I don’t want Iran to have nuclear weapons as much as anyone else, but I am old enough to remember the Cheney Doctrine justification. Philosophically, it makes sense. And it’s very hard to take a stance against it in the moment. No one ever says, “Terrorist nations are entitled to nuclear weapons!”

But I also don’t remember him cautioning, “This means we will be in Iraq for a decade and 4,500 American soldiers will make the ultimate sacrifice.”

The bar for that sacrifice should be incredibly high, particularly when those making the decision never served.

Thank you to those who made that ultimate sacrifice and to those they left behind.

Last Week This Morning

-

10T: 4.58%

-

2T: 4.14%

-

SOFR: 3.51%

-

Term SOFR: 3.61%

What Will Cause the Fed to Hike This Year?

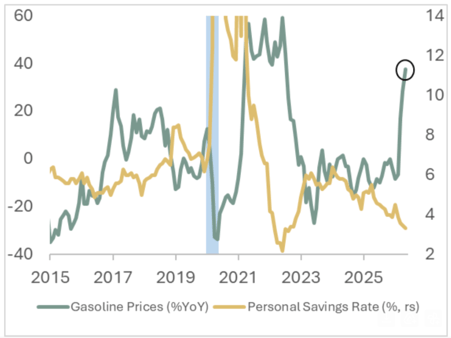

SMBC Chief Economist Joseph Lavorgna published a report on Tuesday, “Why the Fed May Have to Hike at Least 100 Basis Points.” A primary concern is that oil reserves are being depleted at rapid pace and oil could surge to $150/barrel. Without an imminent resolution in Iran, the worst pricing pressures are still ahead of us. As gas prices jump the most since covid, the savings rate is collapsing to GFC levels.

In the last 50 years, there have been only 3 other instances of oil surging more than 50% in one month.

- 1973 OPEC oil embargo

- 1990 Gulf War

- 2020 Covid reopening

That’s it.

This type of shock is nearly unprecedented.

The Fed hiked in 1973.

The Fed cut in 1990.

So what will they do this year?

TLDR: the shock matters, but the starting point matters more.

Let’s jump in the way back machine to revisit 1973 and 1990 so we can more carefully examine 2026.

1973 – Oil Embargo

Oil quadruples nearly overnight

-

More importantly, it never retraces. It remains elevated until the second oil shock five years later with the Iranian Revolution

Gas prices at the pump increased 36%

-

Using today’s prices, that roughly translates from $3/gallon to $4.10/gallon

-

Average prices today are actually $4.55/gallon, so the increase is worse than it was in ‘73

-

CPI climbs from 3.6% to a peak of 12.2% (13 months after embargo)

-

Core CPI climbs from 2.5% to a peak of 11.5% (16 months after the embargo)

GDP was running about 2 points above trend for two consecutive years, suggesting the economy was already overheated. This enabled inflation transmission

-

Today, we are running right on trend, which suggests inflation is less likely to transmit as easily

Wage growth was strong (averaging 7.2%), contributing to the inflation spiral. Prices go up, workers demand a raise, employers give it to them, workers can afford to pay higher prices, producers raise prices…spiral

-

60% of all American workers were union members, and most of those had automatic COLA adjustments based on the prior year’s inflation

-

Today, that number is less than 10% and COLA is no longer automatic

-

-

Wage growth has been cooling post-covid

Unemployment rate was 5% but climbed to 9% within two years

The UoM Survey inflation expectations ran up to 8%

-

Today’s reading is 4.8%, up considerably from February’s 3.4% but not 8% (yet)

M2 money supply was 5% above trend for two consecutive years (just like GDP), but then on trend heading into the shock

-

Contrast that with post-covid stimulus peak of 20% above trend

Fed Funds started 1972 at a very accommodative 3.5% but finished at 5.75% (remember, I said the economy was well above trend)

-

1973: kept hiking to 10%

-

1974: hiked to 12% before slashing to 8% as Burns front-ran cooling economy from oil shock effects

10 Year Treasury climbs from 6% quickly, then gradually pushes north of 8% as inflation settles in

Takeaways and Lessons

Inflation and inflation expectations were amplified because the economy was already overheated. GDP was well above trend, monetary policy was accommodative, and real rates were negative (Fed Funds below inflation). Wages chased inflation, leading to a spiraling effect. Oil climbed and never came back down.

Burns, a close Nixon puppet friend, cut rates too quickly once inflation began to come down. This prevented inflation from ever getting back to baseline. The T10 remained elevated for 20 years and wouldn’t have a 5-handle again until 1993.

What similarities would cause today’s Fed to hike?

Today’s economy would need to reaccelerate or wage pressures would need to pick up (spiral). Both of these could lead to inflation expectations becoming unanchored. Burns’ mistake with oil was to say Fed policy can’t help with a supply shock (like I’ve been saying). That might be ok for some nobody in Charlotte to say, but the Fed can’t directly say that because it could spill over into inflation expectations.

Random Fact

Did you know that Nixon, in anticipation of inflation from abandoning Bretton Woods, froze wages/prices/rents in 1971? I didn’t. AOC would be so proud of him. This led to pent up demand and pricing pressures, which then led to an overall surge in 1972. This conveniently helped him win in a landslide, before the overheating required aggressive intervention and cost Nixon his legacy…along with that pesky Watergate thing…where many of his own recordings showed him applying incredible pressure on Burns to cut rates.

1990 – Gulf War

Oil up 75% in two months, but fell back down as the US helps Kuwait against Iraq

Gas prices at the pump increased 11%

-

Using today’s prices, that roughly translates from $3/gallon to $3.35/gallon

CPI climbed from 4.7% to a peak of 6.4% (2 months after invasion)

-

Core CPI climbed from 4.9% to 5.7% (6 months after invasion)

GDP was at trend but falling as a result of the S&L crisis

Nominal wage growth was about 3%, same as it is today

-

Union membership had fallen to 16% and most automatic COLAs eliminated

Unemployment was at 5.2% at the start but climbed to 7.8% by mid-1992

Inflation expectations climbed from 4% to 6.7%

-

These returned to 4% within one year

-

5yr forward inflation expectations climbed from 4% to 5%

M2 was 5% below trend

Fed Funds was being cut from 9% as Greenspan focused on economic damage from the credit crunch over oil spike

-

FF would get down to 3% in 1992

The T10 started at 8%, climbed to 9% during the shock, then fell back to 5.5% as the economy fell apart

Takeaways and Lessons

The oil shock was transitory temporary. The economy was already cooling off, so Greenspan prioritized that.

What similarities would cause today’s Fed to hike?

Oil dropped as soon as we invaded Iraq…but how long before we have a similar knee jerk reaction in Iran? Even if that happens today, Core CPI peaked 6 months after the invasion…that’s December. There is basically no universe where inflation is plunging in 2026. Will the Fed tolerate the ugly headlines? Will grandma care that prices should cool down in 2027 when she’s responding to a call from the University of Michigan?

Random Fact

As an idiotic 8th grader, I protested the Gulf War because the popular girls were. We yelled, “Peace in the Middle East!” as we tried to stage a walk out of our English class. My English teacher told us to shut up because we didn’t know what we were talking about. That’s not an exaggeration, she told us to shut up, sit down, and keep our mouths shut. She proceeded to rip us new ones for the next 40 minutes. She wasn’t polite and she didn’t try to protect our feelings. She wasn’t supporting the war, she was attacking how little we understood about it. She said we weren’t serious. We didn’t appreciate how Americans were going to die. Her point was made a few weeks later when a US Army car pulled up to our neighbor’s house and told two of my classmates their dad had been killed. He was one of just 294 American soldiers that died in the Gulf War.

2020

I’ve written plenty about this, I’m not rehashing this. How about we all agree that we aren’t about to drop $3T out of a helicopter onto the economy or slash rates to 0%?

This Year

The Fed hiked in 1973 because the economy was already hot.

The Fed cut in 1990 because the economy was already cooling.

It’s more about the starting point than the shock itself.

Today’s economy is hanging in there, but GDP, unemployment, and M2 are basically all on trend. Wages are cooling, not heating up. We don’t have a demand problem. This is not an overheated economy the way it was in 1973, nor is it one that suffering from a credit crisis.

That means the Fed is on hold through year end. Goldilocks. Not too hot, not too cold.

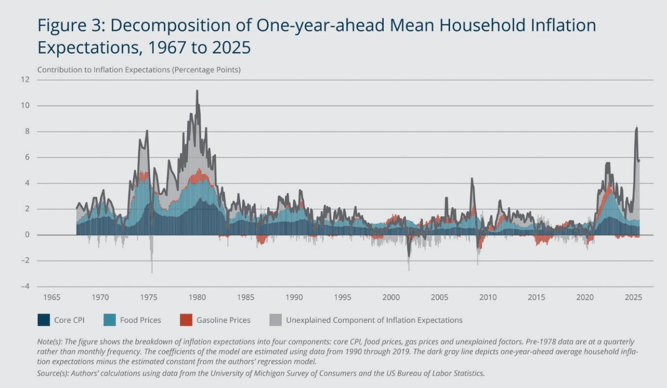

The single biggest risk to a Fed hike this year is inflation expectations. Longer term inflation expectations are hanging in there but definitely climbing.

And one year ahead? Already off to the races. Inflation expectations peaked at an all-time high of 10.4% in early 1980s following the Iran Revolution and resulting oil spike. A Boston Fed research piece last fall (Unexplainable Expectations) showed that about 6% of that 10.4% was unexplainable, eg irrational. That was peak irrational pricing of inflation.

The second highest reading? Last year’s tariffs. If we see another spike in irrational pricing, it could suggest expectations are becoming unanchored. Warsh will be laser focused on this.

I’m not saying a Fed hike will be effective – I think it would be a mistake.

But when all you have is a hammer, everything is a nail.

The Week Ahead

Core PCE is the main event, but GDP also comes out. Obviously, any news on a deal with Iran will dominate rate movements.

Other Random Facts

Volcker has the best branding team ever. He’s remembered as the hero that defeated inflation following the cowardly Arthur Burns. But did you know Volcker cut rates 10% in his first year as Fed Chair? Heck, did you even realize there was a Fed Chair between Burns and Volcker? William Miller hiked rates 4% before passing the baton to Volcker.

Also, Nixon signed the 55mph national speed limit into law in early 1972 to maximize fuel efficiency.