Last Year This Morning

Normally, the year-end newsletter pits various interest rate features in hypothetical bowl game matchups. But with so few bowl games and everything clearly designed to let Ohio State and Notre Dame in as the token sacrificial lambs, it’s a bit challenging.

Plus, we normally review last year’s predictions to see how terribly we did. The pandemic has rendered every forecast worthless. Even if I was right, it was for the wrong reason.

So we will switch it up this year. We will lead off with the Top 10 Lead Pipe Lock Predictions for 2021, and then follow that with a review of my thoughts on COVID and how they might have evolved.

While it feels like an eternity ago, here’s how interest rates went out on NYE 2019.

1-month LIBOR 2.00% (with the market pricing in 1-2 cuts in 2020)

SOFR 1.55%

2 Year Treasury 1.58%

10 Year Treasury 1.91%

Lead Pipe Lock Predictions – 2021

Prediction #1 – Markets Will Do Better Than the Economy

Markets are forward looking. They move in anticipation of the change. Stocks jump before actual EPS improves. The yield curve inverts before the actual recession hits.

Conversely, the economy (GDP) reports what is actually happening right now.

The economy is going to struggle for a long time. There will be long lasting scarring from this pandemic. It will likely take four years for the labor market to regain jobs lost. GDP will recover, but primarily because it’s bouncing off the all-time low. It’s like celebrating Penn State as the most improved team next year… sure, technically it’s true, but that means they had a horrid year this year.

The Great Decoupling began after the financial crisis. Markets love Fed accommodation and stimulus, and it has both in spades. Stocks won’t tank just because of a Biden presidency, and certainly not with a Fed put firmly in place.

Prediction #2 – We Avoid a Double Dip Recession, But Not by Much

Two weeks ago, JPM made headlines by calling for a double dip, with GDP in Q1 2021 coming in at -1.0%.

This is quite a bit below the WSJ consensus forecast of 1.9%.

JPM has reason for concern. In addition to the surging number of cases/deaths and increasing restrictions, the St Louis Fed’s Recession Probability Index had spiked recently.

Because I’m a silver lining kind of guy, I think we’ll split the difference and end up around 1.0%. Despite increased restrictions, it feels like we have grown numb accustomed to a certain amount of COVID headlines.

Prediction #3 – Inflation Will Not be a Problem in 2021

Worrying about inflation is like worrying about Notre Dame showing up in the college playoffs. Sure, I guess technically it could happen, but don’t we have a lot of precedent that suggests otherwise?

Just like the Playoff Selection Committee dealing with a Notre Dame win, the Fed would love to have an inflation problem right now.

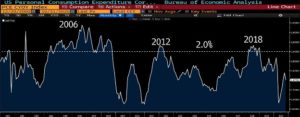

But despite 0% interest rates, massive stimulus, and unprecedented Fed accommodation, Core PCE hit 2.0% just twice since the financial crisis.

Inflation changes direction more quickly than a scrambling Tom Brady, and we will have plenty of lead time to adjust before it represents a threat. When our 13-year-old complained about how much more of his birthday money it took this year to buy his favorite video game, I made him write on the virtual chalkboard.

Prediction #4 – Vaccines Will Reveal Our Self-Centeredness

We will seek out justifications for cutting in line to receive a vaccine, furthering the class warfare that COVID exasperated.

The same Hampton-ite that bemoaned in June, “I know I told everyone to just stay at home, but I didn’t mean grocery store workers, Amazon warehouse employees, or my favorite sommelier!” will now become, “But I am important and have money, therefore I should be able to get access to a vaccine first. I wasn’t able to summer in Monaco!” The low brow equivalent might be, “I need to go to the Penn State white out game!”

I wish I could say I won’t be guilty of this, but if my family and I have the opportunity to be vaccinated by pulling some strings, I’m not sure I will pass it up. I’ll justify it somehow, dress it up in rationalizations, but I will only contribute to the growing divide.

Prediction #5 – Lenders Will Increasingly Issue New Loans on SOFR, But LIBOR Will Still be Around

Freddie pushed the market toward SOFR-linked issuances in Q4, but traditional lenders haven’t begun the process in earnest. They will begin to make the shift in 2021.

Hedging volume on SOFR will continue to tick up. More providers will offer SOFR hedges. They might even start using SOFR futures to hedge their positions instead of using a LIBOR correlation position.

But LIBOR will still be in place a year from now. Two weeks ago, the regulators punted on the conversion of legacy contracts. Don’t be surprised if regional banks are given a similar reprieve.

Prediction #6 – Financial Conditions Will Set the Stage for a Strong Recovery… Eventually

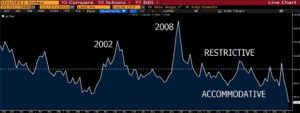

If the recession hasn’t felt quite as awful as -33% GDP would suggest, a large part of that is how accommodative financial conditions have been.

Like the Chicago Bears on drafting Mitchell Trubisky, the Fed went all-in on accommodation as soon as COVID hit. The lesson learned from 2008 was, “We’re going to have to eventually anyway, let’s just fast forward and limit the damage.”

Keep in mind, easy financial conditions benefit readers of this newsletter far more than the average minimum wage worker. That’s why markets (and assets like real estate) will do better, faster, than the typical employee.

Prediction #7 – Fed Balance Sheet Never Gets Paid Down

A few months ago, I wrote about hysteresis. It’s the concept in economics that says the effects persist after the initial causes giving rise to those effects are removed1.

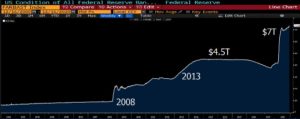

Post financial crisis, the Fed’s bloated balance sheet persisted even though the economy recovered. Emergency measures became the new normal. The Fed could barely raise rates. It couldn’t reduce its balance sheet. Hysteresis.

“Now we have even more intervention. A much bigger balance sheet. Direct asset price manipulation.

The Fed is no longer the lender of last resort, it is the lender of first resort.

When we are on the other side of this, I’m not confident we will allow the Fed to extricate itself from these policies. We will demand low rates. We will demand high stocks. We will demand to be protected from default. We will demand a bailout even after a decade of profitability (cough cough airlines).”

How will we ever pay down this balance sheet? The minute the Fed tried to reduce it from $4.5T, the markets began to wobble. Now we’re north of $7T and the Treasury doesn’t want rates to spike. The Fed reducing its holdings would most certainly put upward pressure on yields, so instead Yellen and Powell will have a *wink wink* agreement to operate independently.

Prediction #8 – An Inflation Shock is the Biggest Risk to Rates

I know I said inflation isn’t a thing. And I believe that. Certainly for the foreseeable future. But as my annual recap shows, I am wrong. A lot.

If inflation somehow becomes a threat, we could experience a dramatic spike in yields.

This could come in many forms: A surprise in the actual data. A misstep by Powell about tapering bond purchases. Massive stimulus (e.g., Dems win both Senate seats in GA and a $3T package is back on the table).

The prediction here isn’t that inflation will take off in 2021, but rather that a surprise represents the biggest risk to higher rates. Basically, the most non-committal prediction ever.

Prediction #9 – The Fed Remains Max Dovish

The Fed won’t even so much as hint at the possibility for higher rates in 2021. Even though the country should be vaccinated by the second half, the true recovery will still be one to two years away.

Per #8, Powell avoids a 2013 Taper-Tantrum-like spike in yields by sending all sorts of accommodative signals.

There won’t be a single whisper about rate hikes. They won’t even allude to a return to normalcy in the future. If you have floating rate debt, you have as little risk as you will ever have for the next three years. And three years will probably become five years (or more).

The Fed’s own projections show Fed Funds on hold through year-end 2023.

Don’t fight the Fed.

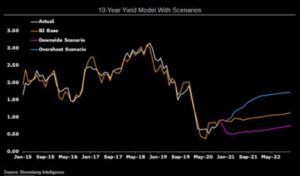

Prediction #10 – The 10 Year Treasury Will Finish the Year Below 1.50%

I’m not sure this counts as a bold prediction. In the September 8th newsletter, we discussed how the yield curve behaves after a recession2.

“Using the previous cycles as our guide and making the movements proportionate, the yield curve would steepen to about 1.00% by year end and the 10T would be around 1.15%.”

Not too shabby, right? With a friendly stimulus announcement, breaking through 1.00% feels like a distinct possibility.

The Bloomberg rates model puts the 10T at 1.00% (snoozefest), with a high side of 1.56% and a low side of 0.50%.

There really isn’t a reason for the 10T to break above 1.50% next year. Even as the US begins to recover, the rest of the globe will trail. If the German bund is in negative territory, how high can our own yields move?

That doesn’t mean we can’t experience pops here or there, but a sustained movement higher feels unlikely.

Plus, the Fed could always make an off-the-cuff remark about Yield Curve Control and pull rates back down.

There you have it, the Top 10 Lead Pipe Lock Predictions for 2021. You’re welcome.

We hope you enjoy the holidays and 2021 turns a new page. We’ll take a two-week hiatus for the holidays and return next year.

Continue reading below to see my self-review of the 2020 newsletters.

2020 – What I Got Right and Wrong

#1 – Why Flattening the Curve is Overrated

We have to start with the one that went viral. Why Flattening the Curve is Overrated3 had more than a million reads within a few days, almost entirely from people that it wasn’t intended to be written for.

The newsletter opened with, “Here is the question that no one has answered to my satisfaction – can you describe to me what the successful lifting of quarantine looks like?”

I’m not sure that has been answered yet. It felt so obvious to me at the time, but I was roasted.

My obsession with real data, and not just the “follow the science” mantra, began with the widely read, “The Hammer and the Dance”4.

This article was singlehandedly responsible for my deep dive into the pandemic. It struck me as horribly unrealistic. Panic-inducing. Worst of all – easy to grasp. “Flatten the curve” is just so easy to grasp intellectually. It’s cognitively convenient. This would shape my view of the media’s portrayal for the rest of the year.

The author’s own summary of the article: “Strong coronavirus measures today should only last a few weeks, there shouldn’t be a big peak of infections afterwards, and it can all be done for a reasonable cost to society, saving millions of lives along the way.” (emphasis mine).

I disagreed.

“We are committing to be on quarantine between now and when a vaccine is developed, not just the next two weeks. I’m not sure that has sunk in yet for those that believe isolation is the cure-all here.

If we are truly only on lockdown for the next two weeks, it’s probably a cost we are all willing to bear. But I have some bad news for you – it won’t be two weeks. Not with the current psychology of this disease. We are starting with just two weeks because it makes it easier to accept. It’s comfortable. They’re keeping us calm. Easing us into it. The next announcement is coming. Two weeks will become four weeks. A month will become three months. This could drag on the rest of the year.

The minute we lift quarantine measures, the second wave begins. Eventually the third wave. Or a fourth.”

But while I disagreed with his assessment, I recognized that none of us (least of all me) had any clue of the best path. Taking an overly cautious approach could be forgiven, especially in the early days.

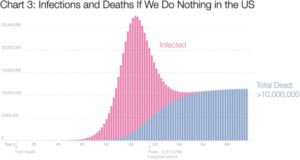

But that’s not what got me riled up. He wrote, “If the coronavirus is left to spread, the US healthcare system will collapse, and the deaths will be in the millions, maybe more than 10 million.”

Thankfully, he included a helpful graph and a link to this really cool model that allowed you to play with the inputs. His projection?

10mm Americans dead within 200 days.

10mm Americans dead within 200 days… that sort of absurd projection contributed to the panic. The use of a model that you could manipulate made it feel more legitimate.

It was my first exposure to the importance that an intellectually easy concept would play in the pandemic. Flatten the curve. It’s just so easy to grasp. You either believe in it or you think the earth is flat and want people to die. It was also when I realized how much control the media had on the portrayal of the pandemic.

He concluded with a call to arms, evoking a WWII image. “What if Churchill had said the same thing? “Nazis are already everywhere in Europe. We can’t fight them. Let’s just give up.”

I love when Stanford MBA ex-consultants reference wars while typing away safely in their million-dollar San Fran apartments…

Grade – B+. I stand by my position. Isolated lockdowns can make sense (nursing homes), but the blanket lockdowns are unrealistic to enforce and have questionable benefits.

#2 – The Human Toll of an Economic Pandemic

If cognitive laziness is the biggest theme of the pandemic, the second biggest has been the lack of appreciation for unintended consequences. On April 6th, I wrote about the human toll the shutdown might have5. We touched on things like mental health, education, crime, etc.

I concluded with some predictions.

- “By month end, the government will have a more targeted plan to un-quarantine, even if it won’t begin until June. Americans may comply with an extension into May, but only if it comes with a light at the end of the tunnel.”

Grade – D. The lack of a coordinated federal response is probably my biggest complaint about the mishandling of COVID-19. I thought for sure there would be a sensible, targeted re-opening. I was wrong. State by state decisions were made, largely along political lines.

- “Masks are the first example of what’s to come as we un-quarantine. There will be more and more announcements similar to this that will help us feel like we can get back to work.”

Grade – B. Masks certainly caught on as the PPE de jure, so I think I got that. But things like cleaning off surfaces, washing hands, eye protection, etc. all fell by the wayside. Remember when we thought we had to wipe down our groceries?

#3 – Medical Models are as Imprecise as Economic Models

On April 13th, I wrote about the shocking variance between medical projections6.

I really got on to Governor Cuomo and Mayor de Blasio for their botching of the ventilator issue. Mind you, we were a month in at this point. Cuomo was making headlines for demanding 33,000 ventilators and telling Trump to pick which 30,000 New Yorkers should die. It seemed absurd. How could NY go from needing a few hundred to over 30,000 in a few weeks?

Furthermore, he totally failed to consider the impact of his words. What if a ventilator destined for Michigan got diverted to NY because he out-screamed the Michigan governor?

Not only did NY not need those ventilators, topping out at 5,000 used at its peak, it turned out ventilators actually hurt a lot of COVID patients.

Again, I get it – everyone was just doing the best they could. But leadership should be careful not to politicize the pandemic because it leads to everyone else doing the same. Here was a recap of shifting projections.

I also cited Stanford epidemiologist John Ioannidis7 saying we have massively overestimated the fatality of COVID-19. “When you have a model involving exponential growth, if you make a small mistake in the base numbers, you end up with a final number that could be off 10-fold, 30-fold, even 50-fold.”

Ioannidis continued, “If I were to make an informed estimate based on the limited testing data we have, I would say that COVID-19 will result in fewer than 40,000 deaths this season in the USA.” (emphasis mine).

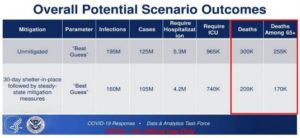

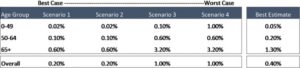

This stood in stark contrast to a confidential presentation that same week by the Homeland Security and Health and Human Services, obtained by the “failing” New York Times, which made some striking worst-case scenario forecasts.

Grade – C. This is probably my biggest regret of the year. I felt like 40,000 deaths was too low, but far more likely than 2mm+ deaths. I thought we would ultimately see around 100k-150k COVID deaths by year end, largely because it would do what a virus does – spread. The fact that we are north of 300k is heartbreaking.

I thought we would figure out a better way to live with COVID while taking reasonable precautions. Those with the highest risk would adjust their behaviors, and that would waterfall down the risk spectrum. I have been surprised by the sheer number of people that still don’t take it seriously. I still don’t think government intervention is the best solution, but I can understand why political leaders feel it necessary to enact restrictions.

#4 – Deflation (And Maybe Something About the Protests)

It was a rough summer. I obviously hated rioting and looting, but I could also appreciate frustration boiling over. It led to a tough conversation with our children about white privilege8.

“Would you agree that those two kids, growing up side-by-side, one white and one black, have the same likelihood of committing a crime?” Yeah, they seemed to agree.

“But if a police officer walks up to them both, the white kid is safer. If you’re standing next to Kawan and a police officer walks up to both of you, Kawan is more likely to have a bad encounter.”

And that’s what the protests are about.

If my son’s life was dependent on how that interaction with the police officer was about to go, would I have him switch places with Kawan? Not in a million years.

And that’s what the protests are about.

And that means I know it. I am aware of it. And I haven’t done anything about it.

Grade – C. Maybe we get some credit for having the discussion with our kids, but I’m not sure my behavior has changed since then. Life for this middle aged, upper middle class, white guy largely went back to normal. How convenient.

#5 – Politics Dressed Up in a Lab Coat

On June 29th, I wrote about my increasing frustration about the sensationalism of the pandemic. How you viewed COVID basically told us your political beliefs9. Furthermore, the stats were being skewed in both directions. Fox was underreporting the severity, while CNN made it seem like the apocalypse was upon us.

I think we should pay way more attention to the mortality rate than total number of cases. This is what we should be basing decisions off of. The CDC’s best estimate for COVID’s mortality rate across all age brackets is 0.4%. As a frame of reference, the seasonal flu is usually around 0.1%. In other words, about 4x deadlier.

-

- For those that say it’s just like the average flu, it’s not

- For those that say it’s just like the second coming of the Spanish Flu, it’s not

If you’re under the age of 50, the mortality rate is around 0.05%.

Remember all those dire forecasts of 4mm Americans dying? They were based on a mortality rate of 3.2%. Right now, the CDC’s best guess is 0.4%. Strip out those with underlying conditions. Or address the fact that the CDC estimates at least 35% of all COVID positive Americans are asymptomatic. The real numbers fall further.

Grade – A. Most people stopped at whatever their favorite news source told them. We got into the weeds of the CDC’s real data. That deep dive helped shape my view on the situation.

#6 – The Illusion of Knowledge

Better known as The Mask Newsletter, I wrote on July 19th, I wrote about the blind acceptance that masks were the single most effective deterrent of coronavirus spread10.

I included a graphic from the CDC’s website that clearly said surgical masks don’t prevent the spread of airborne viruses. I included the following quote directly from the WHO’s website:

“There is limited evidence that wearing a medical mask by healthy individuals in the households or among contacts of a sick patient, or among attendees of mass gatherings may be beneficial as a preventive measure. However, there is currently no evidence that wearing a mask (whether medical or other types) by healthy persons in the wider community setting, including universal community masking, can prevent them from infection with respiratory viruses, including COVID-19.” (emphasis mine).

What really drove me nuts was how many news organizations were claiming, “The science backs up mask usage” without actually citing scientific evidence. They cited other news articles. A NYT’s article referenced a Vanity Fair article, which in turn referenced a debunked study. Just because we say, “the science backs it up” doesn’t necessarily make it so. But… wearing a mask is just so intellectually easy to grasp. Just like Flatten the Curve or “get us ventilators!” – it just makes so much sense. But that doesn’t make it true.

The most authoritative study I could find was a meta study backed by the WHO. It concluded:

- Assuming no physical distancing and no mask, the transmission rate was 17.4%.

- Assuming no physical distancing with a mask, the transmission rate dropped to 3.1%.

So wearing a mask could reduce the transmission rate by 82%. (17.4%-3.1%)/17.4%

Using the CDC’s best estimate of mortality rates for my age bracket, the likelihood of me dying from COVID if I come into close contact with someone that has it:

Without a mask 0.069%

With a mask 0.012%

That’s a compelling drop. Is that enough for me to say, “I should wear a mask when I am in crowded places or talking to an immunocompromised person?” Yes.

But across 1,000,000 people, that’s just 572 lives saved. I’m not sure that ties out with the story we are being presented about masks.

Do they help slow the transmission of COVID? Yes.

Are they the next best thing to a vaccine? No.

Grade – B. I wear a mask to go into stores now, whereas I did not when I wrote this in July. I do it to make other people feel comfortable or to adhere to the store’s rules, but I still prefer to just keep my distance from people. And I still worry that people are engaging in behavior they would otherwise avoid, believing a mask is keeping them safe.

Overall Grade for the Year – B Minus

I get dinged for not predicting a pandemic, but since I am grading on a curve, I snag the B.

I hope we got credit for tackling challenging topics with data-based analysis. I worked hard to source everything I wrote, providing citations and links to every single piece of evidence or quote.

Reasonable people can disagree, but I didn’t want to resort to the same cognitive laziness I was railing against.

Most importantly, I sincerely hope no one felt I was callous or insensitive. It was a challenging year to write about something as mundane as interest rates, and I appreciated the opportunity to step outside that box.

I look forward to the day when all I write about is how boring interest rates are again.

Sources

- https://www.pensford.com/the-illusion-of-safety/

- https://www.pensford.com/how-does-the-yield-curve-behave-after-a-recession/

- https://www.pensford.com/why-flattening-the-curve-is-overrated/

- https://tomaspueyo.medium.com/coronavirus-the-hammer-and-the-dance-be9337092b56

- https://www.pensford.com/the-human-toll-of-an-economic-pandemic/

- https://www.pensford.com/medical-models-are-as-imprecise-as-economic-models/

- https://profiles.stanford.edu/john-ioannidis

- https://www.pensford.com/deflation-and-maybe-something-about-the-protests/

- https://www.pensford.com/politics-dressed-up-in-a-lab-coat/

- https://www.pensford.com/the-illusion-of-knowledge/