I get my hair cut at Great Clips every few weeks. I don’t have enough hair to justify spending more than $15. I tried to swing by on Wednesday and they were closed. Every other Great Clips within 10 miles had an hour long wait. So I bailed.

Thursday, I decided to check online before heading over. Maybe they had closed permanently. Nope, they were open. But the wait was an hour. I checked in online and timed my arrival for the one-hour mark.

Once I got in the chair, I asked why they were so busy. I assumed school ending, graduation ceremonies, etc. The woman cutting my hair said, “No one will come to work because they are making more sitting at home.”

Enhanced unemployment was encouraging workers to stay at home. Great Clips couldn’t get stylists to come to work, and there were rolling store shut-downs where each one took a turn. Plus, stores were allocating just two stylists per day. That led to a huge back up and one hour wait times.

The moral hazard of enhanced unemployment is playing itself out. It will be interesting to see how the 23-GOP-led states that reduce enhanced unemployment will fare against the rest of the nation. For at least for the Great Clips around our house, lower wage employees are choosing to make more off the government than returning to work.

Last Week This Morning

- 10 Year Treasury down a couple of bps to 1.59%

- German bund down a few bps to -0.18%

- 2 Year Treasury down 1bp to 0.14%

- LIBOR at 0.085%

- SOFR at 0.01%

- Biden releasing a $6T fiscal budget proposal for infrastructure in 2022 tomorrow (the largest level of federal spending for the US since WWII)

- Core PCE came in at 3.1%, the highest reading since 1992

- This was higher than the forecasted 2.9%

- For comparison, March was 1.6%

- Before you scream “The Inflation Sky is Falling!”, keep in mind it is measuring against the first month of last year’s shutdown. This is like Jim Harbaugh’s taking his 2015 record (10-3) and comparing it to Brady Hoke’s 2014 record (5-7) and demanding a contract extension…oh wait, he did…

- Personal income plunged 13.1% (the largest drop ever), someone turn that stimmy machine back on!

Front End Rates are Trying to Go Negative

Let me begin with a disclaimer – I am not a repo expert. The only thing I know less about than repo is reverse repo. You can fill two internets with what I don’t know about the repo market. With that being said…

What’s the deal with reverse repo all of a sudden?

Repo Backdrop

The repo market is a short-term funding market where someone with cash loans it to someone with collateral (usually Treasurys) for a short period of time, frequently overnight.

Let’s say you’re a corporate Treasurer and you just received your gigantic tax bill. Or you’re preparing the balance sheet snapshot for quarter end. Or you need to pay for a massive investment in Texas so you can move out of your socialist less-business-friendly state. You check the corporate coffers and like one of my kids two weeks into their college semester, most of the money is already gone.

Being the good Treasurer, you have a diversified portfolio of holdings, including a big chunk of Treasurys. You could sell the Treasurys, but that triggers tax implications. And if you’re a financial institution, it could have regulatory impacts.

So you ask around to see if anyone will lend you some cash for a few days. In exchange, you’ll pay a very low interest rate (since it’s basically risk free) and you’ll temporarily assign the Treasurys to them as collateral. Once you pay them back, they return the Treasurys. It’s a win-win.

SOFR is a repo rate. You may recall it misbehaved in September 2019 when it spiked north of 5.0% (and even had some intraday readings north of 10%). There was a shortage of cash, and so holders of Treasurys had to offer increasingly higher interest rates to entice someone to lend it to them. This dislocation led to massive Fed Reserve intervention, leading me to ask, “Is it really any better to transition from one manipulated index (LIBOR) to another (SOFR)?” Instead of 20 banks doing the manipulating, now it is just one – the Fed.

The Fed was right to intervene aggressively in 2019. Liquidity evaporated and parts of the financial system were at risk.

This time around, the problem is the exact opposite – there is too much cash coupled with too few Treasurys.

Problem #1 – Too Much Cash

When the Fed buys Treasurys, it is putting $120B cash each month onto balance sheets (mostly of money market funds and banks). Federal stimulus compounds this, such as the money recently deployed to state and local municipalities.

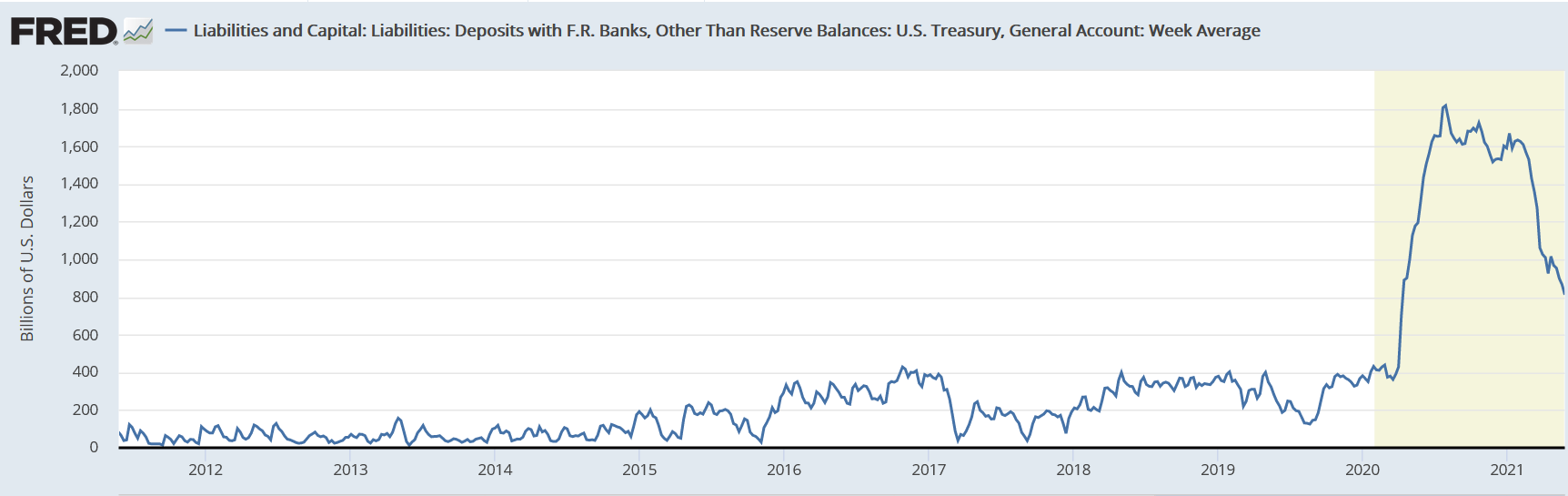

Check out the graph below of the Treasury General Account. This is the federal government’s bank account. Notice how the balance has plunged recently. That cash is being transferred from the government to other entities (GSE’s, banks, state/local munis) and frequently end up in a bank account or money market fund. Those, in turn, need to do something with it.

Problem #2 – Too Few Treasurys

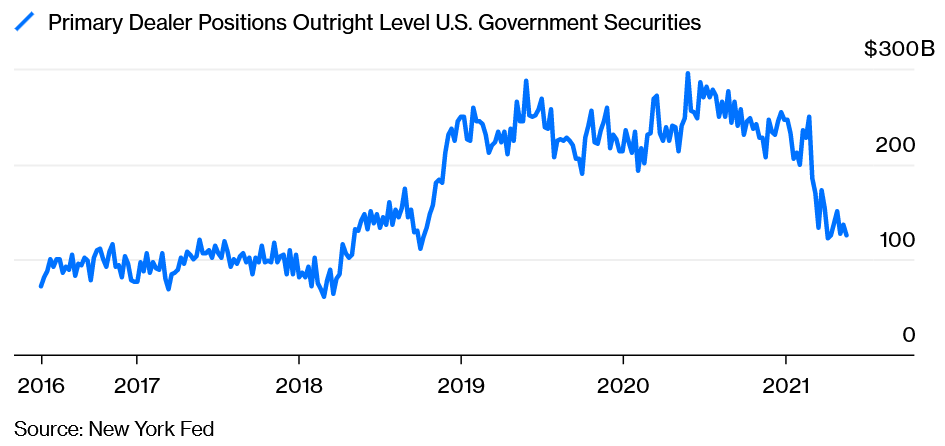

When the Fed buys Treasurys, it is taking that potential collateral out of circulation. Look how Treasury holdings by primary dealers have plunged.

This shortage will be exacerbated by the reinstatement of the federal government’s debt ceiling on August 1, which will translate into even less supply.

Too much cash is chasing too little collateral, and front-end rates think about going negative. We addressed this in early March. Four week t-bills have been yielding 0% for the last two months, and eight week t-bills are 0.005%.

If it sounds crazy to think about negative interest rates, just remember that much of the world is already grappling with that problem. It’s the return of principal rather than the return on principal.

The Fed knew QE would flood the market with cash and came up with the RRP to deal with that.

Reverse Repo Program (RRP)

The Reverse Repo Program (RRP) was actually created before the most recent round of QE, but it was largely ignored the last few years. It allows money market funds and banks to lend cash to the Fed in exchange for collateral, Treasurys. It was basically a relief valve for banks with bloated balance sheets. Sticking money under the Fed mattress. Even though the reverse repo rate is 0%, it’s better than the general overnight repo rate of -0.01%.

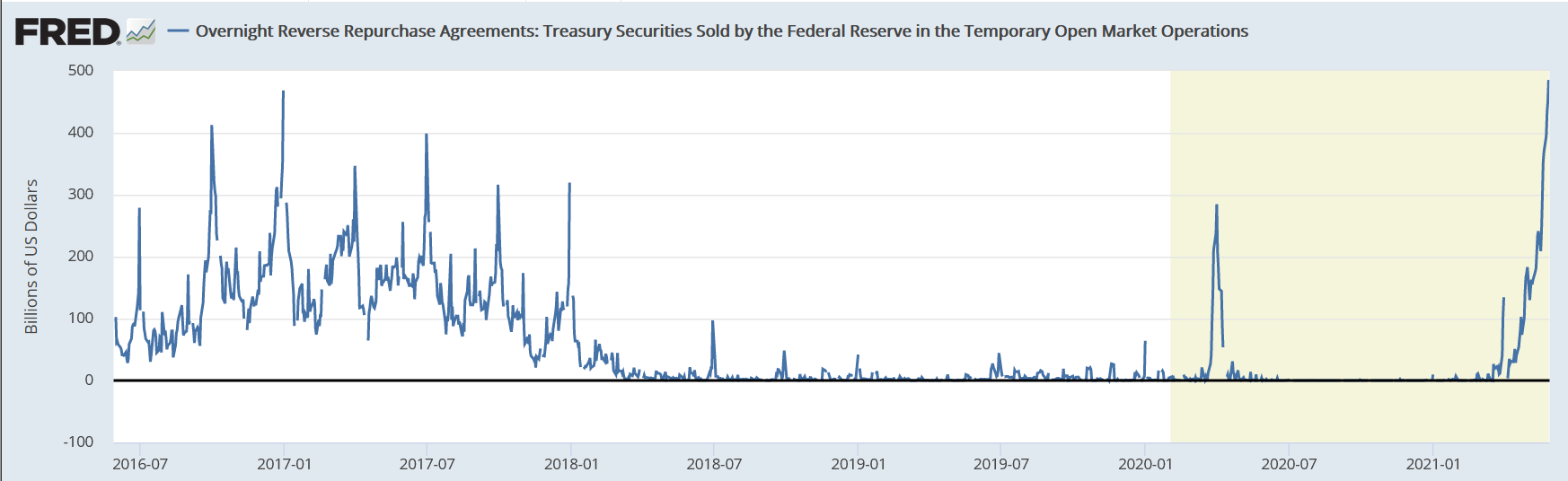

Here’s what the recent volume looks like.

In mid-March, do you know what the total amount outstanding in the Reverse Repo Program was? Zero. Last week, the RRP daily volume had grown to a record high of nearly $500B. What happened in March?

The SLR Expiration on March 31st

The Supplemental Leverage Ratio (SLR) ratio is meant to require banks hold a certain amount of capital relative to assets. Because QE increases assets for banks, this means the ratio gets distorted. The Fed knew this and created an exemption to the SLR test as a result of QE measures. “We know we are forcing your balance sheets to bloat, so we won’t force you to hit this SLR hurdle for now.” We had written about it in terms of potentially causing higher yields because banks would be forced to sell Treasurys in order to hit the SLR target. That exemption expired on March 31st.

As the exemption expiration loomed, Jamie Dimon suggested JPM might have to turn away deposits because they would only exacerbate the ratio dilemma. And if banks are turning away deposits, where’s the next logical place to park them? Money market funds, which are the primary user of repo markets. Too much cash.

So Now What?

This isn’t occurring at quarter or year end, which means you can’t simply explain it away as transitory. Heck, I’m not even sure the Fed considers this to be a legitimate problem. I would agree it’s a smaller threat than the September 2019 turmoil. Too much cash is better than not enough cash. The Fed’s main concern might be one of optics – it doesn’t want to give the appearance that it has lost control of interest rates. Powell doesn’t want rates to drop into negative territory unless he is the one that makes it happen.

What could the Fed do if it decides this actually might be a problem?

- Increase the Interest On Excess Reserves (IOER) to encourage banks to park their cash in that account. It currently pays 0.10%. Increasing that could incentivize banks to stop searching out repo, as well as prevent rates from going negative.

- Or send a signal about tapering. If QE is the cause of this, ease off it. They could taper front end purchases or target certain longer durations. This comes with its own sort of problems, including losing credibility after constantly telling us they won’t taper until 2022, as well as potentially creating market turmoil in the nascent stages of the recovery.

- Actively sell front end holdings. We talked just last week about how the Fed was far more concentrated on the front end of the curve. If the Fed starts actively selling, it could cause rates to spike and entice Treasurers to put their money into those instruments.

- Re-institute the exemption for the SLR. Even though this feels like such an obvious cause and effect given the timing, re-instituting this exemption mostly benefits a few of the biggest banks and doesn’t necessarily benefit the broader market enough to ease pressure.

- Increase the daily counterparty limit. This was increased in March from $30B to $80B because the Fed recognized the impact the SLR exemption would have. It could increase this further.

Bottom Line

The Fed has tools at its disposal to deal with this, even though they might not view this as a pressing issue. I don’t see a lot of near-term impact on our clients, but the likely risks include Fed credibility. The Fed does not want negative interest rates unless they say so.

How does the Fed withdraw enough support to ease the strains on the financial system without upsetting the apple cart and tightening conditions too soon?

I don’t have a clue. But that’s why Jay Money Powell gets paid the big bucks and I write a newsletter from my laptop in a Richmond hotel before my sons’ tournament.

Random Thought of the Day

The Treasury Department issues Treasurys each month.

Primary dealers are obligated to buy a minimum amount of those Treasurys each month.

The Federal Reserve, through QE, buys those Treasurys.

The Federal Reserve, through RRP, offers those Treasurys up as collateral back to those same banks.

Got it. I think.

Thank goodness far smarter people are in charge of these things.

Week Ahead – Jobs Report

Friday brings the next labor report, which takes on increased significance following last month’s huge miss (266k vs 1mm expected).

Consensus this month is for 660k jobs gained. I wouldn’t be surprised to see a higher number, partially making up for last month’s miss.

There remains quite a bit of slack in the labor market, and not just from paying people more money to sit at home. According to a paper by Alexander Bick and Adam Blandin, 37% of all employees are no longer with the same firm they were with in February 2020. That is a staggering statistic. After the initial snapback from re-opening passes, the rest of the recovery will feel more like a traditional recovery.