If stuffing is the best part of Thanksgiving, seeing family is a distant fifth. Unlike all previous Thanksgivings, this iteration had the odd backdrop of World Cup soccer. I’ve watched far more than I expected because there’s really nothing else on when I get up at 3:30am. Plus, I do love the continuous clock. That being said, the flopping is killing me.

I watched my three nephews, all under 10, beat the living snot out of each other for hours on end. This was real punching and kicking and they just kept going back for more. I was struck by how much tougher they are then the grown men playing soccer on TV. If my 4 year old nephew slammed a striker the way he slammed his older brother, the striker would be taken off on a stretcher and no amount of magic spray could save him. The dramatic confusion around which limb to grab when an opponent breathes is a non-starter for me.

America’s best soccer players all play other sports, so we will never be dominant. But I wish our team had a couple of NFL linebackers that ran around and politely introduced the world to what actual physical contact looks like.

Last Week This Morning

- 10 Year Treasury down to 3.68%

- German down 5bps to 1.97%

- 2 Year Treasury down 10bps to 4.45%

- LIBOR at 4.05%

- SOFR at 3.79%

- Term SOFR at 4.08%

- S&P US manufacturing PMI came in at 47.6 vs expected 50.0

- This is the lowest reading since May 2020

- S&P US services PMI came in at 46.1 vs expected 48.0

LA Ports

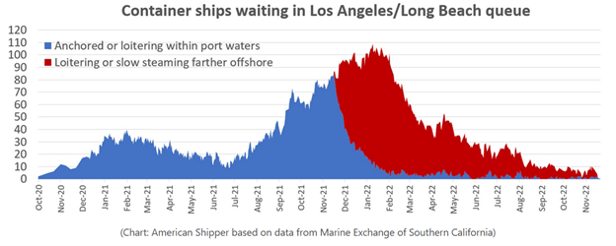

Remember when we all became experts in LA ports (as opposed to the time when we all became experts on pandemics, inflation, college sports, protests, etc)?

At the peak, there were more than 100 container ships waiting off the coast of southern California. Last week, this number dropped to zero. This includes those ships that were even farther off the coast than usual.

Some portion of the inflation problem has been supply chain related, and those issues were never going to be primarily resolved through demand destruction. Supply chain issues needed time, and they have improved considerably.

American Shipper (Christmas magazine gift ideas anyone?) interviewed the CEO of Norwegian firm Xeneta, a company that tracks shipping rates. The topic was the plunge in shipping and whether it was related to the vacuum post-covid or a fall in demand.

CEO: “We run monthly polls with our customers, who have tens of billions of dollars of procurement spend. We asked them last week how they thought ocean volumes in 2023 would compare to 2022, and hardly anyone expected an increase in volume. Thirty-nine percent said they expected volumes to decrease by 10% or more. So, not only will carriers have to adjust to the current reductions in volume, they will face significant volume reductions in the coming quarters as well. That means it’s going to be hard for them to hit that equilibrium between supply and demand in 2023.”

American Shipper: “You’re saying that it’s not an import timing issue. It’s an economic weakness issue?”

CEO: “Yes, that’s what we’re saying.”

FOMC Minutes

The biggest headline in an otherwise quiet week was the FOMC Minutes, which were interpreted by the market as dovish. Maybe, just maybe, there is a light at the end of the tunnel.

That being said, it is premature to call this a pivot. The general message boiled down to two critical takeaways:

- The pace of hikes should slow, eg from 75bps to 50bps to 25bps

- The final landing spot might be higher than currently priced in

This doesn’t strike me as a reason for rates to plunge and stocks to rally, but here we are. I suspect the market (over)reaction is more of an exhale that the unabated run of 75bps hikes is at least coming to an end.

Another interesting takeaway is that the Fed might be separating into two camps.

Camp 1 – slow the pace of hikes, we are nearing the time to pause and evaluate the effects of massive tightening, forward looking data is slowing

Camp 1 Spokesperson – Vice Chair Lael Brainard

Camp 2 – slow the pace of hikes but keep hiking until inflation is materially lower, we can’t allow inflation to become entrenched, it is too soon to pause, the labor market is too hot, financial conditions are barely in restrictive territory

Camp 2 Spokesperson – Jay Money Powell

If you started skimming, you may have missed that…but the Chair and the Vice Chair appear to be in different camps. Awkward…

If the job market is Exhibit A for why Powell may not be ready to pivot yet, Exhibit B is Financial Conditions. After a charge towards recessionary territory in October, financial conditions are actually back at the breakeven point.

From Powell’s perspective, this could mean the brakes aren’t even being pressed that hard.

Source: Bloomberg Finance, LP

Source: Bloomberg Finance, LP

With this week’s Core PCE data and another CPI print before the December 14th FOMC meeting, there is a chance that Brainard’s camp gains traction heading into year end.

But in general, I think we are a few months out from a true Fed pivot.

Week Ahead

Core PCE (the Fed’s preferred measure of inflation)

GDP

Jobs report

Buckle up