Deeply in the money cap strikes have proved the most beneficial as rate expectations started climbing in late 2020. Now that there is a 40% chance of a cut priced in for the March Fed meeting and an almost 100% chance we’ll get a cut by the May meeting, it may be time to rethink what strike is optimal.

Since March is the first meeting with a significant chance of a cut priced in, we examined the performance of deeply in the money caps purchased two months prior to the first cut to a cap set at the bottom of the forward curve over the hedge term.

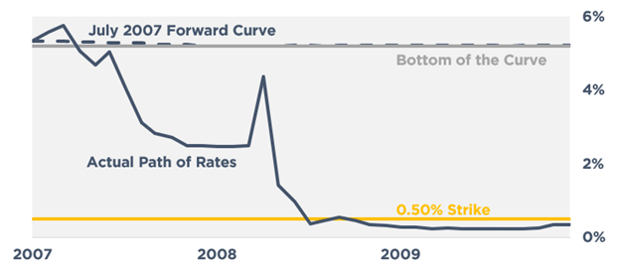

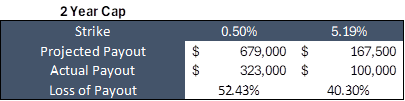

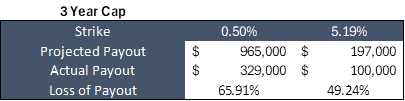

July 2007

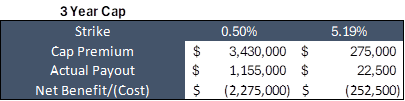

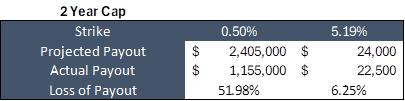

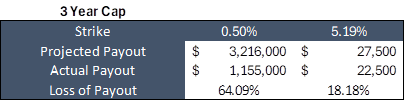

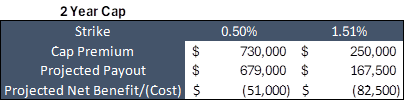

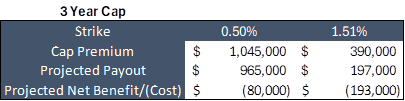

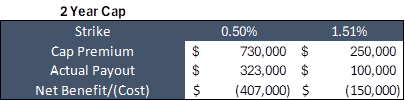

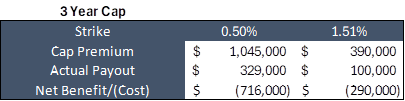

The first cut during the GFC was in September 2007. In July, markets expected rates to remain flat around 5.19% for the foreseeable future and what happened was wildly different.

Looking at a $25mm cap for example, the tighter strike cap appeared to be a more efficient use of funds at the time of execution based on the forward curve.

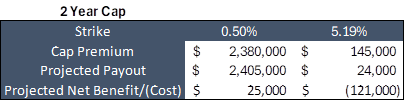

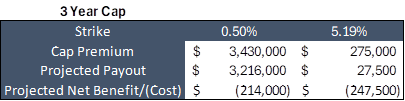

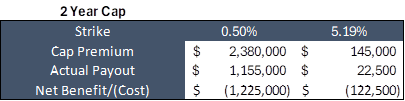

As the Fed cut rates the payout of the 0.50% strike fell short of what the market projected leading a cap at the bottom of the curve to be a more efficient use of funds.

The 0.50% cap lost the majority of its projected payout as rates fell, while the higher strike cap performed much closer to expectations.

On a $25mm financing, losing ~$1.25mm of projected payout on the two year cap and $2.06mm on the three year cap would mean a 4% and 8.25% decrease in funds resulting from debt.

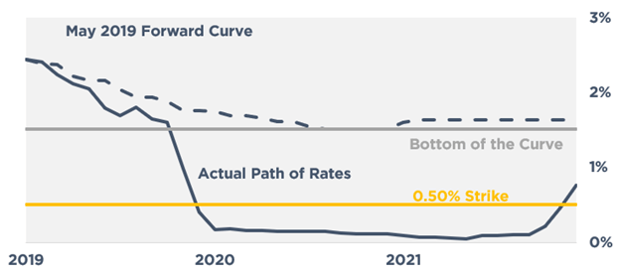

May 2019

In May 2019 markets expected a soft landing, and for the next eight months it looked like that was going to happen.

Again, the 0.50% strike cap was projected to be the most efficient use of funds.

As we all know, Covid-19 led rates down a much different path which required the Fed to cut rates to zero and maintain those levels for an extended period of time.

It’s no surprise that caps lost a meaningful amount of payout compared to expectations at execution and that the higher strike turned out to be the more efficient use of funds.

Putting this Strategy in Play – Establishing an Interest Escrow with your Lender

Some borrowers are taking on new debt today with required strikes in the 5% to 6% range where they have flexibility surrounding their strike. Others have debt from 2020 and earlier where strike requirements may be closer to 1.00%.

Some lenders are allowing borrowers to purchase a higher strike today in exchange for escrowing the difference in cost between their required strike and desired strike. By escrowing, borrowers ensure their ability to meet the increased interest expense resulting from decreased cap payments. While borrowers don’t get to keep the money in their pocket at the outset, this allows them to benefit from rates falling below expectations. In that scenario, when they exit the debt, they receive the remainder of that escrow balance back.

If borrowers think that we’re poised to see rates fall more than expected in the coming months/years as we have seen in previous cycles today could be their last chance to raise their cap strike before values plummet.

To discuss this strategy or any other hedging solutions, reach out to us at Pensfordteam@pensford.com or (704) 887-9880.