I guess we’ll all be able to really enjoy some downtime this summer…

Last Week This Morning

-

10T: 4.59%

-

2T: 4.07%

-

SOFR: 3.56%

-

Term SOFR: 3.61%

-

Warsh confirmed as Fed Chair

-

CPI about as expected, but much higher than last month

-

PPI way hotter than expected, which was also much higher than last month

-

Fed-speak: remember when I said that Fed officials would start ratcheting up the tough talk even if they have no intention of hiking?

-

Collins: “While it is not in my most likely outlook, I could envision a scenario in which some policy tightening is needed to ensure that inflation returns durably to 2% in a timely manner.”

-

Kashkari: “We are dead serious about getting inflation back down.”

-

Make It Stop!

This is brutal. Do we all just take the summer off?

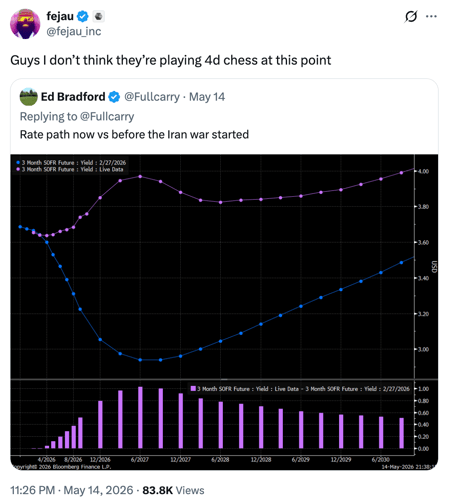

The odds of a single rate cut in the next 12 months are the same as FF hitting 5%. That is not a typo.

The market is pricing in the same probability that the Fed hikes 1.25% as that it cuts just once.

Rates across the curve are returning to levels we saw a few years ago at the peak of “higher for longer.”

Warsh took over and markets immediately puked. If he can’t at least acknowledge the possibility of hikes, rates could keep running up. Ironically, Warsh postured for Fed Chair based on returning credibility and yet the lack of independence from Trump’s wishes for lower rates is playing a role in rates jumping.

Even more ironic is the fact that Warsh actively opposes Fed officials sharing their thoughts on the path of rates. Warsh saying he will hike if necessary is exactly what the markets want to hear and yet he philosophically opposes it. And even if he conveniently makes an exception for himself, he risks running the ire of Trump.

What a time to be alive!

Japan 10yr hit the highest yield in 30 years. The last time it was this high, DJT was holding a press conference calling his Miss Universe “Miss Piggy” and “an eating machine.”

Don’t worry, it’s not like he made her jump rope in front of a room full of reporters…

The German Bund hit 3.16%, its highest level since 2011. Coincidentally, that was the year that Obama mocked Trump at the White House Correspondents’ Dinner. Trump may not have published a book that year, but a lot of observers believe that led to Trump’s focus on winning the White House.

The US sold 30yr Treasurys at 5% for the first time since 2007 when DJT was releasing “Trump 101: The Way to Success.”

Last week I wrote, “For what it’s worth, Trump has a tendency to change course when the T10 gets around 4.5%...now we wait to see how he handles Iran as the T10 threatens to run to 4.60%.”

The T10 finished the week at 4.59%. This would be a good time to do something Donny!

What Brings Rates Back Down?

This question has levels to it. Let’s first ask the uncomfortable question…

Can the T10 push to 5%?

-

Yep, but as much as I blame Trump for shooting himself in the foot, In Bessent I Trust. While he can’t enact QE, he has two other levers.

-

Bond issuance: shift issuance to heavily front-end weighted. Lack of new 10yr and 30yr bonds creates buying on the long end of the curve from the sovereigns and pension fund crowd that has a mandate.

-

Treasury Buyback Program: the Treasury can buy bonds in the secondary market. In order to do this, they will need to issue new Treasurys…see above.

-

Like Fed-speak, Bessent only first has to say he could do these things.

-

-

Markets are testing Warsh here…if he refuses to acknowledge the possibility of a hike then, rates could keep pushing higher.

-

The T10 climbed 25bps last week. Markets are in a bit of a panic trade here and it’s a global dislocation, so 5% is possible…but I don’t think it’s probable.

-

Each bps move higher makes US debt that much more appealing.

What gets the T10 back to 4.2% - 4.5%?

-

Warsh/FOMC convince the market they will hike if necessary.

-

Some sort of progress on the Iranian stalemate, likely brokered by China. Did you think Trump’s visit last week was actually about trade deals?

-

Oil needs to get back below $100/barrel and move towards $80.

-

Inflation expectations need to subside.

What gets the T10 back to 4.0% - 4.2%?

-

Concrete progress on Iran, likely an actual deal

-

Oil < $80

-

Weak jobs reports

-

Deteriorating economic data…markets are focused on inflationary pressures, but the global economy just got hit with a shock and US consumers just got hit with a tax.

The year Trump got into hot water for picking on Miss Universe, he also rolled out “The Art of the Comeback.” Perhaps the biggest takeaway was “Stay alive long enough for things to turn your way.”

Seems like an opportunity for the President to re-release that one as a new, special edition.

Unfortunately, another lesson from this book was “Confidence can substitute for discipline.”

The Week Ahead

Quiet week on the data front, not that that matters much right now.

Check out this cool new cap tool we are rolling out to customers: Cap Optimizer

Right now it basically just says, “Too bad, so sad” but once rates and vol settle down, it will be super cool!