If you caught our previous article on why you should Negotiate Those Floors, then you’re already aware of what your imbedded loan floor could do to you future interest expense. But what if you didn’t negotiate it and you’ve already closed. In this resource, we’ll talk about how you could negate its impact by buying out the floor.

Buying Out the Floor

Floors are most frequently seen in the loan documents but can also be bought from third party banks as a separate instrument just like caps. If your loan has a built in floor, you could enter a separate contract that pays you in the event your floating rate falls beneath the strike. This is commonly referred to as “buying out the floor” and is just like a rate cap but in the other direction.

Let’s assume the following scenario:

- You have a SOFR based financing with a loan floor set at 3.00%

- In order to negate the impact of the loan floor, you purchase a separate floor contract struck at 3.00% that pays you for any amount SOFR falls beneath the strike

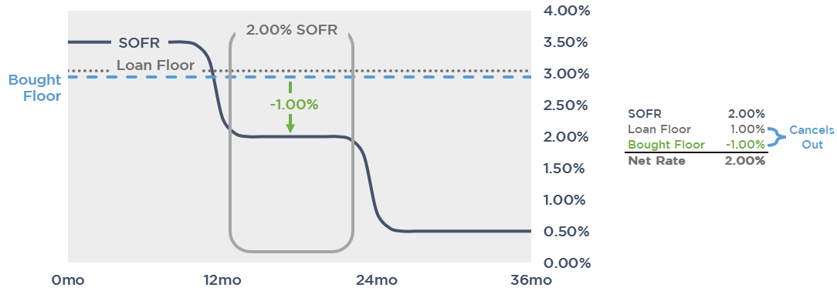

The graph below illustrates how this would play out if SOFR resets at 2.00%.

Because SOFR is below the loan floor, you’re stuck paying 3.00%, or 1.00% more than you would if there wasn’t an imbedded floor. This is where the separate floor contract comes into play. Because the strike was set to match the loan floor, it negates its impact completely and allows the loan to function as if there wasn’t an embedded floor on the loan to begin with, bringing the net rate back down to floating at 2.00%. It now feels like you have no floor at all!

Many clients consider the breakeven point. For illustrative purposes, if a 3 year floor for $25mm at 3.00% costs $300k, in order for the floor to pay for itself, SOFR would need to average 2.60% or lower over 3 years to pay for itself. Alternatively, the floor will have also paid for itself if SOFR averages just 1.80% in the final year.

Flooridors

Simply buying out the floor negates its potential impact entirely but what if the upfront premium is too cost prohibitive? An alternative approach would be to simultaneously sell back a lower strike floor to the bank creating a floor corridor or, as we call it, a “flooridor.” The instrument behaves similarly in concept to a cap corridor, just in the opposite direction. The idea is to lower the upfront cost by netting the value of the sold strike against the cost of the purchased strike.

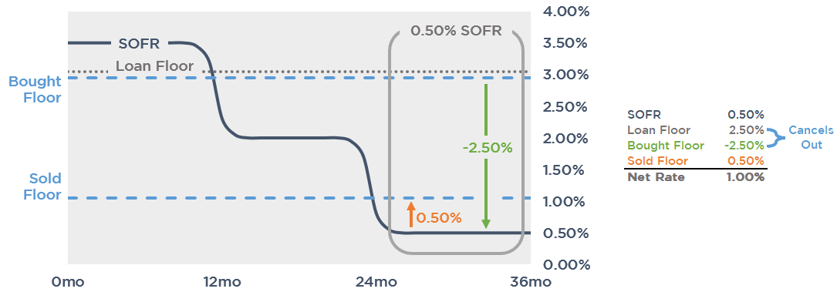

Let’s go back to our example structure but add in a sold floor at 1.00%

- Buy a 3.00% floor – If SOFR falls below this strike, the bank owes the borrower the difference between SOFR and the strike.

- Sell a 1.00% floor – If SOFR falls below this strike, the borrower owes the bank the difference.

Here’s how that would play out if SOFR resets at 0.50%.

The bought strike is negating the imbedded floor entirely, reimbursing the borrower the full 2.50% to make up the difference. However, the sold floor is costing the borrower 0.50%, bringing the effective rate back up to 1.00%.

Because both strikes would be bought and sold with the same bank, you would never actually pay the bank. Instead, they would just reimburse you for the net difference between the payments. Further, because the bought floor is struck higher than the sold floor, the bought floor will always be paying out more meaning the flooridor can only be an asset to you.

The maximum reimbursement is equal to the difference between the bought and sold strike. In effect, the loan floor is lowered to the sold floor strike but not removed entirely. For this reason, flooridors tend to make the most sense if you believe floating rates might fall below current expectations, but not necessarily all the way back to 0%, or if you want to improve your position for the lowest cash outlay possible.

Comparing the outright purchase of a floor to a flooridor, selling back a lower strike can help to offset a substantial piece of the premium.

Conclusion

If you’re stuck with an unfavorable floor on your loan and want to regain the ability to float lower in the future, you could enter into a separate floor contract that would reimburse you in the event rates fall below the floor.

To save on upfront costs, you could simultaneously sell back a floor at lower strike, netting the sold strike’s value against the cost of the bought strike, creating a flooridor. With this strategy, you’re exchanging some of the risk below the lower strike for a lower premium.

If your financing has an embedded floor and you have questions about whether buying a floor or flooridor could make sense, reach out to the experts at pensfordteam@pensford.com or (704) 887-9880.