at how flat lending growth in commercial real estate has been over the last few years. This graph starts in 2005 when CRE lending growth was almost 20%. Nothing about the current environment screams “bubble” the way it did in fifteen years ago.

- Liquidity

a. Everyone is worried about how rising rates will impact cap rates, but I’m not sure they can gap materially wider as long as the industry is awash in cash. Quantitative tightening, aka balance sheet reduction, may have a bigger impact on cap rates than rising floating rates.

Speaking of which…

It’s the Liquidity, Stupid

Rising rates will dampen demand on big ticket purchases like houses, cars, and other interest rate sensitive sectors. Stocks will probably reprice. It will also help with the psychology of an overheated economy, which in turn should help with the supply chain issues.

But I also think there’s a chance that monetary policy won’t cure all inflationary ills. Actually, I don’t think a 3.0% hike in interest rates is actually the equivalent of slamming on the brakes.

Instead, I think the lack of response to a 3.0% hike in interest rates could lead to mistakes in other areas of policy, most namely Quantitative Tightening…which impacts…

Liquidity.

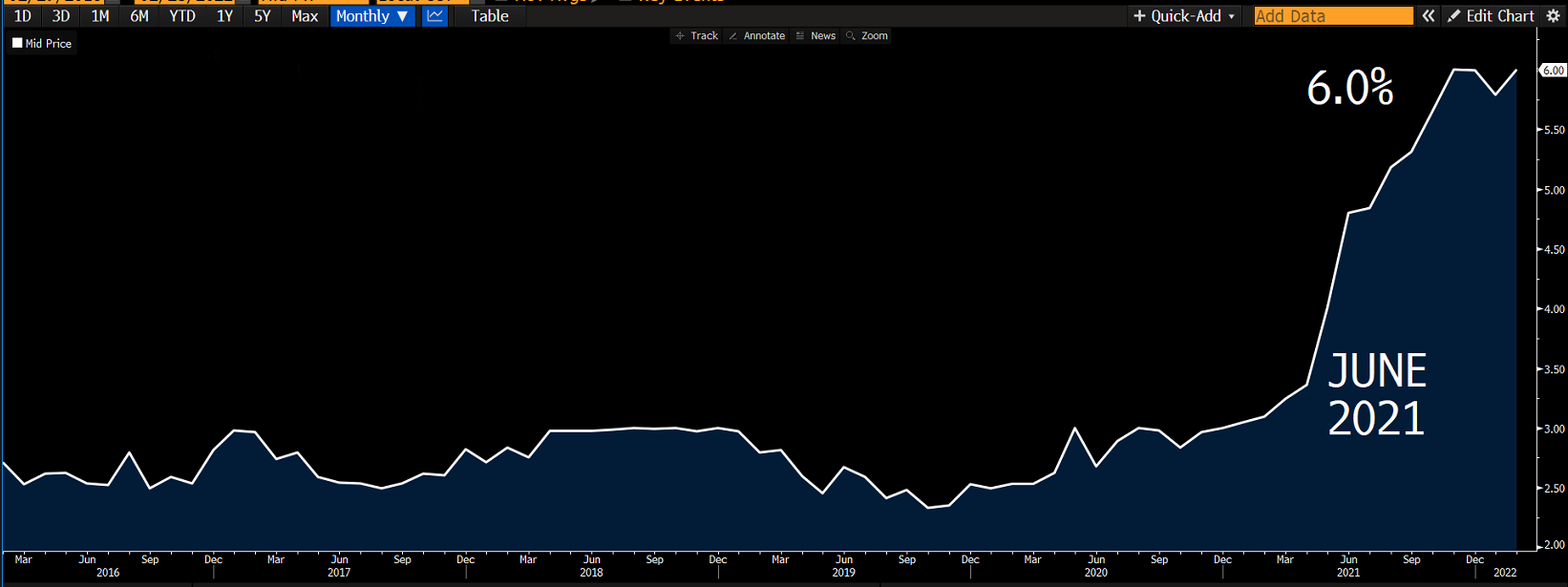

Here’s the Fed’s reverse repo outstanding balance. It serves as a proxy for excess cash in the system. Look at when it spiked – June of 2021. Remember that 1 year forward inflation graph from earlier? Inflation expectations started surging in June 2021. Probably just a coincidence, right? We actually wrote about it on June 1 (https://www.pensford.com/industry-news/whats-all-this-reverse-repo-stuff-about).  Source: Bloomberg Finance, LP

Source: Bloomberg Finance, LP

At the time I wrote that, RRP had spiked from $0 to $500B in a week. Shortly thereafter, it climbed to nearly $2T.

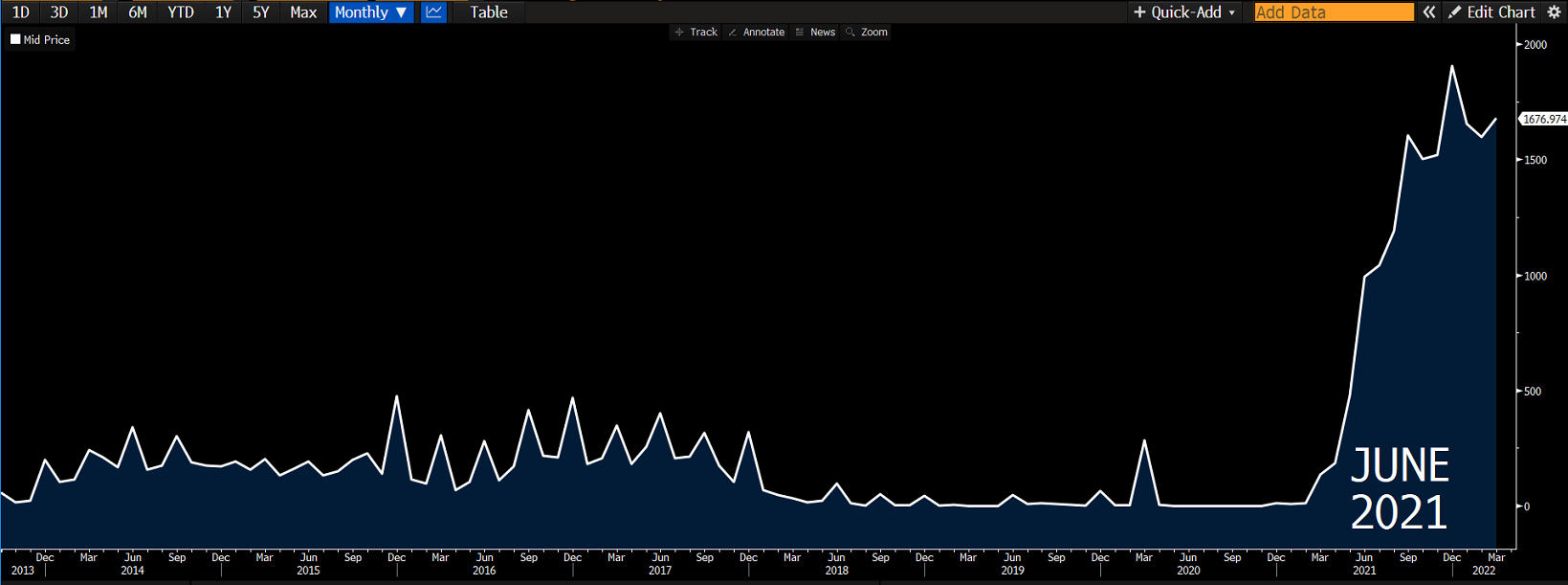

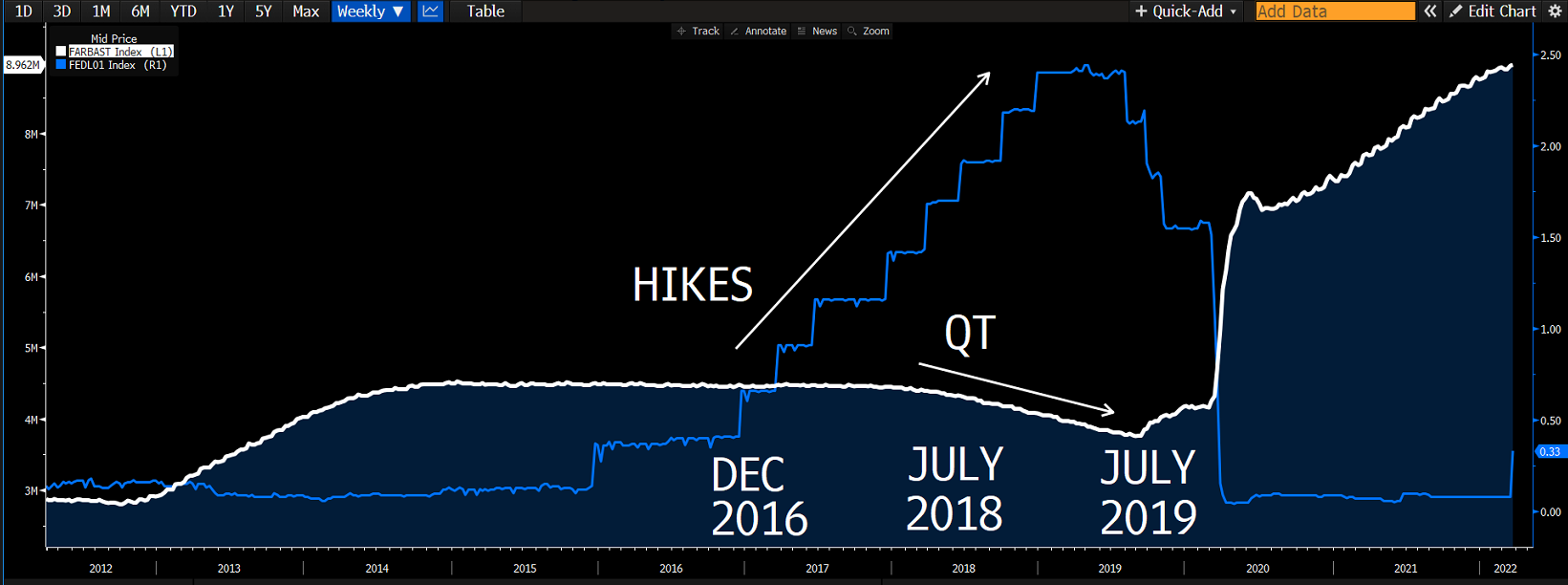

The Fed hopes Quantitative Tightening will help drain excess cash from the system. Sounds admirable, but the last time the Fed was hiking rates and shrinking the balance sheet at the same time, markets seized up quickly. The Fed managed to reduce the balance sheet by just $600B before it had to throw in the towel.  Source: Bloomberg Finance, LP

Source: Bloomberg Finance, LP

Powell said at the last meeting the pace would be much faster this time around. Does that mean the Fed will be throwing in the towel faster?

0% interest rates aren’t to blame for the current pricing surge, nor will they fix it. It’s a demand/supply mismatch, exacerbated by excess liquidity.

Time will be the biggest factor in supply chain resolution. Quantitative Tightening will be the biggest factor in removing excess liquidity.

For day to day impact, yes, rising floating rates will be a hot topic. Interest expense, cap costs, borrowing spread, etc.

But from a macro perspective, I think the real estate industry should be more focused on the drainage of liquidity. Like winning, liquidity covers up a lot of flaws. Take that away, and we become far more sensitive to things like rising interest rates.

This, not rising Fed Funds, could be the primary catalyst for meaningful pain in our industry in the coming years.

Week Ahead

We get the Fed’s preferred measure of inflation this week (Core PCE), which will likely confirm the Fed’s intent to hike 50bps at the next meeting. Forecasts for Core PCE suggest a 5.5% print.

We also get the next batch of jobs data, with consensus forecasts for gains of 490k jobs and a 3.7% unemployment rate.

Most importantly, Carolina vs Duke in a Final Four matchup for the ages (and yes, I am writing this before Carolina has played St Peter’s…)